Grains Australia CEO Richard Simonaitis speaking at the 2026 GRDC Perth Update.

BIOFUEL is shaping demand for Australian grain exports, both directly from Europe on canola, and indirectly for feedgrain from South-east Asia, Grains Australia chief executive officer Richard Simonaitis said.

Speaking at the Grains Research and Development Corporation Research Update in Perth last week, Mr Simonaitis outlined the importance of the EU canola market to Western Australia, and opportunities for feedgrain as noodle wheat demand flattens.

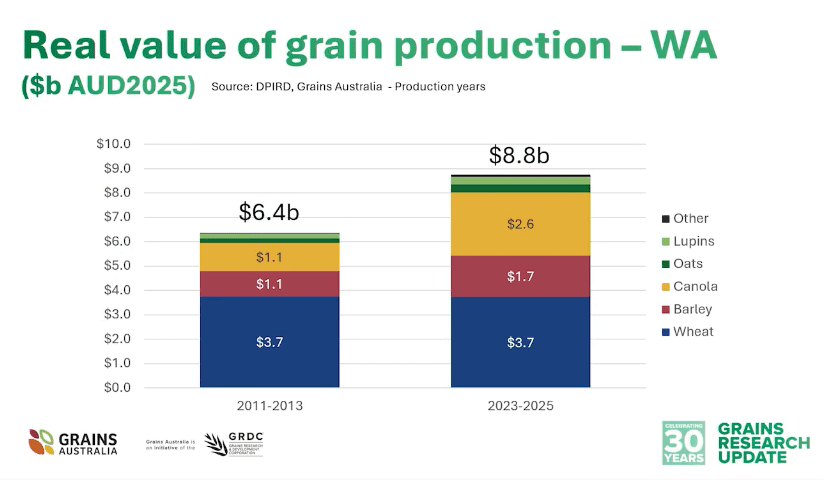

He stepped through “about a 30pc increase in value over the last 10 or 12 years” for WA grain exports.

“That happens when you’ve got a robust R&D climate, when you’ve got a world-class breeding program, and when you’ve got innovative farmers who will adopt the practices that were developed in world-class R&D,” Mr Simonaitis said.

With trade and market access being one of GA’s key functions, Mr Simonaitis spoke about both the EU canola market and selected Asian wheat markets.

“We’re seeing our highest-value market for canola into the EU for biofuels, and we’re seeing 120-130 million tonnes a year of US corn going into ethanol, which is leaving a gap for us in the South-east Asian feed market.”

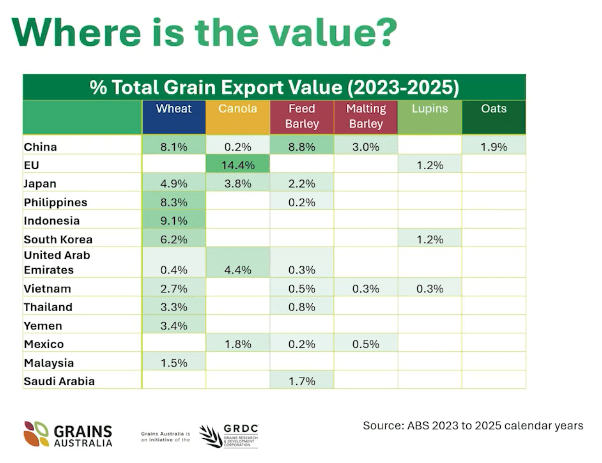

He said energy policy in affluent countries, namely the EU on canola which accounts for the largest chunk by value of WA grain exports from January 2023 to December 2025, was also significant.

“There’s a tension there, if you like, between increasing feed markets opening up at the lower end of quality, and premium markets in energy.”

Noodle demand flattens

Grains Australia is this year absorbing the functions of the Australian Export Grains Innovation Centre.

Sharing insights from AEGIC’s relationship with some export customers, Mr Simonaitis said indications are that feedgrain is picking up demand in South-east Asia.

“In the milling grades, growth is going to continue, albeit organically.

“The feed markets are growing much quicker than the noodle market.

“Those feed markets are growing rapidly.”

US corn is the feedstock for US ethanol production, and the traditional input for animal feed in Asia.

Mr Simonaitis said Australian wheat was competing with US corn in the South-east Asian feed market as consumers looked for animal rather than grain protein in their diets.

