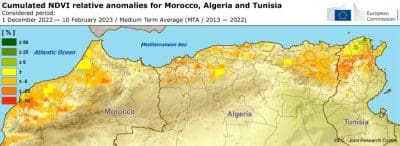

Comparatively poor vegetation conditions signal sub-par crop potential this year in North Africa. Not shown here are the eastern regions, including Libya and Egypt, where prospects presently are better than in the west. Source: European Commission, JRC MARS bulletin global outlook crop monitoring February 2023.

CEREAL production across the Maghreb region of northern Africa is under serious threat this season as extensive drought conditions negatively impact crop yield potential in a band stretching from Mauritania in the west to the western reaches of Libya in the east.

Morocco Algeria losses

Morocco appears to be the worst hit country in terms of lost production potential, with rainfall registrations across much of the country since September last year being the lowest in more than 30 years. Aggregate precipitation in the three months to November 30 was 50 to 80pc below the long-term average.

The drought conditions caused delays to crop seeding in the autumn of up to 30 days, and some fields were simply too dry to plant. Early December rainfall was above average in most cropping areas, but recordings in 2023 to date have been below average. Southwestern Morocco is still in a multi-year drought, and lack of irrigation water meant much of the region’s winter crops were not planted. Biomass accumulation across the growing season in almost all areas is reported to be well below average, leading to a poor prognosis for crop yields.

According to the latest JRC MARS crop bulletin, Morocco’s planted wheat area this season is 2.38Mha, 11pc lower than the five-year average of 2.68Mha. The current yield forecast of 1.49 metric tonne per hectare is 23pc below the five-year average of 1.94t/ha. This culminates in a production forecast of 3.56Mt, 34pc lower than the five-year average of 5.36Mt.

The country’s barley crop is faring no better, with the planted area and current yield forecast 17pc and 30pc below the five-year average, respectively. This puts expected production at 1.04Mt against the five-year average of 1.86Mt. With the winter crop in many regions now in an advanced vegetative stage, substantial rainfall is required in the first half of March to significantly reverse the sliding yield outlook.

The situation in eastern neighbour Algeria is quite similar, where ongoing drought conditions severely hampered the autumn planting program, and vegetative crop growth has been well below average since crop emergence. The pre-seeding period from September to November saw extremely dry conditions, especially in the north-western cropping regions.

And since the beginning of December, the drought area has expanded to the central and eastern cropping regions. Rainfall registrations in many districts from December 1 to February 20 are now the lowest in more than 44 years. Cumulative temperatures in most agricultural areas were 10 to 15pc above the long-term average, and the average daily temperatures were as much as 2°C above the long-term average.

JRC MARS is calling Algeria’s planted area 1.39Mha, a 23pc deficit against the five-year average of 1.81Mha. The current yield forecast is 24pc lower than the five-year average at 1.3t/ha, which leads to a production outlook of 1.8Mt, 45pc lower than the five-year average of 3.25Mt. The barley crop is performing a little better against the five-year average, down 9 and 10pc, respectively. As a result, forecast production currently stands at 1.19Mt compared to the five-year average of 1.47Mt.

Tunisia wants soaking rain

Continuing eastbound journey to Tunisia, where substantial rainfall is urgently required to avoid widespread crop failure this season. Warm and dry conditions have dogged plant growth since planting in late autumn. Very little rain fell from early December to mid-January, and while falls since then have been far more frequent, the substance of most events was quite underwhelming.

Cumulative rainfall since December 1 is running at 10 to 40 millimetres, depending on the cropping region, against long- term average of 50 to 150 millimetres. In some areas, the seven-week period to December 20 ranks as the driest in more than 44 years. The mean daily temperature has exceeded the long-term average by at least 2°C over the same period but as much as 4°C in some districts.

Consequently, soil moisture deficits have been growing far quicker than the wheat and barley plants, save for the irrigated areas. Wheat production is forecast at 0.99Mt, 14pc lower than the five-year average but off an average planted area. Barley output is expected to be down 29pc against the five-year average at 0.37Mt.

Wheat import scale up

Lower cereal production across North Africa will undoubtedly increase demand for European exports, which are already running at a hotter pace than in the 2021/22 marketing year. The European Union has exported more than 19Mt of wheat to the region since July 1 last year, 6.7pc ahead of the previous season’s shipments. The early pace was slow, with Russian supplies displacing traditional EU business, but the sales have picked up, especially into Algeria, in recent months. On the other hand, current season barley shipments to the region to early February were sitting at 3.2Mt, lagging those of the 2021/22 season by around 40pc.

While the European crop is currently ticking along quite nicely, any crop scares will be exacerbated by the lower production outlook on the southern side of the Mediterranean Sea. The EU is also expected to enter the 2023/24 marketing year with a weakened net export supply position relative to its main competitor, namely Russia.

The USDA is pegging EU carry-in wheat stocks for 2023/24 at just 11.1Mt, against Russia with 14.4Mt. But the USDA still has 2022/23 Russian production at 92Mt against the local analysts at more than 100Mt. Agritel appears to have a slightly more realistic balance with this season’s carry-outs at 14.1Mt and 21.9Mt for the EU and Russia, respectively. Either way, the EU will enter the 2023/24 marketing year in a suboptimal position to fill the increased Maghreb wheat demand in 2023/24.

HAVE YOUR SAY