Weather: US weather is officially a problem. Kansas NDVI went down over the past week – super unusual and shows how bad that part of the world is becoming. It’s dry and windy and really hot – not great if you are a wheat plant. Meanwhile the eastern corn belt is super wet, which will start to impact corn planting.

Markets: The CFTC data is backward-looking but tells us that Hard Red Winter has the biggest gross long it’s ever had, and near a record gross short; if you are simply looking at the net position you are missing that this is becoming a huge problem. If the situation deteriorates in the HRW belt and the massive short needs to get out, I’m not sure the long will be that obliging at US$6.30 per bushel; at $7.50/bu it might.

Day ahead in Australia: The diesel situation will be fasinating for the next few months – we have had a massive spike in demand, but what happens now? Will we see demand erosion with diesel above $3/lt in most parts of Australia. Fun fact: according to Petrol Spy, Daly Waters in the Northern Territory has AU$2.98-per-litre diesel. The Australian dollar dropping under 0.6900 is good timing, but with this much volatility, it’s doubtful the trade will show all of the currency move.

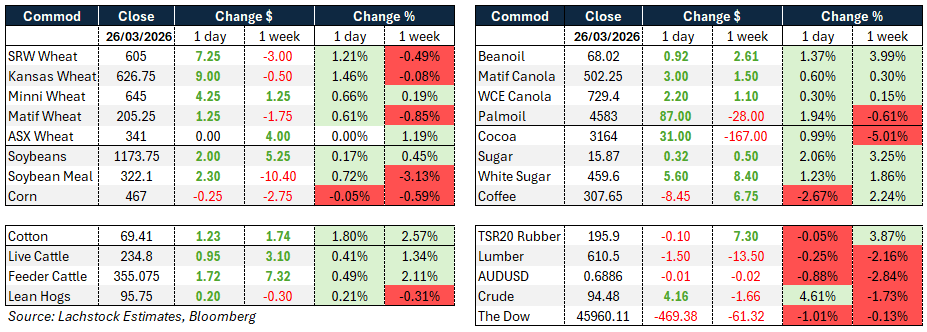

Global wheat: Chicago July +7.25c/bu; Kansas July +9c/bu; MATIF Wheat +€1.25/t. Wheat markets pushed collectively higher on Thursday, driven by deteriorating moisture prospects across key HRW growing regions. Weather forecasts that had previously shown meaningful rainfall for the southern plains were revised sharply, with precipitation chances now pushed further east and little relief expected for western Kansas and the Texas and Oklahoma panhandles through to April 9. The ongoing heat across HRW areas is compounding already building soil moisture deficits, leaving the market increasingly anxious. While there is still time for forecast maps to shift, the market is losing patience with each successive eastward nudge of the rain. Drought monitor data confirmed the trend, showing expanding areas of severe and extreme drought across winter wheat country. Implied volatility in Chicago July wheat rose to 37.45 percent from 34.78pc the prior session, reflecting elevated uncertainty.

On the demand side, weekly US wheat export sales of 397,000t comfortably beat expectations of 250,000t and were roughly three times the pace needed to meet the USDA’s projected annual target. Total all-wheat sales are already running at 98pc of the USDA’s full-year pace. Sales by class were led by HRW at 165,700t, followed by HRS at 103,600t, with The Philippines, Taiwan and South Korea the top buyers. South Korea also separately purchased around 65,000t of feed wheat in a private deal at approximately $276/t CFR, with Cargill believed to be the seller.

On the supply side, Morocco’s wheat harvest is projected to double to around 7 million tonnes (Mt) this season on improved rainfall, while French grain exports from Rouen surged to 374,000t in the latest week. An Algerian tender remains on the radar with details awaited.

Other grains and oilseeds: Corn July -0.25c/bu; soybeans July +2c/bu; WCE canola May +C$2.20/t. Corn markets were largely two-sided and subdued ahead of Friday’s expected White House agricultural policy announcements, with the nearby contract settling fractionally lower while the deferred December contract edged up 1.25c. The same themes that have dominated corn trading all week remained in play, including high fertiliser prices, potentially lower planted area both in the US and globally, elevated fuel costs, and broader inflationary concerns stemming from the Middle East conflict.

Weekly corn export sales of 1.218Mt tonnes were broadly in line with estimates and comfortably above the pace required to meet the USDA target. The pro-agriculture event at the White House on Friday is expected to include the release of the Renewable Volume Obligation, which traders anticipate will increase feedstock demand for both corn and soybeans, alongside a potential announcement on year-round E15.

Soybean markets were driven predominantly by the products, with bean oil surging ahead of the RVO release, while meal held firm on the back of strong export data. May soybeans settled up 2c, soybean meal gained $2.30 per short ton, and bean oil rallied 92 points, leaving the May crush margin up 13c to $2.83. Weekly soybean export sales of 669,000t and meal sales of 508,000t both well exceeded trade expectations.

The Trump-Xi meeting confirmed for May 14-15 in Beijing has rekindled optimism around a potential improvement in Chinese demand for US agricultural commodities.

ICE canola extended its rally into a third consecutive session, drawing support from strength in crude oil, MATIF rapeseed, Chicago soy oil and Malaysian palm oil, though the prospect of large ending stocks and a weaker Canadian dollar capped gains.

Some French farmers are reported to be switching from maize to sunflower plantings given lower input requirements, while Brazil’s soybean area outlook for 2026-27 has been clouded by rising fertiliser and fuel costs linked to the conflict. Malaysia is also moving to shore up fertiliser supply after import costs surged.

Macro: AUD/USD 0.6894c; Dow -469.38; Crude +$4.16. The dominant macro story remains the US-Iran conflict and its cascading effects on energy, inflation and global growth. President Trump extended his deadline for attacks on Iranian energy infrastructure by a further 10 days to April 6, citing ongoing talks that he described as progressing well, though Iranian officials and Wall Street Journal reporting suggested Tehran had not in fact requested the reprieve and remains undecided on how to proceed. Brent crude settled near $108 per barrel as markets remained unconvinced of a near-term resolution, and energy prices briefly pared gains following Trump’s social media post.

The OECD sharply lifted its inflation forecasts in response to the conflict, now projecting average G20 inflation of 4pc in 2026, up from its December estimate of 2.8pc, with the US expected to run even higher. The Dow fell sharply, down 469 points, reflecting ongoing uncertainty. The Australian dollar was largely unchanged on the day but has weakened notably over the past week, consistent with the broader risk-off tone.

Domestically, Australia’s economic outlook has been revised softer, with growth forecast at just 1.3pc in 2026 as higher inflation from both domestic pressures and the Middle East conflict weighs on consumption and investment. Inflation is expected to peak at 4.9pc in the second quarter of 2026, with the RBA’s trimmed mean target not expected to be reached until mid-2027. In the US, initial jobless claims rose modestly to 210,000, in line with expectations, with the labour market broadly stable though the pace of job creation remains weak. In the euro area, money supply and lending data pointed to ECB policy remaining modestly restrictive, with an April rate hike seen as unlikely.

Local: Through the west of the country bids were stronger across the board, with 2025-26 canola at A$765/t and 2026-27 at $800/t. Wheat was $332/t and $363/t, while barley was $335/t and $333/t free in store Albany. In the east, canola was $746/t and $780/t, wheat was $325/t and $358/t, and barley was $313/t and $318/t track Geelong. Lentils continue to work higher, with April forward now around $700/t delivered Geelong/Melbourne, as liquidity remains low and box margins slowly start to improve. There is some decent demand for ASW-type wheat through the south, with domestic consumers looking for more cover, but growers remain slow sellers.

HAVE YOUR SAY