Weather: As with all frost events, it takes some time for the actual damage to become clear – in the case of the US HRW crop, that time period was apparently a few days, such is how bad the crop is. It feels like this may be a knock out punch for many areas – heat/lack of rain now frost. Sheesh.

Australian east coast is in a strange position – the export path is shut, carry out it growing but so is flat price. It feels like the northern market has jumped ahead of the curve but, now that has opened discussions about SA/WA imports to Brissy.

Markets

Donald Donald Donald. Its a Tuesday, that must be tough talk day – plenty of sound bites about the bombs kicking off again if…

Markets are getting resistant to the Truth Social traffic – moves are getting more muted and there is a growing level of comfort with the new normal. Im sure you are all sick of my one liners… but the function of the market is to move the surplus to where its needed. Classic example of Russia putting wheat into Iran through the Caspian Sea.

Qld diesel has moved from $3.20/lt to $2.60/lt – 50psi and no roof racks… probably…

Day Ahead – Australia

Shift F9 on spreadsheets in every trade house trying to work out how to get grain to Queensland. Additionally, with diesel coming off, the reach of the Downs market into the central west of NSW has got a little further.

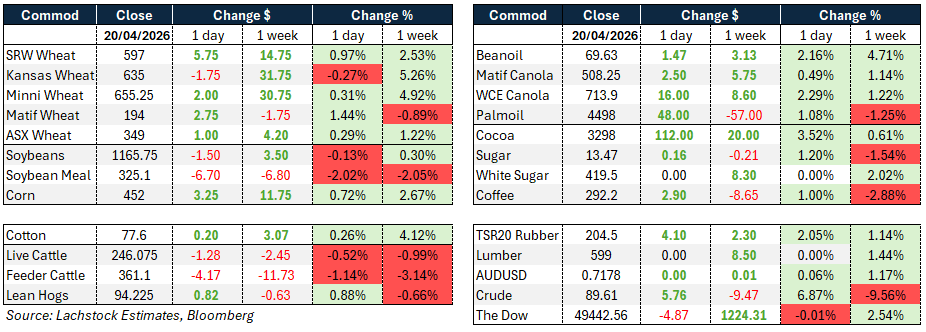

Global wheat: Chicago +5.75c, Kansas -1.75c, Matif +€2.75

Global wheat: Chicago +5.75c, Kansas -1.75c, Matif +€2.75

Wheat markets were mixed on the day with Chicago finding support from a combination of frost damage concerns and strong export inspections, while Kansas gave back early gains to finish lower.

Kansas had rallied as much as 13.25 cents at its peak before selling pressure took hold into the close, with the weakness attributed to forecast rainfall returning to the southern plains in the 6-10 and 11-15 day outlook, intermarket profit taking given how stretched Kansas had become against other classes and competing origins, and news that India had approved an additional 2.5 million tonnes of wheat exports, bringing total permitted exports to 5 million tonnes.

While Indian domestic prices remain above global export levels limiting the immediate impact, the approval acts as a ceiling on any sharp rally in world values.

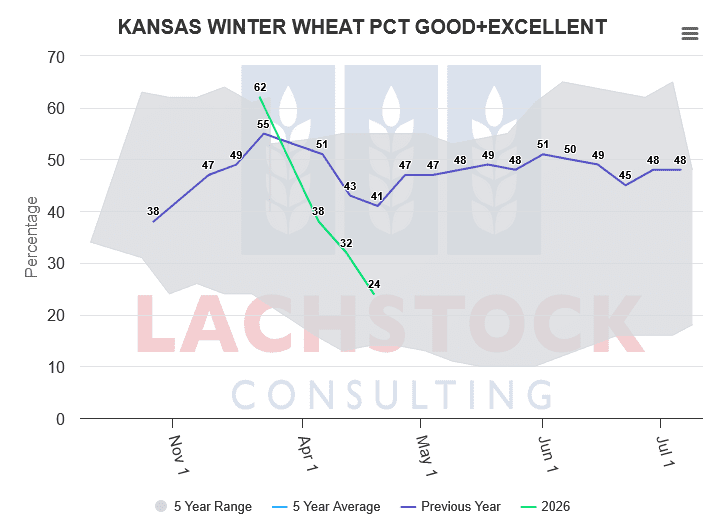

After the close, winter wheat conditions fell 4 points to 30% good to excellent nationally, with Kansas dropping a significant 8 points to just 24%, a result that was at the worse end of pre-report estimates. The crop has now been subjected to multiple freeze events, excessive heat, and persistent dryness, with some areas considered beyond recovery.

Spring wheat planting came in at 12% against expectations of 13%.

Weekly export inspections of 518,000 tonnes exceeded trade ideas and left cumulative shipments running 14% above year-ago levels.

