Weather: Rain in the US started the session looking pretty good, but, as the updates rolled through, things looked worse and worse – there is still rain for KS and OK but the heat and the wind are extreme.

Europe looks pretty good – France will miss out this run but Russia is set to get a decent drink.

WA is going to get belted, particularly Gero zone.

Markets:

Market physiology is a fascinating thing. At the absolute base level, all that happened overnight was Trumps tone changed. Reports from Iran suggest there isn’t any discussions happening and they were actively bombing while Donald was saying they are making good progress. Infrastructure damage is extensive, there is no guarantee that the strait will open yet the market shed a bunch of risk premium.

However, the world now has a 5-day timer that has started and will be looking for a resolution. It seems a pretty common view that Trump is trying to exit and save face but, if it’s one thing we have learnt through this – it’s that Donald can flip the script at any moment.

Day Ahead – Australia:

More conjecture and more paralysis. From a growers perspective, just cause Don said we are making headway hasn’t resulted in a bunch of urea trucks rolling through the gate. We still have supply issues and they will exert pressure on this growing season, regardless of what happens in the next 5 days.

Lots of discussion around planted area composition, does this change what growers plant. For the NNSW grower its more about rain than margin today.

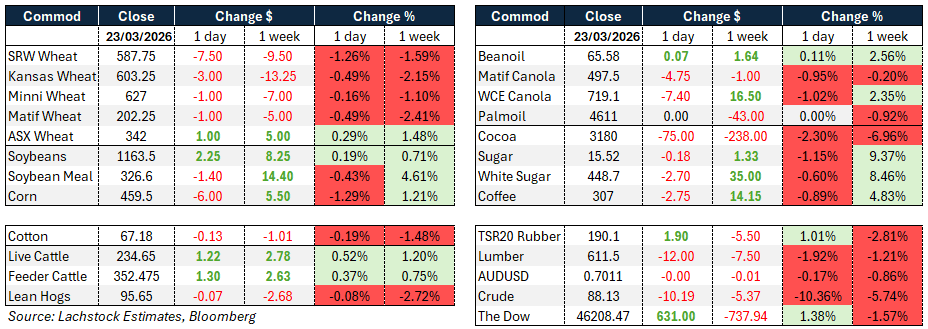

Global wheat: Chicago -7.50c, Kansas -3.00c, Matif -€1.00

Global wheat: Chicago -7.50c, Kansas -3.00c, Matif -€1.00

It was a volatile session for wheat markets, with prices trading comfortably higher for much of the night session before being dragged sharply lower when President Trump announced Iran had been given a further five days to negotiate before any strikes on energy infrastructure.

Kansas City wheat fell from 614 to 591 in under ten minutes before partially recovering to close around 605. The news was initially interpreted as a de-escalation, sending crude oil down around 14 percent and taking grains with it, though Iran denied any formal negotiations had taken place, adding to the confusion.

Implied volatility in Chicago wheat eased back, closing at 32.15pc versus 34.20pc on Friday.

On the weather side, HRW crop conditions remained the key domestic focus. Midday maps showed some improvement in the 11-15 day outlook earlier in the session but moisture was progressively reduced as the day wore on, leaving the ten-day forecast hot, dry and windy. After the close, by-state condition ratings confirmed the deterioration with Kansas down 6 points, Oklahoma down 4, Colorado down 5, and Texas up 1.

US wheat export inspections of 458,000 tonnes topped estimates and are running 18pc ahead of last year.

Russian March grain exports are estimated at 4.7 million tonnes (Mt), up sharply from 3.5Mt in February and roughly triple year-on-year levels as importers moved to secure supply amid the Middle East conflict. Russian cash wheat was unchanged at $240.50.

European winter crops are reported to be resuming vegetative growth under favourable conditions with adequate soil moisture.

Chinese authorities have reportedly sold out two recent 500,000 tonne wheat auctions and are preparing to offer 800,000 tonnes in the next round.

Other grains and oilseeds: Corn -6.00c, Soybeans +2.25c, ICE Canola -$7.40

Corn had a wide and violent session, trading a range of 456.50 to 473.75 before settling down 6 cents at 459.50. The market lost 14 cents in around 15 minutes at the peak of the crude oil selloff before finding support, with some arguing the limited net loss on the day was a relative win given the macro backdrop. A daily sale of 102,000 tonnes of corn to Mexico provided some underlying support, and weekly export inspections of 1.7 million tonnes were in line with expectations and remain 38% ahead of last year’s pace.

