Weather: Nothing really in the way of relief for the western part of the US wheatbelt but, now things are getting too wet in the east – this is an issue for SRW quality – early days but it will be traded.

Brazil corn is being affected by dryness, particularly in Paranà state.

Rain is building for this weekend on the east coast, good falls yesterday in southern WA.

Markets

Iran and Russia partnering up is a sobering development. Nothing official but needs to be watched.

The fact that Iran agreed to everything apart from discussions around nuclear should be a deal breaker for the US.

Gasoil rallied hard over the last few days – it has been a clear diver of terminal gate prices so I expect diesel to rally over the next week, despite Albo securing just over one days supply….

Day Ahead – Australia

With NSW off yesterday, things were a little quiet – back today with a sharply higher offshore and risk back on from a global commod perspective.

Not often i put a trade recommendation on here – but fill up today – diesel will grind higher over the next few days

.

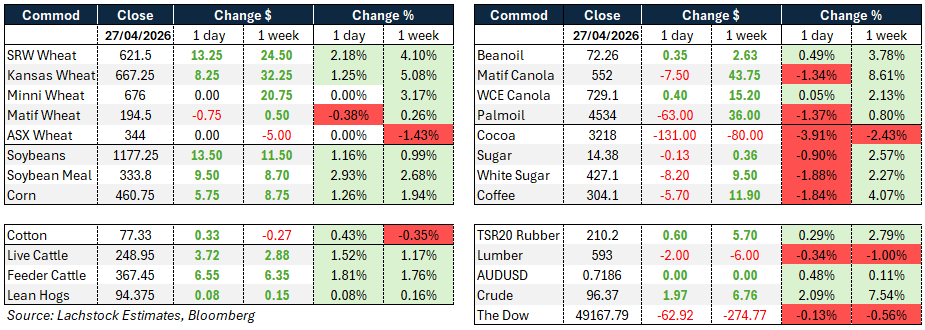

Global wheat: Chicago +13.25, Kansas +8.25, Matif -0.75

Global wheat: Chicago +13.25, Kansas +8.25, Matif -0.75

Wheat markets were underpinned by a combination of weather stress, geopolitical risk and supply-side concerns.

In the US, drought conditions across the central and southern High Plains continue to threaten the winter wheat crop, with large sections remaining extremely dry and wildfire risk elevated.

Kansas conditions slipped to 23% good to excellent with poor to very poor holding at 41%, and despite numerous forecast rain events in the southern plains, the driest areas continue to be bypassed.

Spring wheat planting came in at 19% versus trade expectations of 24%, a meaningful lag.

US wheat export inspections of 356,100 tonnes were up 12% year on year, a positive data point, while national winter wheat crop conditions were unchanged at 30% good to excellent, fractionally above trade ideas.

