Weather:

Weather:

EU is baking – debate rages over what this means from a crop perspective – corn is being belted with estimates suggesting the crop will be at least 30% lower year on year.

Indian monsoon hasn’t caught up yet with the main wheat producing areas running 20-40 percent behind normal – one to watch

More rain on the way for southern Australia – areas like the Eyre Peninsula are running off the charts from an NDVI perspective.

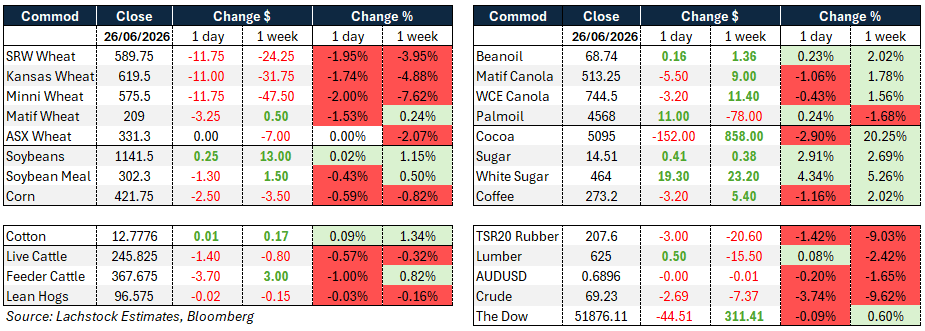

Markets

More military action over the weekend which gave energy a bid and underlines just how messy the path out of this thing will be. Its just baffling that there are as many as 80 sea mines bobbing around in the strait and one hasnt been hit yet. The environmental impact of an oil tanker going down is frightening.

Grain markets have zero concerns, a fact shared by the wave of spec selling. Grains are short, interesting set up, especially in corn with fresh shorts racing in despite rumours that China may reduce import tariffs on US products.

Day Ahead – Australia

The bleed continues with the next rain event building. This looks solid and stretches across the majority of the belt.

Canola should still find support with this energy bounce.

Wheat: Wheat stepped in a hole to close the week as WU sank 11.75c, KWU shed 11c and MWU gave up 9.75c, the board buckling under the weight of an advancing Northern Hemisphere harvest. Spreads told the story of harvest pressure — Chicago calendars were weak alongside Minneapolis, though KC bucked the trend with firm calendars. Implied vol in WU bled lower, settling at 25.92% against 26.95% Thursday.

Wheat: Wheat stepped in a hole to close the week as WU sank 11.75c, KWU shed 11c and MWU gave up 9.75c, the board buckling under the weight of an advancing Northern Hemisphere harvest. Spreads told the story of harvest pressure — Chicago calendars were weak alongside Minneapolis, though KC bucked the trend with firm calendars. Implied vol in WU bled lower, settling at 25.92% against 26.95% Thursday.

Across the pond Matif Sep was off €3.25 in a profit-taking mood and Russian cash slipped 50c to $231.75, the reality of a Russian crop pressing toward 90 mil tons now sitting right at the doorstep and emboldening the seller.

The final VSR observation wrapped up with the WN/WU running average at 71.66% of full carry, leaving the Chicago storage rate unchanged at 0.165, while the KWN/KWU average at 41.26% will see the KC storage rate contract to 0.165 on July 19.

There remains a counterweight to all of this — the European heat. France lost another 2% of soft wheat conditions to 74% good-to-excellent, still ahead of last year’s 68%, and with harvest now underway at 7% cut, what’s standing is largely what they’ll get; you can’t harm it much further from here.

In case you missed it, its warm in Europe – plenty of areas cracking 40 degrees and some. There will be some limited impact on winter crop but Corn will be belted by this.

Chicago SRW is suddenly net short 71k after piling on another 19.4k this week, and the market could badly use a China bid.

Next Tuesday’s acreage and quarterly stocks reports loom, with the trade leaning toward bearish numbers on both, particularly for wheat.

