While picking of Darling Downs cotton can start in March, it is a long way off for this crop at Nobby and many more like it. The market for nearby cottonseed has rallied as a result. Photo: CottonInfo

PRICES for feedgrain in southern markets have eased a few dollars in the past week but firmed in the north, as sorghum harvesting and sales straight off the header dampen selling interest in white grains.

ABARES has this week released its forecasts for 2023-24 wheat and barley production, and the numbers are in line with expectations.

Amid forecast drier conditions, area planted to wheat is estimated by ABARES to decrease from 13 million hectares in 2022-23 which yielded 39.2Mt to 11.8-12.5Mha producing 28.2Mt.

Barley area is expected to drop, but to a lesser degree than wheat, to produce 9.9Mt million tonnes, down from 14.1Mt in the harvest just gone.

On exports, ABARES forecast wheat at a record 28Mt in 2022-23 and 22.5Mt in 2023-24, while barley is seen at 8.7Mt of current crop, or 2pc below the record set in 2016-17, and 5.8Mt of new crop.

Growers across southern Australia are starting to plant oat and dual-purpose canola and cereal crops in mostly dry conditions, while in northern Australia, flooding has stemmed the flow of cattle into feedlots to temper near-term demand from that sector.

| Today | Mar 2 | |

| Barley Downs | $408 | $405 |

| SFW wheat Downs | $410 | $405 |

| Sorghum Downs | $425 | $430 |

| Barley Melbourne | $365 | $370 |

| ASW Melbourne | $420 | $430 |

| SFW Melbourne | $418 | $425 |

Table 1: Indicative prices in Australian dollars per tonne.

Northern

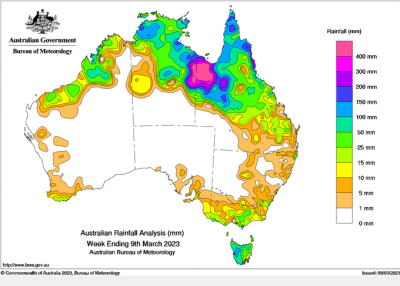

While parts of northern Australia have received torrential rain in the past week, little has fallen on grain-growing areas, and this has allowed the sorghum harvest to advance at pace.

Parts of Central Queensland including Emerald on 23mm and Clermont with 52mm have had significant rain in the week to 9am today, which is perfectly timed for recently planted sorghum.

GrainCorp’s Qld regional operations manager Brad Foster said in a video posted today that the southern Qld’s sorghum harvest was about halfway through, with 180,000t in the network so far.

He said CQ’s sorghum harvest was expected to start in late April and run into July-August.

Smithfield Cattle Company commodity buyer Brett Carsburg said the buying has been thin as the feedlot sector in particular waits to see how long recent rain across parts of northern and central Australia will impact the supply of feeder cattle.

“A lot of feedlots have already covered their grain requirements for cattle on feed, and they’re not advancing too far out,” Mr Carsburg said.

“They want cattle prices to go down, but with this rain…occupancy will be a bit lower than expected for the next 30 days.

“I’d expect feedlots to be a bit conservative until they see weather fining up and cattle coming in from the north.”

Image 1: Heavy to torrential rain in parts of Qld and the NT is limiting the supply of cattle available to feedlots, and tempering their demand for grain in the short term.

Mr Carsburg said grower interest in selling wheat and barley in the northern region has fallen away with the sorghum harvest.

“Growers who had grain to sell to open up space for sorghum have done that already.

“The growers now who’ve got white grain are hanging on to that until they can see an increase in soil moisture.”

Topsoil in northern New South Wales and southern Qld is mostly dry, but sitting atop a full subsoil profile.

With concerns about dry conditions taken hold below the tropics, Mr Carsburg said growers were hanging on to wheat and barley in case supply gets tight and the northern domestic market rallies as a result.

“Growers who have white grain now are using it as insurance.”

In the cottonseed market, current-crop prices have rallied around $15 in the past week to $505/t delivered Downs, around $40/t over new crop.

The lateness of the cotton crop, combined with already tight current-crop stocks is behind the rally.

“There are limited sellers of old crop, and with ginning slightly delayed, it could be difficult to secure.

“Old crop’s got to roll into the first three weeks of April.”

Port demand subdued in south

Values for feed wheat and barley have softened in the past week as export focus shifts to milling wheat, and up-country demand dominates the feedgrain space.

Key Agri broker Matt Noonan said APW and H2 wheat was sitting at around $20/t over ASW-type wheat, and attracting much of the trade’s interest in warehoused grain.

“A good chunk of wheat that went into the system was APW or better.

“Early on, (the trade) targeted feed grades, but over the past month and a bit they’ve transitioned to more demand for APW or better for export.”

Lower protein wheat in southern NSW is largely going to domestic consumers, who are feeling the impact of reduced supply from the Lachlan and Macquarie valleys which were hard hit by flooding last year.

“From a farm gate level, it hasn’t worked to go south into Melbourne with that grain, even though freight rates have come off a little bit.”

Apart from yesterday’s derailment on a branch line west of Junee, the NSW rail supply chain is said to be working very well, with mostly canola and milling wheat heading in wagons for export.

Mr Noonan said growers were keen to sell warehoused canola rather than feed wheat or barley on spikes in the market.

Grain Central: Get our free news straight to your inbox – Click here

HAVE YOUR SAY