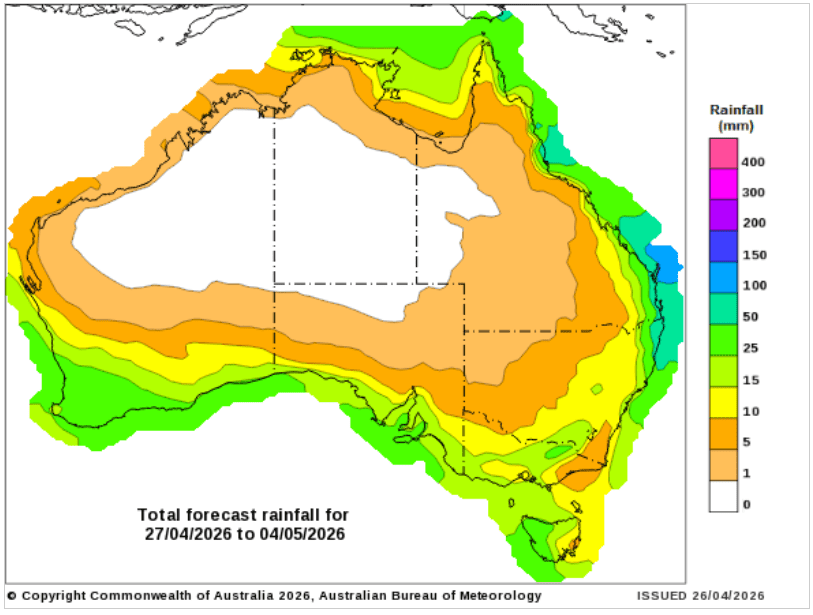

Weather: Draw a line from down the middle of the US – left dry and hot, right stormy and wet. The weekend weather stayed consistent the recent theme with western KS arguably too late now.

So your telling me there’s a chance…even the BOM has some rain in the 8-day forecast for pretty much the whole east coast – fingers crossed.

Markets

The idea that a sitting president has had 3 decent attempts on his life is just bonkers. The idea that the markets shrug it off is equally bonkers. The idea that Donald uses this to get his new ballroom finished is beyond bonkers.

The tin-foil-hat brigade will have a field day with this one, meanwhile, there is still a conflict in the Middle East without any signs of a resolution.

Energy markets ripped on Friday – Sing Gasoil one of the biggest movers. Gasoil markets have been harvesting souls over the last 2 weeks as the break caught energy bulls offside – now that stopout feels like it’s done, the market faces the reality of a fundamental supply issue.

Day Ahead – Australia

Boats moving from west to east, rain on the forecast but nothing hitting the ground yet – feels like we start the week on the defensive. Cash markets have been grinding higher, with the pull on the east coast filtering all the way down to Geelong/Melb.

Old crop canola has given the sticky longs an opportunity to exit – new crop grappling talk of rotation changes and global support from an energy perspective. I’m still waiting for Albo to pop up with a bio-mandate of some description – is bound to happen but an easy one to butcher.

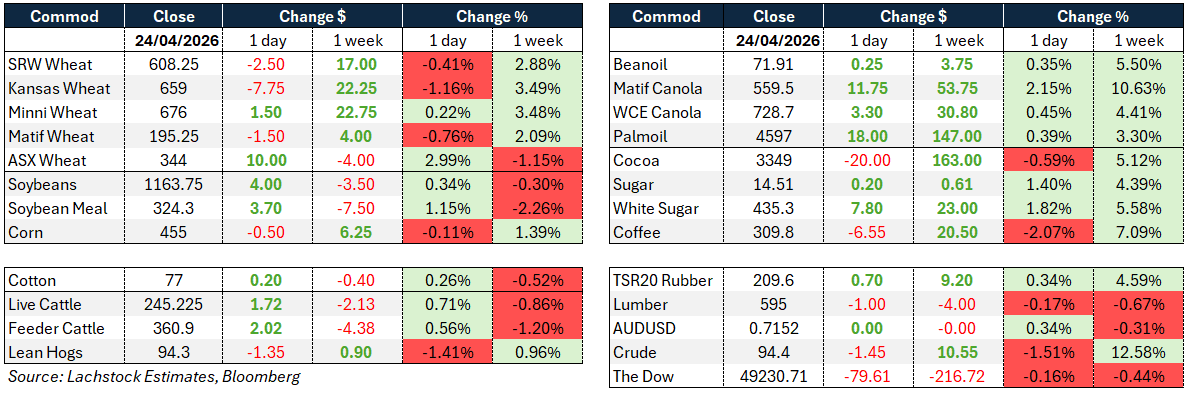

Global wheat: Chicago -2.50, Kansas -7.75, Matif -1.50

Global wheat: Chicago -2.50, Kansas -7.75, Matif -1.50

Wheat markets ran out of energy into the weekend, with profit-taking the dominant theme across the session.