Other grains and oilseeds: Corn eased into the weekend as CN lost 2c and CZ slipped 1.5c, the middays backing off some of the oppressive heat seen the prior session.

The setup still has above-average temps blanketing the entire belt from this weekend through July 5th before the southeast cools and the northwest stays hot — a profile the crop can use so long as July doesn’t turn into a furnace, but the modelled July 5th breakdown was enough to inspire a poor close. As with wheat, corn is reluctant to commit ahead of stocks and acres; once the report clears it becomes a mad scramble for China headlines and the next forecast.

South Korea’s MFG booked an estimated 136kt of feed corn in tender.

The European corn picture continues to deteriorate — French grain maize conditions collapsed to an eight-year low at 76% good-to-excellent, down 8% on the week, with the French farm ministry flagging maize production potentially down around 30% on heat damage and reduced plantings, and growers suggesting losses could run deeper.

Despite the broad grain sell-off, Aug Matif maize managed a €0.25 gain.

Beans traded two-sided and finished modestly easier, SN off 1.25c and SX down fractions.

The product split favoured oil share — SMN lost $1.20 while BON tacked on 49 points, lifting July crush 4c to 333.50.

Palm found support as Malaysian futures firmed after Indonesia confirmed its B50 biodiesel mandate proceeds on schedule next month, the Sep contract up 40 ringgit to 4,597.

Two China threads ran through the session: persistent speculation that Beijing is on the verge of lowering tariffs on US ags — in the discussion, though the origin proved elusive — and the on-again, off-again Argentine strike, where yesterday’s “strike on” view softened to something less certain today.

Beans keep the China antenna up even as the oilseed weather window remains weeks away.

Macro: Crude went south again on Friday’s close but the weekend narrative flipped, with oil rising after reports the US and Iran agreed to stand down on strikes ahead of talks resuming this week in Doha — Brent jumping as much as 1.9% to $73.39 before paring, WTI back near $70.

The de-escalation follows several days of tit-for-tat: Iran struck a container ship Thursday, the US retaliated Friday and again overnight Saturday after Tehran hit a Qatari oil cargo, the VLCC Kiku left “not under command” off Fujairah carrying some 2 million barrels. The waterway stays fragile — the JMIC lifted its Hormuz threat level to “substantial,” the IMO estimates roughly 80 mines sit in the historic shipping lanes, and Oman has warned allies that transiting ships may ultimately face fees.

Vessels are again crossing via both the Omani and Iranian routes, though shipowners remain wary with hundreds of ships still penned in the Gulf. On the supply side, Putin acknowledged Russian fuel shortages and queues at the pumps, with a full diesel export ban among measures under discussion.

The reopening of Hormuz is easing the global fertilizer crunch — welcome news for Brazil heading into its new planting season.

On the policy front, Trump requested $11.1 billion in farm assistance, including $10 billion for corn, soybean and rice growers and $1.1 billion for Florida producers hit by winter storms.

The dollar enters the second half of 2026 on the front foot, buoyed by bets on higher US rates and persistent appetite for US assets, a backdrop that spells more pain for currencies like the Aussie. The Dow finished a touch softer at 51876, off 44.51.

Local: The week ended mixed through the west of the country with canola $800 and new crop $843, wheat $332 and $353, and barley $320 and $332 FIS Albany.

Through the east, canola was $758 and $800 for new crop, wheat $323 and $344, and barley $308 and $310 track Geelong.

Biblical rainfall fell across most of the east coast, with 50–100mm through NSW, 25–100mm in Victoria and 25–50mm across SA. The rain will be welcomed in most areas, although parts of SA and Victoria may become a little too wet – not a bad problem to have in what is shaping as a potential super El Niño.

It will be interesting to see whether grower liquidity changes heading into the new financial year later this week, particularly with some sizeable tax bills on the way.

HAVE YOUR SAY