Separately, Russia shipped wheat to Iran via the Caspian Sea for the first time in years, highlighting the growing importance of that route given Middle East disruptions.

Chinese customs data showed year-to-date wheat and wheat flour imports up 495% year on year to 1.79 million tonnes, though this reflects the low base from prior year rather than a structural shift.

Other grains and oilseeds: Corn +3.25c, Soybeans -1.50c, Matif Canola +€2.50

Corn was the standout performer on the day, drawing support from firm cash markets, strong export inspections of 1.669 million tonnes that left the cumulative pace 32% above year ago levels, and a meaningful lift in crude oil prices following the reimposition of controls on the Strait of Hormuz.

Corn planting matched expectations at 11% complete. The interior and CIF markets remain well supported with growers largely absent from the cash market.

On a fob basis the US Pacific Northwest remains the cheapest origin into Asia, though Argentina is closing the gap and is the world’s lowest cost overall fob.

Canola pushed solidly higher on ICE with Matif rapeseed and Malaysian palm oil also firmer, all drawing support from the surge in crude.

The soyoil complex was the notable mover within beans, with board crush firming 3 cents to 315.5 cents on the back of a 147-point gain in soyoil, while soymeal shed $6.70 and beans themselves dipped 1.5 cents.

Bean export inspections of 749,000 tonnes were at the high end of estimates but cumulative shipments remain 25% below year-ago levels. Bean planting at 12% matched expectations.

On the fundamental side, China’s agricultural ministry projected soybean imports would fall 6.1% in 2026, extending a broadly bearish demand narrative, and US soybean export orders remain well below historical norms despite China’s partial return as a buyer following the bilateral trade truce.

Arrivals of US beans into China in March reached 1.8 million tonnes, exceeding Brazilian supplies of 1.4 million tonnes for the first time in a year, though US shipments were still 24% below the prior year.

Brazil’s soy harvest was 92% complete as of April 16, slightly behind last year’s pace, while the 2025/26 production estimate was nudged higher to 178.11 million tonnes.

The Brazilian winter corn crop is developing well with favourable conditions in Mato Grosso supporting expectations of a bumper outcome.

Macro: AUD 0.7174, Dow -4.87, Crude +5.76

The dominant macro driver of the session was the Middle East, with the Strait of Hormuz remaining closed and the United States seizing an Iranian-flagged cargo vessel over the weekend, an act Iran characterised as piracy. Brent crude surged more than 5% on the day, trading near $95 a barrel, unwinding most of Friday’s decline.

President Trump confirmed the ceasefire with Iran expires Wednesday and stated an extension is highly unlikely, while also asserting the strait will remain blockaded until a deal is signed.

Vice President Vance departed for Pakistan where a second round of talks is expected, joined by Jared Kushner and Steve Witkoff. Iran confirmed it was sending a delegation though the composition remained unclear, and significant internal divisions within the Iranian leadership between hardliners and more pragmatic officials continue to complicate negotiations.

Equity markets retreated from recent highs on the ceasefire uncertainty, with the Dow slipping modestly.

On the data front, preliminary April global PMI data is due later in the week alongside US March retail sales, neither of which is expected to shift major central banks away from their current wait-and-see posture.

March CPI across major economies showed elevated headline readings driven by energy, but with no clear transmission into underlying inflation, central banks appear content to hold until further clarity emerges.

Nitrogen fertiliser prices have approximately doubled since the start of the Iran conflict, with industry executives warning of further upside if the strait remains closed.

Brazil’s heavy reliance on imported fertiliser, sourcing 95% of nitrogen and 96% of potash from overseas, makes it particularly exposed to any prolonged supply disruption.

Local: Bids were softer to start the week in the west but recovered through the day as global risk premium was again applied, canola finished the day A$770/t current season and $805 new, wheat was $333 and $358, barley $341 and $331 FIS Albany.

Through the east canola was $750 current season and $783 new, wheat $338 and $368, barley $315 and $328 track Geelong.

Lentils remain around $700 delivered southern ports with steady container demand, although global appetite remains subdued with a large Victorian program still to work through.

The AUD has strengthened in recent weeks to now be trading above 71c as USD safe haven buying unwinds on easing conflict expectations, acting as a slight headwind to local export competitiveness.

In other news, national cattle yardings pushed to their highest weekly level of the year post-Easter, with MLA reporting more than 107,000 head yarded last week and monthly throughput reaching 409,280 head, the largest seen in some time. Northern NSW continues to drive the lift, with dry conditions and frosts forcing turnoff, while prices have generally held together despite the larger supply — the EYCI remains around 802c/kg cwt and feeder steers 456c/kg, although processor cows eased 6c last week to 323c/kg as freight and weight sensitivities start to bite.

HAVE YOUR SAY