Weather: If it wasn’t bad enough in Kansas, temps are now predicted to spike with the majority of the state heading back above 30 degrees.

Some light rain forecast for the driest areas of Brazil but deficits are still building

Rainfall for Southern QLD and NNSW is still holding on, although amounts are well short of what is needed. Southern NSW rainfall forecast is sticking around.

Markets

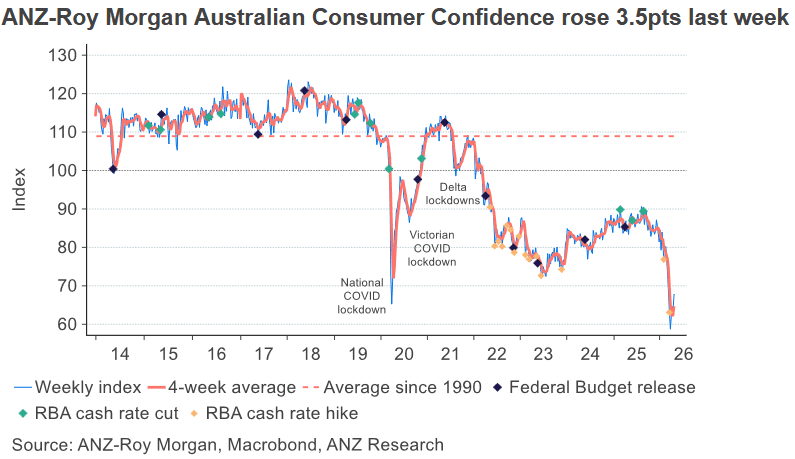

ANZ-Roy Morgan Australian Consumer Confidence rose 3.5pts to 67.8pts last week. The series is at its highest level since mid-March but remains among the lowest readings since the series began in 1973.

UAE exiting OPEC is an interesting one. Its a moot point in the short term, however, longer term it feels bearish. The catch is that there isn’t a lot of additional headroom. Most analysts and traders believed the UAE was already pumping at or very close to its maximum capacity before the war. So the incremental barrels may be modest in the near term, though Abu Dhabi has invested heavily in expanding capacity and has signalled its intention to boost output over the medium term once it is free of quota constraints.

Wheat markets have been a game of chicken for a long time – while the net position spec position has been not really exciting, the gross longs and shorts have been massive. Last week saw an exit – both sides. Which makes the rally interesting. Fundamentals should always win, eventually.

Day Ahead – Australia

A lot to digest. Rate rise seems a certainty post today CPI data. US crop situation is going from bad to worse. Global wheat balance sheets remain heavy but start to tighten next year. Asian demand has been normal without panic. Oh, and there is a war without resolution.

If you are in the north of the country, all of this doesn’t matter – its all about supply – with boats coming around and some relief in truck freight, solutions are being found, albeit slowly.

It feels bid today.

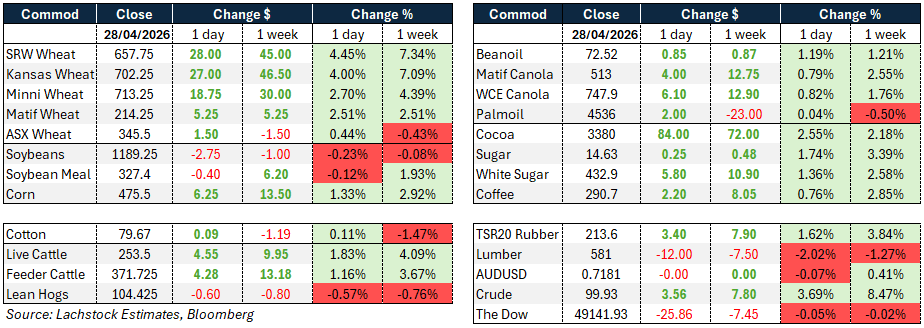

Global wheat: Chicago +28.00c (4.45%), Kansas Wheat +27.00c (4.00%), Matif Wheat +5.25 (2.51%)

Global wheat: Chicago +28.00c (4.45%), Kansas Wheat +27.00c (4.00%), Matif Wheat +5.25 (2.51%)

Wheat markets surged on Tuesday with Chicago SRW, Kansas and Minneapolis all posting strong gains, driven by deteriorating US winter wheat crop conditions and an increasingly concerning weather outlook.

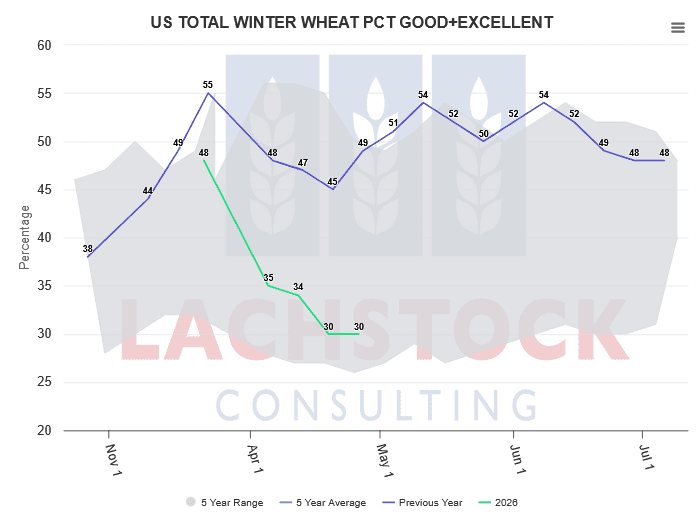

The latest USDA Crop Progress report showed only 30% of the winter wheat crop rated good to excellent as of April 26, pushing CBOT wheat to its highest level in nearly two years.

