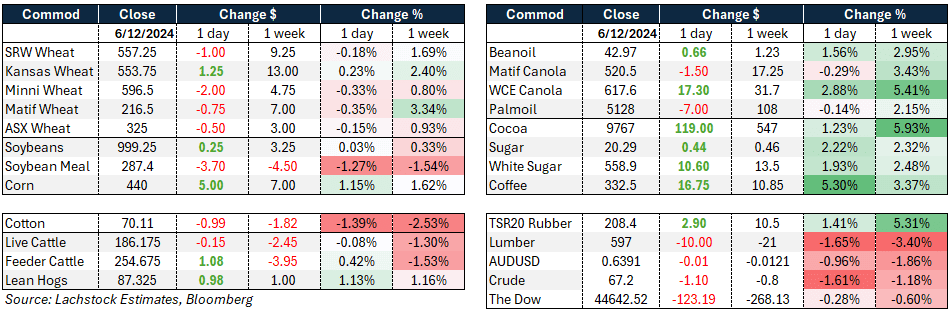

The day ahead

Weather – Rain on the east coast is now behind us (hopefully) with totals coming in below the more extreme forecasts. Having said that, over the past week, some areas saw falls greater than 100mm – so now it’s all about the impact. Nothing market moving globally, more of the same.

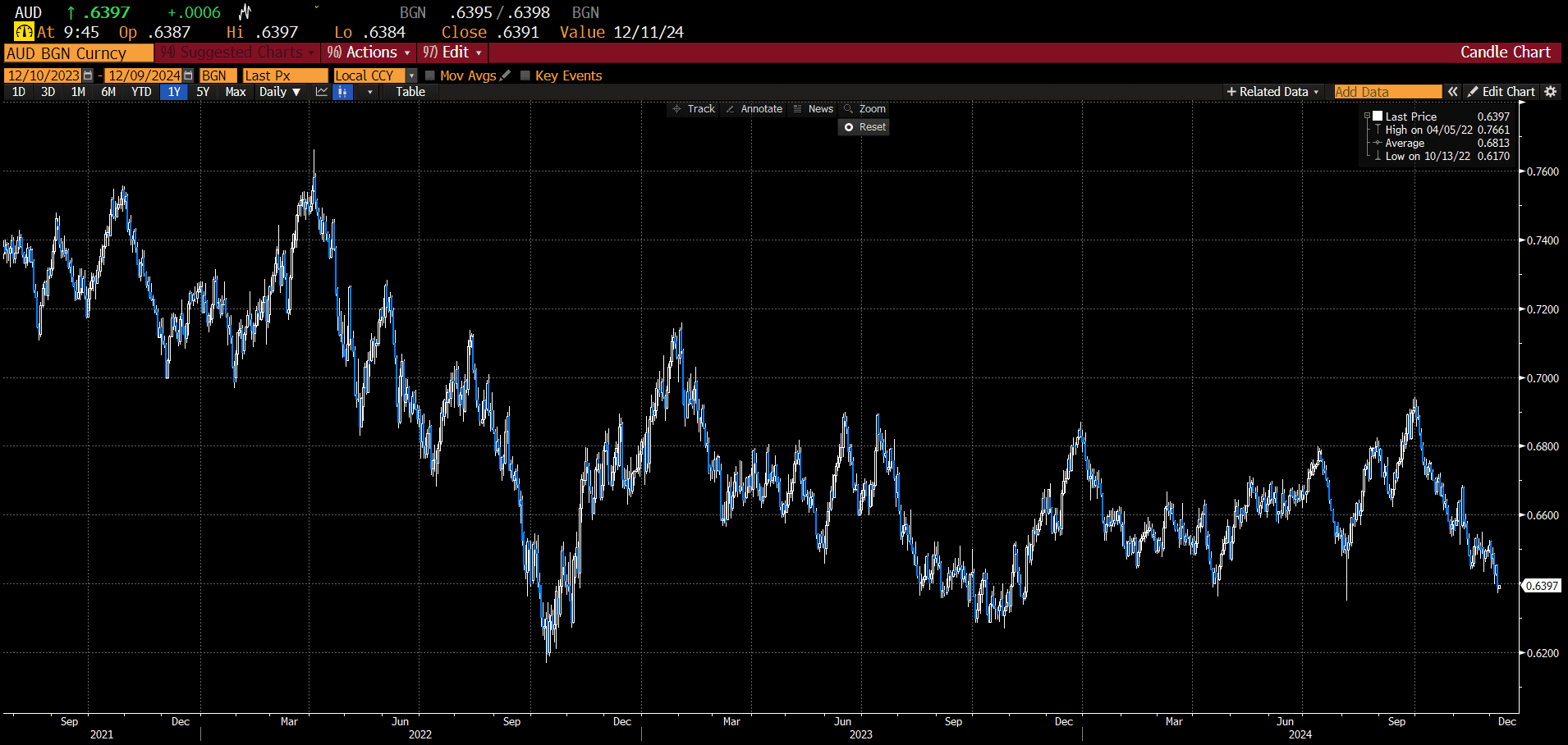

Markets – It was a bumpy week with futures and cash markets diverging. Russian cash was firmer over the week as the grind into the export quotas begins. From a futures perspective, Matif also outperformed its North American cousins. But, it was all about the AUD, finally breaking under the magical 0.6400 mark, printing its lowest level since Aug.

Markets – It was a bumpy week with futures and cash markets diverging. Russian cash was firmer over the week as the grind into the export quotas begins. From a futures perspective, Matif also outperformed its North American cousins. But, it was all about the AUD, finally breaking under the magical 0.6400 mark, printing its lowest level since Aug.

The Australian dollar eased below US64 cents. Source: Bloomberg in Lachstock Daily Market Wire.

Historically, the AUD does not hang out below 0.6400 for long so it will be interesting to see what the market thinks about this pull back.

Australian day ahead – Currency alone should keep the cash markets bid. From a wheat perspective, Russian FOB firming will also give the trade some confidence, particularly those with a tight balance sheet for Q1 2025.

Offshore

French wheat crop was rated at 86pc good to excellent, down 1pc for the week and slightly behind the 5-yr average of 88pc. Barley was rated at 83pc vs the 5-yr average of 88.6pc.

No more GASC. The role of importing wheat to Egypt now sits with the Agency for Sustainable Development according to a report in Reuters.

Russian wheat export tax is now at US$49.28/t, a massive jump as the govt tries to slow exports. The weak RUB contributing to the increase in the calculation.

The December WASDE will be out on Tuesday this week – some of the focus will be on both corn exports and ethanol production, both of which should go up.

Australia

In the west, canola bids finished the week stronger, with conventional bids around A$856 and GM at $750. Wheat was bid around $385, with barley at $329 in most PZs.

It was a similar story in eastern Australia, with canola bids finishing the week +$10, reaching around $790, and GM bids around a $100 discount. Cereals were largely unchanged, with APW bid at $345 and SFW1 around $311. Barley bids were around $307.

There were some heavy falls in isolated areas of NSW Central West over the week, where between 50-100mm fell in central parts, with dry conditions in the rest of the cropping regions.

Delivered Darling Downs for Jan+ remain around $318 for barley and $335 for wheat.

HAVE YOUR SAY