“Our low-protein…wheat is pricing very well into their feed market.

“People in South-east Asia want to eat meat as they’re getting richer.”

Broad buying from Vietnam

Australian Bureau of Statistics data for the marketing year to September 2025 show Vietnam was Australia’s fourth-biggest market for both boxed and bulk wheat, on 240,251 tonnes and 1.37Mt respectively.

“It’s our only true bread market, and they will pay for the quality that they need.

“They’re a consistent APW buyer, and they know that using our wheat is going to give a golden crust and a fine crumb structure in that banh mi market.

“They are also an opportunistic buyer of feed wheat out of Australia.

“We’ve had a bit of a tariff benefit there versus other origins like Russia, and they will buy Australian wheat into their feed market.”

Scope in Indonesia, decline in Japan

Indonesia, Australia’s third-biggest boxed market in 2024-25 with 264,165t and biggest bulk destination on 3.96Mt, also offers further opportunity on top of its 3-4.5Mt annual demand.

“We would like to get more feedgrains into Indonesia.

“There’s some constraint there with the deal that was done in our most recent free-trade agreement with Indonesia.

“There’s a lot of diplomatic effort there, a lot of business-to-business effort, but there’s opportunities still in front of us.”

On higher-protein wheat, Indonesia appears to be looking to Canada.

“They are buying some Canadian wheat to give a bit more strength to their noodle products…and their bread lines.”

Mr Simonaitis said Japan’s market for noodle wheat was in “very slow decline as their population ages”, but was highly valued as WA’s “only true niche market for wheat nationally”.

“Japan is always at the premium end of the market.

“We’ve got programs to try and develop Japanese-style noodles in more open markets, like China and Indonesia to get a bit more competition [and] underpin the demand side to give our growers a bit more confidence in planting ANW varieties in WA.”

Millers embrace technology

Mr Simonaitis indicated that millers in key customer nations were embracing technology that enabled them to get better performance from wheat that did not necessarily carry the quality hallmarks of Australian cargoes.

“Flour-milling technology used to be that if you wanted to get a product type out of a flour mill, you needed to put something in at the front end to make that happen.”

Mr Simonaitis referenced the work of AEGIC’s Dr Ken Quayle around 2020 with Indonesia’s Wilmar-owned PT Pundi Kencana, one of the world’s largest flour millers.

“They were saying that…historically, they’ve bought wheat from nine different origins.

“Now they’re buying just from three origins, so 40-45pc Aussie, maybe 15 or 18pc Canadian for a little bit of extra protein, and then some cheap filler wheat from somewhere else in the world.

“They’re better able to manage through control systems, through blending tools inside the flour mill, through technology, so these things are all pressures on our supply.”

China markets vary

China is WA’s, and Australia’s, biggest barley market, and behind Indonesia and The Philippines was its third-biggest wheat market in the 2023-25 calendar years.

Following an issue over the blackleg disease, China closed to Australian canola in 2020, and ABS data indicates it reopened with a WA cargo which sailed in November last year.

“The access to canola is just starting to open up again as we get a little bit of comfort around disease management and a more liberal interpretation of how we apply the foreign material.”

Mr Simonaitis indicated that exports of wheat to China may slow as its reserves build from 85Mt in 2020 at the rate of 3-4Mt a year.

“They’re pretty much full in their government reserves program.

“Globally, there’s close to 280Mt of ending stocks at the moment, and China has got capacity for 125M, and right now they’re sitting on about 123 and a half.”

FTAs no silver bullet

While Australia has bilateral trade agreements in place with all the above-mentioned Asian customers, Mr Simonaitis said the nature of trade meant competitors would seek to replicate any benefits therein.

“The benefit of our free-trade agreement activities will degrade over five to 10 years and we’ll start to lose that advantage.”

He gave the example of work done in late 2024 and into 2025 to negotiate an import protocol for Australian wheat into Indonesia which was triggered by Indonesia’s adoption of “quite an onerous certification system”.

That involved quantifying that Australian grain was free from certain materials.

“Any time you’ve got to do that, it comes with a cost.

“We worked with the government, and with our industry partners, to bring their delegation out here…, show them through the control points we had in our value chain, go back and, over the next two or three months, negotiate a protocol unique to Australia.

“Now the North Americans are trying to play catch up and do the same thing.”

Grain Central: Get our free news straight to your inbox – Click here

Good article Liz!