With the USDA Prospective Plantings report due in just over a week, managed money continues to add to their long, currently sitting at around 53% of their record position. AgMarket.net is projecting corn plantings at 94.4 million acres, above the USDA’s February estimate of 94 million, even as the Iran conflict constrains fertiliser availability.

Soybeans held up best of the grains, with May futures finishing up 2.25 cents. Meal lost $1.40 while bean oil edged up, leaving May crush down 4.5 cents at 276.50.

Bean oil drew continued support from anticipation of the EPA’s Renewable Volume Obligation announcement, with administrator Lee Zeldin indicating it would be released by month end. Meal continues to benefit from reported switching of South American meal shipments destined for Europe toward US-origin cargoes due to bunker fuel costs, though the extent and longevity of this shift remains debated.

The USDA announced a daily sale of 161,100 tonnes of soybeans to Mexico. Weekly soybean inspections of 1.1 million tonnes beat expectations but remain 27% below last year’s pace.

A USDA attaché forecast Chinese soybean imports for 2026/27 at 108 million tonnes, up 2 million on the prior year, though noted that reduced Chinese tariffs on Canadian canola could trim demand for competing oilseeds. China also eased rules around weed presence in Brazilian soybean cargoes.

Argentina continues to ship grains at a strong pace on the back of record wheat, corn and sunflower production, and is currently the cheapest overall FOB origin with best-value landed prices into Asia.

Brazil’s soy harvest was 66% complete as of March 19, slightly behind last year but near the five-year average.

ICE canola fell $7.40 to close at 719.10, dragged lower by the steep decline in crude oil though losses moderated through the session. MATIF rapeseed also closed lower.

The May canola contract managed to hold above its major moving averages despite briefly dipping below the 20-day average earlier in the session.

Volume was heavy at 92,760 contracts versus 52,492 on Friday.

Macro: AUD0.7020, Dow +631.00, Crude -10.19

The dominant macro story of the day was the sharp reversal in crude oil following President Trump’s social media post indicating that Iran had been given a further five days to negotiate before strikes on energy infrastructure would resume.

Brent crude swung more than $18 across the session before settling below $100 a barrel for the first time in nearly two weeks.

Trump described talks as productive and cited major points of agreement, and suggested the US and Iran could jointly control the Strait of Hormuz, saying it could reopen very soon. Iran flatly denied any direct negotiations had taken place, with state media saying the country had not responded to US requests for talks through intermediaries, and the Supreme Leader’s military adviser later stated the war would continue until all sanctions are lifted. Iran also continued missile and drone strikes on Israel, the UAE and Saudi Arabia through the session. The confusion and contradiction between the US and Iranian accounts created significant market volatility. Equities surged, with the Dow closing up 631 points, while crude’s collapse dragged the entire commodity complex lower before some recovery into the close.

The IEA noted that more than 40 energy sites across nine countries in the Middle East have been severely damaged, meaning supply disruptions are likely to persist even once the conflict ends.

Russia’s key petroleum export ports of Primorsk and Ust-Luga also suspended crude and fuel exports following drone attacks, adding a further layer of supply-side concern.

AgResource noted that while the Iran conflict has added a risk premium to grain markets, world grain oversupply has not changed, and the seizure of ocean freight markets with costs running 30-60pc above pre-war levels is already slowing global grain trade. The Australian dollar was essentially unchanged on the day.

Local: Southern EC deld markets were steady to start the week though liquidly remains terrible, growers struggling justify additional sales out of the bounds of what is needed by cashflow.

H2 Melb A$368/t, ASW1 Hanwood $340, ASW1 GV $340 NNSW/SQ markets were a little more interesting – they continue their charge towards $400 but fell short by a few $$ on both new & old crop. does a nice round number spur some sellers? not sure but a rain would…….

Everyone is doing their best to avoid the freight task as the top & tail on rates is extreme. WA forecast maps filling in a little more – just in time for sowing. Much of the wheat belt slated for 50-100mm which will be ideal.

HAVE YOUR SAY