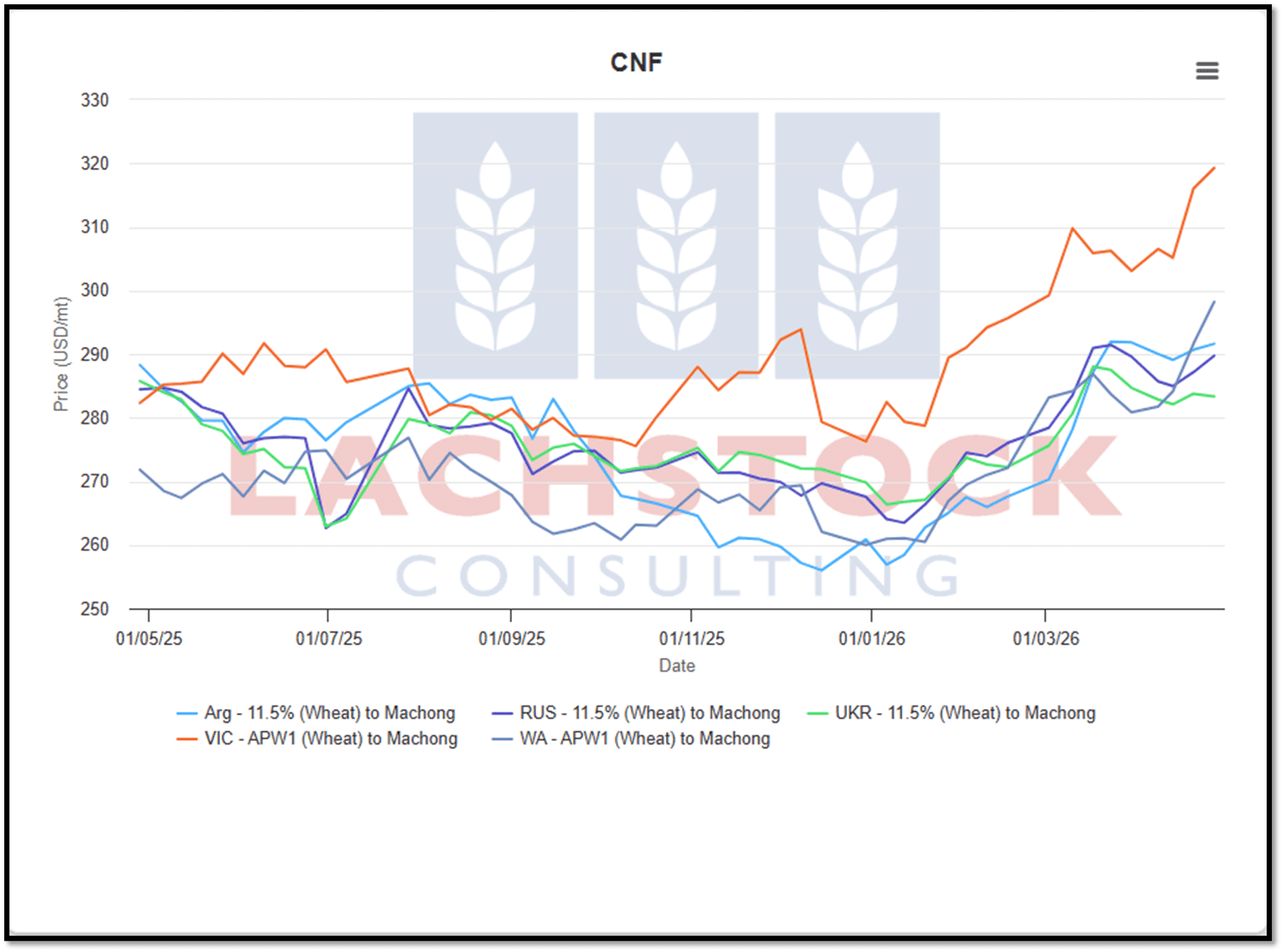

In Paris, Matif May slipped €0.75 while Russian cash was steady at $240.

The market tone was shaped heavily by the ongoing Strait of Hormuz closure, with participants increasingly resigned to a prolonged stalemate rather than a quick resolution.

Saudi Arabia’s purchase of 985,000 tonnes of wheat above the 710,000 tonne tender target was notable, with shipment deliberately routed through Red Sea ports to avoid the blocked strait.

India meanwhile offered a cautiously optimistic crop outlook supported by expanded planted area, though localised heat and hail damage in some areas tempered enthusiasm.

Fertiliser costs remain a significant overhang, with reports suggesting more than half of Middle Eastern urea output may have been disrupted since the start of the Iran conflict, adding a food inflation dimension to the geopolitical narrative.

European crop conditions were described as generally favourable with fair development across winter crops.

Other grains and oilseeds: Corn+5.75, Soybeans +13.50, Matif Canola -7.50

Corn markets were firm throughout the session with July gaining 5.75 cents and December adding 5.25 cents.

Global corn prices in China, Brazil and the EU are all near the top of their recent ranges, keeping US corn competitively priced and discouraging aggressive offers.

Safrinha concerns in Brazil around an abrupt shift to the dry season are absorbing attention that might otherwise have been directed at large Argentine yields.

Chinese domestic corn prices firmed, reviving hopes that US exporters could secure Chinese demand if the Trump/Xi trade dialogue progresses favourably.

In Europe, acreage fears and high input costs are the dominant narrative.

US corn export inspections of 1.64 million tonnes put the year-on-year pace up 31%, and planting progress came in at 25% versus the 23% expected, though cooler temperatures across a broad section of the country have raised germination concerns for the coming ten days.

South Korea purchased around 65,000 tonnes of animal feed corn in a private deal at approximately $263.58 per tonne cost and freight.

In the soy complex, meal led the session higher as chatter around Argentine GMO meal rejections by the EU continued to circulate.

July soybeans gained 13.5 cents, meal rallied $8.70 and July crush hit a fresh high of 317.50 cents.

The key question in meal is whether the EU maintains its position on the Argentine GMO strain or eventually concedes, with the consensus leaning toward the EU being slow to act, which would redirect more EU meal demand toward the US.

Bean oil continues to work through the RVO requirements while beans are being pulled higher by multiple supporting factors.

Soybean inspections of 628,900 tonnes were down 12% year on year, and bean planting came in at 23% versus 22% expected.

ICE canola was marginally higher, taking direction from crude oil and the Chicago soy complex, with European rapeseed and Malaysian palm oil also edging up.

The USDA’s Foreign Agricultural Service forecast Canadian canola production in 2026 at 20.1 million tonnes, down from 21.8 million the prior year, with increased planted area expected to only partially offset a return to average yields.

Malaysian palm oil retreated as sluggish demand from key markets and rising output weighed on prices.

Macro: AUD unch, Dow -62.92, Crude +1.97

The macro backdrop was shaped by the continuing Strait of Hormuz closure and its cascading effects on energy, fertiliser and food markets.

Crude oil added $1.97 on the day and is up 7.54% on the week, reflecting ongoing supply anxiety from the Middle East disruption.

Fertiliser prices are experiencing what analysts describe as a second surge in four years driven by the Iran conflict, with farmers globally rethinking planting plans given grain prices too low to absorb the additional cost burden.

Brazil is advancing a proposal to increase its mandatory ethanol blend in gasoline from 30% to 32%, a move its Energy Ministry says would achieve domestic self-sufficiency in gasoline production, while US ethanol producers are simultaneously lobbying Congress for year-round access to higher ethanol blends to combat elevated pump prices.

The Australian dollar was unchanged on the day. The Dow slipped 62.92 points, continuing recent softness, and UK retail sentiment deteriorated sharply, with the CBI April retail survey recording the sharpest drop in sales volumes in the survey’s history, with a net 68% of firms reporting volumes below year-ago levels against expectations of 40%, and forward trading expectations also weakening.

In agribusiness, Itau BBA flagged 10% growth expectations in its Brazilian agribusiness portfolio for 2026, citing the Iran war as simultaneously raising input costs and boosting biofuel demand.

Local: A public holiday for half the country yesterday, with only SA, Vic and Qld at the desk. Canola markets were softer following Friday night’s futures move, while cereals were firm to slightly softer to start the week, although there wasn’t enough trade to get a clear read.

Rainfall is still there and continuing to build on the forecast, with decent falls likely through WA, SA, Vic and SNSW over the next 8 days. Expect liquidity to keep improving as we get closer to the rain event, likely pressuring domestic markets lower.

WA is starting to follow the trend in east coast CNF pricing and beginning to look too expensive versus Black Sea and Argy offers. New business is likely to slow if that continues.

HAVE YOUR SAY