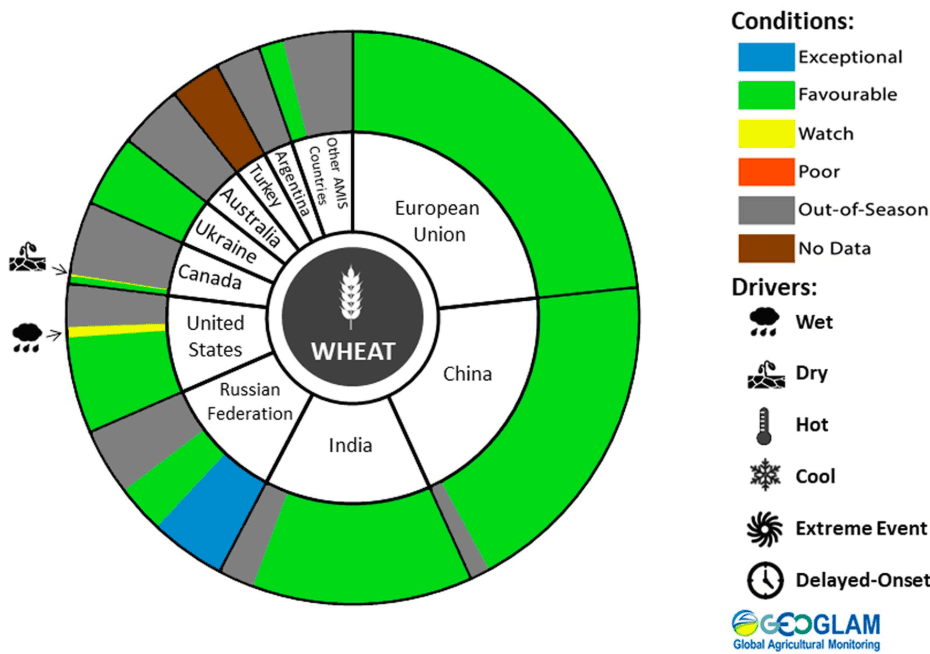

EUROPEAN Union winter wheat conditions are generally favourable, but additional rain is needed in southern Europe in the coming month, according to the Agricultural Market Information System (AMIS) April 2019 market monitor.

AMIS also reports that, in Ukraine, a very warm start to March has led to winter wheat growth being two to three weeks ahead of normal, which tends to be a positive factor for final yields.

In the Russian Federation, winter wheat conditions are off to an exceptional start in the southern region, while areas further north remain in dormancy under favourable conditions.

In China, conditions for winter wheat are generally favourable as warmer than average weather is bringing the crop out of dormancy earlier than normal.

In India, winter week is progressing towards maturity stage under favourable conditions. Total sown area area is in line with the previous year.

In the United States, winter weight conditions are favourable in the main producing area of the southern Great Plains. Further north, in Nebraska and the Dakotas, very wet and snowy conditions are raising concerns.

In Canada, winter wheat conditions are favourable for the dormant crop in the main producing provinces. However, delays in sowing in the fall, along with an increased risk of winter kill, may reduce production in the southern Prairies.

Wheat-producing countries’ conditions rating, pie chart indicating share of world production. Source: GEOGLAM crop monitor

Price indices drop

AMIS reports that global export prices mostly posted solid declines during March.

Pressure continued to come from ample nearby supplies and a generally positive outlook for the next world harvest.

The pace of US exports continued to disappoint traders, and this contributed to price weakness for US winter wheats, but US spring wheat export values rose as wintry weather fostered ideas that seeding of the 2019/20 crop could be delayed.

EU prices were supported by accelerating exports, including recent sizeable sales to Egypt, Algeria and Saudi Arabia, while, towards the end of month, new season prices were underpinned by concerns about a dry outlook for some EU crops.

Tightening export availability is buoyed spot quotations in the Black Sea region.

Wheat prices declined more than 9 per cent during March, owing largely to lacklustre demand for US wheat.

Continued foreign competition drove wheat prices to a one-year low, before rebounding on adverse US weather developments.

Exogenous markets were stronger, the US dollar was stronger and crude oil — West Texas Intermediate — traded 33pc higher since the end of 2018.

Following release of the USDA stocks and planting intentions reports at the end of March prices fell for grains and oilseeds, maize declining by about 5pc.

Investment flows sa managed money establish large shorts, of which maize set a record net short of over 283,000 contracts by mid-month, equivalent to 36 million tonnes. Positions were moderately reduced prior to the USDA reports’ release.

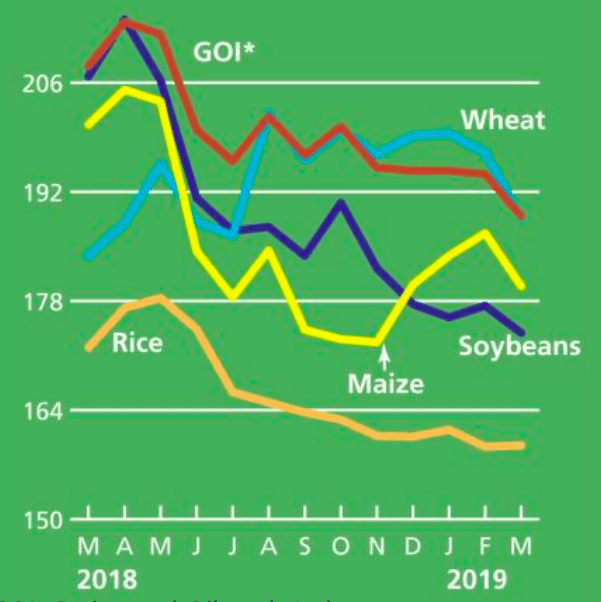

IGC commodity price indices. Wheat (blue line) price index has declined heavily over February and March.

Index base, January 2000 = 100. GOI* grains and oilseeds index. Source: IGC

(click to enlarge)

Source: AMIS

The above is an extract from the AMIS April 2019 market monitor published this week. It covers international markets for wheat, maize, rice and soybeans. This extract relates to wheat only. To read the complete edition click here.

HAVE YOUR SAY