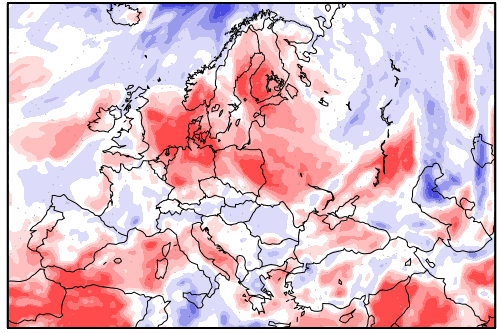

Precipitation forecast for Europe from May 7 to May 15, with red indicating driest areas and purple the wettest. Source: Wx Maps

MAY is the money month for Russian grain production, when the winter crop is made, and the spring crop planting campaign is set up. However, this season’s transition from the El Niño weather pattern to La Niña is sapping key grain-growing areas of critical moisture reserves, which could significantly reduce yields in the 2024 harvest.

There is a historical propensity for a blocking high-pressure ridge system to develop over western Russia in years when the El Niño influence subsides and is replaced with a La Niña weather pattern. And that is precisely what was dished up this spring, resulting in parts of Ukraine, and most of southern Russia and western Kazakhstan receiving less than 50pc of their average monthly rainfall for both March and April.

According to Drew Lerner from World Weather, the ridge has now moved on, but he expects it to return by the end of this month and dominate this season’s summer weather patterns over Russia. Some helpful moisture could arrive before the ridge re-establishes itself, but then it will turn hot and dry, and that is likely to result in varying degrees of yield reduction for both the winter and spring cereal crops. “The infamous drought in Russia of 2010 was a byproduct of this same environment,” he said. “That was a really nasty year”.

The worst years tend to occur when a strong ridge sets up over the west of the country’s wheat growing region. However, there have been other El Niño-to-La Niña transition years, such as 1988 and 2016, when the ridge was weaker and set up further east. The ensuing yield impact was not nearly as pronounced in those years.

Dry south, troublesome temps

The southern wheat growing regions, which account for around 30pc of national production, are extremely dry at the moment, and the forecast for the next couple of weeks holds very little joy for the region’s farmers. While some scattered showers are on the horizon, they are not expected to be nearly enough to erode the severe moisture deficits and restore the early spring production outlook. In many parts of southern Russia, it was the driest April in more than ten years, with rainfall barely 25pc on the April average.

April temperatures were also at, or near record levels across most of southern Russia, averaging 5.4 degrees Celsius above the long-term mean. However, there is expected to be some respite in the first half of May, with the average to below-average temperatures providing a window of opportunity for much needed precipitation and slowing the yield loss impact of low soil moisture reserves. However, the reprieve will be short lived with a return to above-average temperatures expected later in May. Historically, Russia’s best overall wheat production years generally occur amid cooler Mays in the south.

With a cooler forecast comes the risk of overnight temperatures being cold enough to raise freeze concerns, particularly in the more northern winter cropping regions. Over the weekend, temperatures across parts of the Volga region dropped below minus 4 degrees Celsius. With the crops up to three weeks further advanced than normal and already in the jointing crop stage, temperatures of that magnitude are right on the damage threshold. Further south in the Krasnodar region, sub-zero temperatures were recorded at ground level over the weekend, which could be quite problematic for wheat production as much of the wheat crop in that part of Russia is now at the flowering stage.

Price driver

As the world’s largest wheat exporter, Russia’s production and exportable surplus significantly influence international prices. After two consecutive bumper wheat harvests, Russia has been exporting record quantities, flooding the market with cheap grain and progressively pushing global prices lower. Consequently, global grain markets focus heavily on Russian weather at this time of year, and this will only intensify the longer the dry weather lingers.

The concern around possible damage to the Russian wheat crop has been a major price driver over the past two weeks. Some isolated showers over the parched regions early last week momentarily teased futures markets, but the registrations were disappointing, and the recent bullish trend was restored in trade last Thursday and Friday.

July wheat on the Chicago Board of Trade finished Friday up 2.8pc to close a tad above the previous week’s close, reinforcing the recent weather rally. The contract has now increased 12.6pc since markets opened on April 19. Matif milling wheat futures have reacted similarly to the crop issues emerging in Russia and the EU, with the September contract rallying 9.6pc over the same period.

Russian wheat production estimates have begun to decline as the weather outlook remains hostile and the moisture deficits grow. Leading Black Sea market analyst SovEcon was the first to move, cutting its 2024/25 output estimate on April 19 from 94 million tonnes (Mt) to 93Mt. Agricultural consultancy IKAR waited until late last week to make the move, trimming its wheat harvest forecast from 93Mt to 91Mt and its total grain production forecast by 4Mt to 142Mt. The USDA always tends to be conservative with its Russian crop estimates and currently sits on 91.5Mt, with its May update due to be released at the end of this week.

On the export front IKAR now expects Russia to export 64.5Mt of grain in the 2024/25 marketing year (July to June), including 50.5Mt of wheat, down 3.5Mt and 1.5Mt, respectively. The USDA mysteriously increased its new crop Russian wheat export projection by 1Mt to 52Mt in the April update, pegging it at 24.4pc of total global wheat trade. It will be interesting to see if the USDA reacts to the evolving production and export concerns in this week’s report or pushes the can down the road for another month.

With the southern Russian crop now in the critical reproductive phase and weather forecasts showing minimal rainfall through to at least May 20, the risk of more dramatic revisions to production and export forecasts is mounting. Average to below-average precipitation for the southern Russian wheat belt for the balance of May will simply not cut it, given the moisture deficits accumulated so far this spring.

HAVE YOUR SAY