Weather: Not a lot different today – hot in KS, TX about to be belted with rain – not sure thats going to help given harvest generally kicks off around the second week of May down there. Additionally, that crop is rated at 12% good to excellent.

70mm forecast for Rostov over the next two weeks – this will definitely build yield

Markets

Wheat ran out of buyers in SRW – but HRW remained bid. This makes sense if you are looking purely at the weather map and the crop conditions.

Energy was higher across the board – it certainly feels like we are being lulled into a false sense of security in Australia with the current Diesel supply situation – reading between the lines on Albo and Chris Bowen’s pressers – June looks tight. Additionally, Sing Gasoil has also caught a bid

Day Ahead – Australia

Firm – values in both old and new should still remain bid today – a combination of the northern drought pulling values higher, export commitments still being covered and general support through the “super El-Niño” talk.

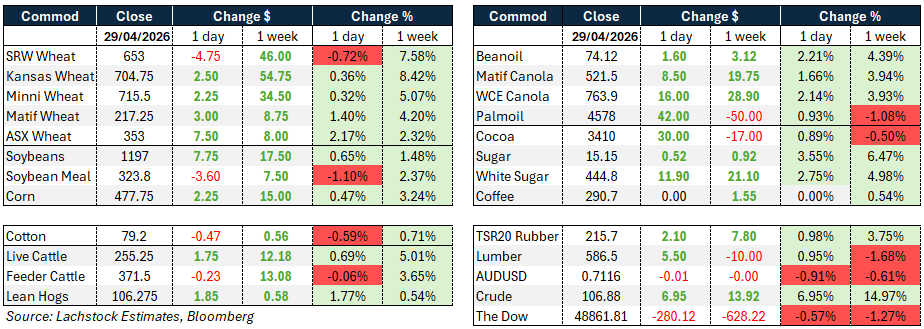

Global wheat: Chicago -4.75c, Kansas +2.50c, Matif +€3.00

Global wheat: Chicago -4.75c, Kansas +2.50c, Matif +€3.00

Wheat markets put in a volatile session, trading sharply higher early before fading into the close as profit-taking and poor demand expectations weighed.

Chicago July touched 671.50 before settling back at 653, down 4.75c, while Kansas City topped 718.50 before finishing at 704.75, up 2.50c. Matif September added €3.00, with Paris seen as cheap relative to other benchmarks and playing catch-up.

The early bid was driven by war risk premium and surging crude, with Trump reaffirming the naval blockade of Iranian ports and ruling out lifting restrictions until a nuclear deal is secured.

That inflationary sentiment faded through the afternoon, partly on the Fed’s rate decision which saw rates held but generated a notably divided vote of four dissenters, unsettling commodities broadly.

USDA attache reports projected Australia’s 2026/27 wheat crop at 29 million tonnes, down 19% on the year, and Canada’s at 36.16 million tonnes, down around 10%, both citing smaller area and a return to near-average yields following strong 2025/26 seasons.

EU soft wheat exports reached 19.28 million tonnes by April 24, up 6% year on year.

Russian cash remains just under $240.

Weekly export sales tomorrow are expected at 150,000 tonnes old crop and 100,000 new crop, and the market will be watching closely given last week’s weak result where durum exports outpaced both SRW and HRS sales.

Other grains and oilseeds: Corn +2.25c, Soybeans +7.75c, Matif Canola +€8.50

Corn posted modest gains, with July up 2.25c, continuing to follow crude and draw support from the safrinha weather story in Brazil, though the December contract made a new high for the move at 499.50 before easing slightly.

Planting progress is running well in the US corn belt with some drought-affected areas receiving helpful rains, and there was residual grower selling though nothing like the volumes seen the prior session.

Export sales tomorrow are expected at 1.45 million tonnes old crop and 250,000 new crop.

The market appears to have hit a wall around 600 on the December contract and will need a fresh catalyst, with worsening safrinha conditions the most likely trigger.

Soybeans firmed 7.75c as bean oil surged 160 points to a new high for the move, pushing July crush to 330.75c and making it very difficult to sell beans despite uncertainty around Chinese demand ahead of Trump’s planned Beijing visit.

Meal was the weak link, shedding $3.60 as large Argentine soybean deliveries to terminals pressured the product. EU soybean imports are running 10% below last year’s pace.

The Netherlands flagged banned GMO organisms in Argentine and Brazilian meal shipments, with Argentina pushing back on Dutch testing methods.

Taiwan’s MFIG bought 65,000 tonnes of US corn in tender.

Bunge beat first quarter earnings estimates, citing a recovery in processing margins.

Matif canola added €8.50, supported by the broader oilseed complex and palm oil strength, with Indonesian palm output potentially down up to 2 million tonnes this year due to El Nino dryness and high fertiliser costs.

Macro: AUD0.7115, Dow -280.12, Crude +6.95

The dominant macro story remains the US-Iran standoff and its deepening impact on global energy markets.

Trump confirmed he rejected Iran’s proposal to reopen the Strait of Hormuz, insisting the naval blockade stays until a nuclear deal is reached.

Brent crude surged above $119.50, its highest since June 2022, with WTI trading around $108. June crude settled up $6.95 at $106.88, the first time during the conflict that the front two months in crude both settled above $100.

The Fed held rates but the 4-3 dissent was the most divided decision since 1992 and sent equities and commodities lower into the close, with the Dow shedding 280 points.

The Australian dollar was little changed, slipping just one point to 0.7116. In Australia, the macro read is increasingly difficult, with annual inflation jumping from 3.7% to 4.6% in March, the highest in two years, driven largely by fuel costs which added around 0.8 percentage points to the headline figure.

Treasury is forecasting inflation above 5% by mid-year.

The RBA is now widely expected to raise rates for a third time when it meets next week.

Treasurer Chalmers is bracing for a multibillion-dollar budget blowout, with inflation-linked spending programs including the aged pension set to cost around $4 billion more than forecast.

The Bloomberg Agriculture Spot Index has climbed for a third straight month to its highest since November 2023, reflecting the breadth of commodity price pressure flowing from the conflict.

Local: WA bids were firmer, with canola at A$795/t and new crop at $830, while GM was $745 and $760. Wheat was $343 and $360, and barley $345 and $338 FIS Albany.

In the east, canola bids were stronger at $770 current season and $805 new crop, wheat was $338 and $365, and barley $315 and $332 track Geelong.

Northern markets remain firm, with Darling Downs May wheat and barley both bid around $440, while in the south Hanwood remains around $370 for nearby months.

Another strong month for barley exports to China is shaping up in April, with LSC estimating around 1mmt executed, which would make it the third consecutive month of 1mmt+ exports.

HAVE YOUR SAY