Dry conditions across key HRW growing regions are the primary concern, with some forecasters now cutting HRW production estimates well below 600 million bushels. Frost risk in the Nebraska region overnight added to anxiety.

The market has moved past hoping for rain and is now pricing in supply risk with conviction, implied volatility in Chicago wheat finishing at 34.62% versus 30.36% the prior session.

Many in the trade have HRW production pegged below 600 million bushels, with some balance sheets circulating as low as 550.

The pivotal HRW crop tour running May 11-14 and the May 12 WASDE will be key near-term catalysts.

Demand destruction remains a future talking point, though the market is not ready to trade it yet with the supply picture still unresolved. Spreads in Chicago were mixed while calendar spreads elsewhere were bid.

Other grains and oilseeds: Corn +6.25c (1.33%), Soybeans -2.75c (-0.23%), Matif Canola +4.00 (0.79%)

Corn followed wheat higher with both the July and December contracts gaining 6.25c, supported by strength in world markets and the broader wheat rally. US corn demand remains solid and a weather story is building in Brazil as some safrinha growing areas continue to dry, though light rains are beginning to appear in a few areas to watch.

The old crop/new crop spread was pressured on reports of the largest single day of old crop corn sales seen in weeks.

US corn remains competitive on a landed basis to Asia via the PNW, though that advantage has narrowed recently with Argentina still the cheapest overall FOB origin.

Soybeans were mixed with the old crop July contract slipping 2.75c while new crop November gained 1.25c.

The soybean meal market was quiet after its recent surge, with July meal down just 40c, while bean oil was firmer up 85 points and July crush finished at a fresh high of 328.75.

The market continues to watch whether China will step in for old crop beans before the window closes, with any progress on the Trump/Xi trade dialogue providing occasional support.

Bean oil remains structurally supported by biofuel mandate uncertainty, which continues to divert demand away from the product until the mandate requirements are clarified.

Tainted Argentine meal remains a source of potential volatility for EU consumers.

On the canola front, WCE canola gained with the first to second month spread narrowing, reflecting a firmer nearby tone.

US soybean planting is running well ahead of pace at 23% complete versus 12% this time last year, while corn planting is at 25% versus 22% last year, both significantly ahead of five-year averages.

Hedgepoint Global lifted its Brazilian soybean production estimate to 181 million metric tons, citing above-average yields across most regions.

Macro: AUD 0.7180, Dow -25.86 (-0.05%), Crude +3.56 (3.69%)

Crude oil continued to push higher, gaining 3.69% on the day, as the Strait of Hormuz closure continues to constrain Gulf supply and the UAE’s shock decision to exit OPEC added a new layer of complexity to the global oil market.

The UAE’s departure, effective May 1, blindsided fellow members and threatens to dilute OPEC’s ability to manage prices through supply adjustments.

The UAE had long chafed against quota constraints and was already producing at or near capacity, with the IEA estimating February output at 3.64 million barrels per day well above official figures.

While the immediate market impact is cushioned by the Hormuz shutdown rendering quotas largely moot, the longer-term concern is a potential domino effect and eventual market share competition once flows resume.

The Australian dollar was essentially flat on the day as markets look ahead to Wednesday’s Q1 CPI print, which economists expect will show headline inflation rising to 4.8% over the year to March, the fastest pace since September 2023.

The spike is driven largely by a 35% rise in petrol prices following the Middle East conflict.

Both NAB and CBA expect the RBA to raise rates by 25 basis points at next Tuesday’s meeting, taking the cash rate from 4.10% to 4.35%, though the decision is expected to be finely balanced given deteriorating consumer and business confidence.

The Dow was marginally softer, while US consumer confidence surprised slightly to the upside in April, with the Conference Board index rising to 92.8 from 92.2, beating expectations for a decline to 89.

The FOMC meeting outcome is due Wednesday morning Australian time, with the Fed widely expected to hold the funds rate at 3.50-3.75% as policymakers wait for clearer evidence that tariff-related inflation pressures are easing.

Local: WA bids were firmer, with canola at A$795/t and new crop at $830, while GM was $745 and $760. Wheat was $343 and $360, and barley $345 and $338 FIS Albany.

In the east, canola bids were stronger at $770 current season and $805 new crop, wheat was $338 and $365, and barley $315 and $332 track Geelong.

Northern markets remain firm, with Darling Downs May wheat and barley both bid around $440, while in the south Hanwood remains around $370 for nearby months.

Another strong month for barley exports to China is shaping up in April, with LSC estimating around 1mmt executed, which would make it the third consecutive month of 1mmt+ exports.

HAVE YOUR SAY