Chicago and Kansas both slipped, though Chicago managed to outperform Kansas after the prior session’s surge in the latter. Minneapolis edged slightly higher.

In Paris, Matif continued to struggle for a bid, remaining well below corn on a feed value basis, though with North Africa in harvest mode the export demand outlook offers little near-term support.

Russian cash prices sit just above US$240/t, with IKAR trimming its 2026 Russian crop estimate to 90 million tonnes (Mt) from 91Mt, citing weather disruptions across Central and Volga federal districts, with export potential similarly lowered to 46.5Mt.

The IGC cut its 2026/27 global grain production forecast by 3Mt to 2.414 billion, leaving it below projected consumption of 2.437 billion, with the Middle East conflict cited as a key factor.

French soft wheat crop conditions edged down to 83 percent good/excellent from 84pc the prior week, though remain well above year-ago levels of 74pc.

India raised its wheat procurement target to 34.5Mt for the 2026/27 marketing year, up from an initial 30Mt.

US buyers have been sourcing milling wheat from Poland in recent weeks as they seek cheaper alternatives to elevated domestic prices.

Other grains and oilseeds: Corn -0.50, Soybeans +4.00, Matif Canola +11.75

Corn did very little on the day, finishing fractionally lower in nearby contracts while deferred months were barely changed.

The more significant corn story is in Europe, where June Maize on Matif surged €7.25/t to €209.75, its highest level in six weeks, as concerns mount over the impact of surging fertiliser prices on planted area in France and across Eastern Europe and the Balkans.

Dry conditions across the EU and a forecast for below-average precipitation over the next two weeks are compounding acreage concerns.

South Korea purchased around 67,000t feed corn in a private deal without an international tender.

In the soy complex, crush margins continued to extend to fresh highs, with the May crush settling at 340.75, up 7 cents on the day.

Soymeal led the complex higher on reports that some Brazilian shipments to Europe were encountering import difficulties, coinciding with a pickup in EU demand for US meal.

Soybeans themselves were largely range-bound, with the market’s next directional move seen as largely contingent on the outcome of the Trump/Xi summit and any implications for Chinese demand.

Canola on the ICE advanced, supported by firmer Chicago soyoil and Malaysian palm oil, despite European rapeseed trading lower.

Canadian Grain Commission data showed canola export volumes for the week ended April 19 at 138,200t, well below the prior week’s 284,100t, with cumulative marketing year shipments of 6.01Mt running significantly behind last year’s 7.52Mt.

Brazilian researchers are set to begin testing a potential increase in the biodiesel blend mandate to 20pc from 15pc, which would represent a meaningful demand uplift for oilseeds.

Forecasts for a strong El Niño event in the second half of 2026 are raising concerns about crop impacts across Asia, compounding existing supply-side pressures from the Iran war.

Macro: AUD 0.7152, Dow -79.61, Crude -1.45

The macroeconomic backdrop remains dominated by the Iran conflict and its implications for energy markets.

Despite crude finishing modestly lower on the day following initial reports of potential peace talks, the broader oil market tone is one of sustained elevation, with Brent trading near $107/barrel and WTI around $96 as the Strait of Hormuz blockade enters its third month.

Weekend peace talks in Pakistan were called off after Trump directed his envoys Kushner and Witkoff to stand down, with Iran maintaining it will not negotiate under threat or blockade.

The IEA has characterised the conflict as the largest supply shock in history, with over 37 vessels redirected and a loss of at least 1 billion barrels considered all but guaranteed.

The supply disruption is cascading through fertiliser markets, with CME Group raising margins on fertiliser futures for the second time since mid-March.

The Dow slipped modestly, and the AUD was flat on the day.

The White House correspondents’ dinner shooting in Washington over the weekend added a layer of domestic political uncertainty, with the suspect, a 31-year-old California teacher, due to appear in court Monday.

US-China relations remain a key watch item, with a Trump/Xi summit anticipated next month against a backdrop of tensions over AI intellectual property, Iranian oil sanctions on Chinese refiners, and competing responses to the Iran war among NATO allies.

Local: The week ended firmer in the west with canola A$800/t and new crop $826, wheat was $343 and $360, barley $346 and $333 FIS Albany. Through the east canola was $774 and $805, wheat $340 and $365, barley $314 and $332 track Geelong.

Some rainfall is on the forecast over the next 8 days, predominantly through WA, SA and Vic, with some for NSW and Qld — although not enough to move the needle, with general consensus that at least 50mm would be needed through NNSW and SQld to avoid a significant decline in planted area.

In other news, last week’s national beef kill surged to an 11-year high, with NLRS reporting 164,883 head for the week ending 17 April, up 26pc on the previous week and 37pc YoY, driven by dry-area turnoff through NSW and Qld, Easter backlog, and processors racing to fill China quota before tariff limits bite. While the reported female slaughter ratio was only 47.5pc, actual liquidation may be heavier than that suggests, with voluntary reporting likely understating both total kill and cow numbers.

HAVE YOUR SAY