Weather: Unfortunately the situation in NNSW and QLD is showing no signs of improving. The pattern about to hit WA is improving, southern east coast looks good but northern Aust is horrible.

I feel like the US has got worse with rain being taken out of KS/OK and Nebraska long range – additionally it looks like its getting hotter

Russia looks like it will get a drink but keep an eye on France as that pattern has turned dry.

Markets: Grains are a sideshow to energy, precious and equities at the moment. Food security hasnt caused any panic buying, margin compression is the order of the day with the supply chain absorbing much of the increase in energy… but for how long? The extreme views of the systemic damage this can cause can be rebutted to some extent if we look purely at the start of the Russia/Ukraine conflict. Predictions at the start of that war, i would argue, didnt materialise to the extent that was predicted. But, is this different. Just as the US looks like it is trying to get out of this, Saudi has said its keen to get involved. Additionally, the US is apparently getting a bunch of marines ready for action. I wonder how the growth in social media algorithums have changed how we trade this sort of thing – i mean, its a conflict – some one gets bombed, they retaliate – yet the capital flows dont match the fundamentals – my opinion – just confused is all.

Day Ahead – Australia: The fact the northern market forecast hasnt improved is a bigger driver than the war.

Rain in WA should keep new crop in check but, there is zero grower engagement with the uncertainty.

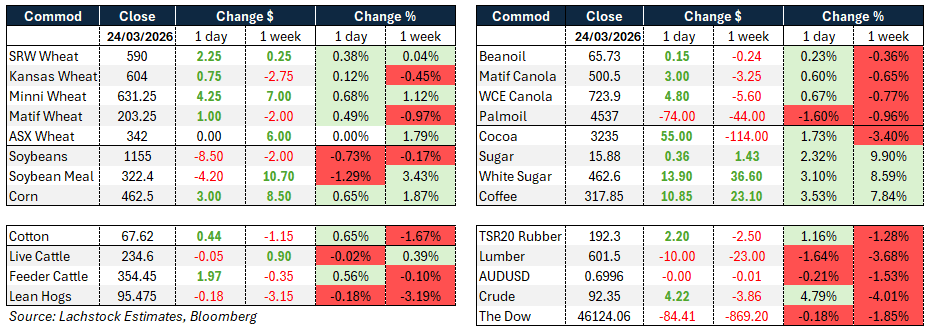

Global wheat: Chicago +2.25c, Kansas +0.75c, Matif +€1.00

Global wheat: Chicago +2.25c, Kansas +0.75c, Matif +€1.00

Wheat markets edged modestly higher on the day, with Chicago gaining 2.25c to 590, Kansas up fractions to 604 and Matif adding €1.00 to 203.25.

The market found intermittent support from deteriorating hard red winter crop conditions and a firmer crude oil complex, though gains were difficult to sustain.

A fresh bullish catalyst remains elusive, with Commstock Investments noting that while peripheral supportive factors exist, they are not sufficient to drive sustained day-to-day buying.

The HRW weather outlook is the key near-term focus. Conditions remain hot and dry through Friday, with late March and early April expected to bring greater moisture opportunities to the region. Confidence in the forecast is still low, leaving traders reluctant to take strong positions.

The USDA Prospective Planting report on March 31 adds a further reason to consolidate, with markets broadly in a wait-and-see mode.

The conflict in the Middle East continues to generate significant headline risk for wheat. Iran’s effective closure of the Strait of Hormuz is reverberating through the fertilizer complex, with Russia temporarily suspending ammonium nitrate exports from March 21 to April 21 to prioritise domestic spring fieldwork, and sulfur trading at an 18-year high as Persian Gulf supplies remain off the market.

Australian farmers are already responding ahead of winter planting, with some paring back wheat acreage and considering a shift toward oilseeds, pulses and barley, decisions that could weigh on global supply into 2027.

On the export front, EU soft wheat exports reached 17.1 million tonnes as of March 22, up from 16.1 million tonnes a year earlier, with Morocco, Egypt and Saudi Arabia the leading destinations.

MARS released its first EU 2026 harvest projections, forecasting soft wheat yield at 5.98 t/ha, down 5% from 2025, and rapeseed at 3.22 t/ha, down 3%.

SovEcon raised its Russian wheat export forecast by 1.1 million tonnes to 46.5 million tonnes for 2025-26, citing improving importer demand as the war adds to supply risks elsewhere. Jordan cancelled its wheat tender before issuing a new one with a March 31 deadline for June-July shipment.

Other grains and oilseeds: Corn +3.00c, Soybeans -8.50c, WCE Canola +C$4.80

Corn edged higher, with the July contract gaining 0.4% to $4.72 a bushel, supported by a firmer crude complex and continued managed money buying.

The market remains focused on the March 31 USDA Prospective Planting report, with the central debate around corn acreage. The bullish acreage argument centres on high fertilizer costs and availability concerns, though a meaningful portion of the market believes spring fertilizer was largely purchased months ago and is sceptical of a dramatically low corn number, noting growers’ tendency to plant through price signals.

Soybeans fell 0.7% to $11.70 a bushel, under pressure from expectations of a significant increase in US planted area in the upcoming report, as farmers are seen rotating away from corn due to input cost concerns.

Brazil’s harvest is just under 70% complete versus 80% at the same point last year, and March export volumes are running around 17.9% below last year’s pace.

China eased sanitary requirements on Brazilian soybean shipments, though the broader trade relationship with the US remains in focus ahead of the anticipated Trump-Xi meeting in mid-May.

The upcoming biofuels announcement is providing some support to the complex. The White House’s “Celebration of Agriculture” event Friday is expected to include finalised renewable volume obligations, with the broad market expectation that the outcome will be favourable for the biofuel industry. Agriculture Secretary Brooke Rollins confirmed the administration is moving quickly on blending standards. If lower corn acreage materialises, ethanol prices may need to rise to incentivise additional corn supply to refineries.

ICE canola closed higher, with the May contract up C$4.80 to 723.90, reclaiming a good portion of Monday’s losses. Support came from gains in crude oil, Chicago soyoil and Matif rapeseed, while weakness in Malaysian palm oil, Chicago soybeans and soymeal tempered the upside. Crush margins continued to improve, with the May position rising to C$296 per tonne above futures. Rising feed costs driven by the Iran conflict are weighing on Chinese hog producers already dealing with prices at 16-year lows, while West African cocoa and cotton farmers are facing a significant fertilizer shock heading into their planting season.

Macro: AUD0.7000, Dow -84.41, Crude +4.22

Crude oil was the dominant market mover, with WTI closing up $4.22 at $92.35, though the session was volatile. Prices surged on escalation fears before pulling back sharply late in the day on reports of a potential month-long ceasefire being discussed, a signal the market took seriously given the size of the crude reversal.

The Strait of Hormuz remains effectively closed, with Iran now charging transit fees of up to $2 million per voyage on commercial vessels, adding a further layer of friction to the world’s most critical energy shipping lane.

Diplomatic activity around the conflict intensified. President Trump indicated Iran had offered a goodwill gesture related to energy flows through the Strait, while simultaneously confirming the deployment of around 2,000 troops from the 82nd Airborne Division to the region. A 15-point US proposal was reportedly delivered to Iran via Pakistan. However, Iran’s parliament speaker denied any negotiations had taken place, and the IRGC described Trump’s comments as psychological operations.

Gulf states including Saudi Arabia signalled readiness to join the US-Israel campaign if their critical infrastructure is targeted, and Saudi Crown Prince Mohammed bin Salman has reportedly been urging Trump to continue the campaign to help reshape the region.

The US composite PMI fell to an 11-month low of 51.4 in March. The services PMI dropped to 51.1 as output, new orders and employment all softened, with employment falling into contraction. Manufacturing held up better at 52.4. The most concerning element was the surge in input and output prices, with composite output prices rising to their highest level in nearly three and a half years, reflecting the pass-through of higher energy costs. The initial adjustment appears to be flowing partly through margin compression rather than fully into prices, which has negative implications for growth and employment.

In the eurozone and UK, markets are now pricing around a 70% chance of rate hikes at the April 30 policy meetings.

Australia and the EU signed a long-awaited free trade agreement. Australian beef exporters secured 35,000 tonnes of tariff-free access, an eightfold increase from current levels, though well short of industry expectations. Sheep meat access was set at 30,850 tonnes, drawing sharp criticism given New Zealand holds 163,769 tonnes of equivalent access. The deal also sees Australia abolish its 5% import tax on European cars and raise the luxury car tax threshold for electric vehicles. It still requires ratification by both parliaments and faces a potentially difficult passage through the Australian Senate as well as opposition from European protectionist interests. Von der Leyen used her address to the Australian parliament to frame the agreement in the context of a broader strategic shift, warning that economic dependencies could be weaponised in the current global environment and calling on Australia and Europe to jointly respond to the consequences of China’s export-led growth model. The Dow fell 84 points to close at 46,124, while the Australian dollar was little changed at 69.96 US cents.

Local: Bids were steady across the board in the west of the country, with canola $750, wheat $329 and barley $335. New crop bids were $800, $355 and $330 FIS Albany.

Through the east, canola was $735, wheat $325 and barley $310, while new crop bids were $770, $355 and $313 track Geelong.

Lentil bids are sneaking higher, with deferred May/June delivery now pushing towards $700 into Geelong/Melbourne, though liquidity remains non-existent.

It remains slow going on the east coast, with growers gone to ground, if not below it. Apart from some cash flow selling, there is very little activity. Wheat is the hardest commodity to buy, with the trade carrying some barley length as growers were more willing sellers through harvest.

HAVE YOUR SAY