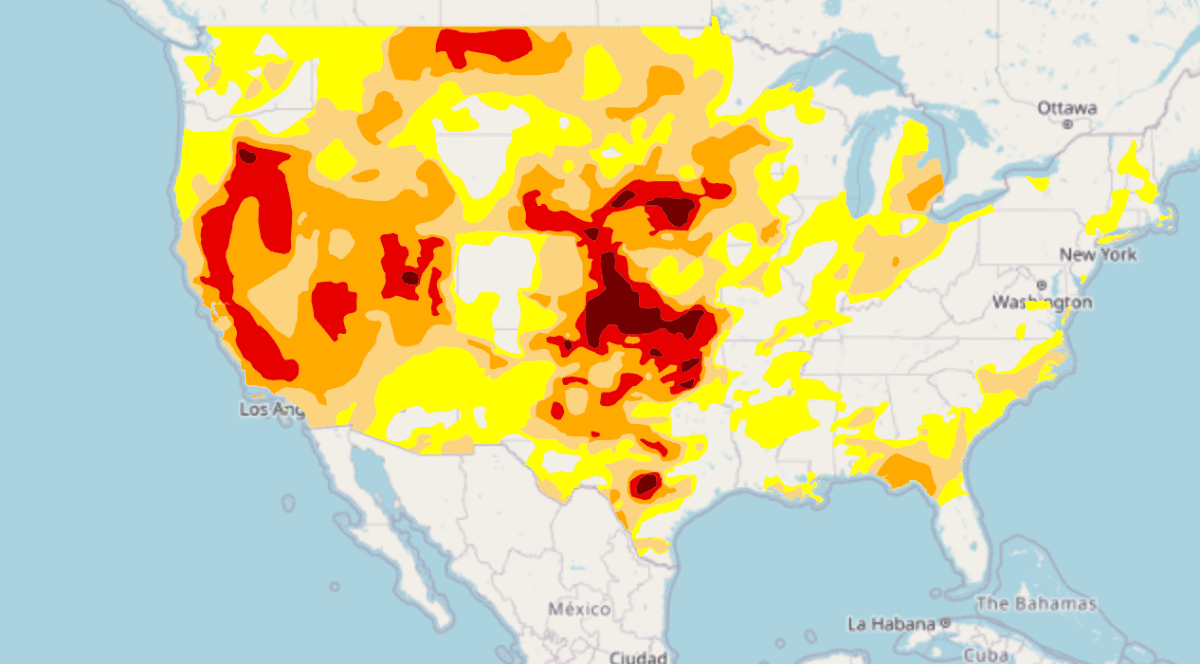

A drought map of the US for the week to January 3, with shades ranging from yellow as abnormally dry to maroon as exceptional drought. Source: US Drought Monitor

VAST swathes of the United States remain extremely parched, despite beneficial rainfall in some regions as the calendar rolled into the New Year. As of 3 January 2023, 38.7pc of the total US land area and 46.3pc of the lower 48 states (excludes Hawaii and Alaska) were experiencing moderate to exceptional drought conditions.

While a bout of stormy weather in the last week of 2022 and the first week of 2023 saw rainfall registrations leave their mark on California’s record books, the US Great Plains remains in a world of pain, with the 2023-24 winter-crop production in serious jeopardy.

Hard wheat bears brunt

According to the National Integrated Drought Information System, 123.3Mha of crops in the US were experiencing drought conditions on January 3, unchanged week on week but 14.7pc lower than a month earlier. The United States Department of Agriculture estimates 64pc of the nation’s winter wheat area is drought declared, down slightly from 69pc a week earlier. Most of the improvements were on the fringes of the western and southern Soft Red Winter wheat-growing regions.

Analysis of the US drought monitor data suggests that the Hard Red Winter wheat production areas of the US Plains are in far worse shape than the soft wheat areas, with slight improvement apparent in the last week and very little joy in the short-term weather forecast. The vast majority of Hard Red production areas were in some stage of drought declaration, most in the severe to extreme categories.

In the last USDA crop progress report for 2022, the national winter wheat crop rating was 34pc good to excellent as of November 27. That was the second-worst rating for that time of year since 1987. Add a devastating freeze in parts of Kansas and Texas in the week before Christmas and well below-average rainfall in December for most of the wheat growing areas, and the picture has definitely deteriorated.

Spotlight on Kansas

The most severe moisture deficits are apparent in Kansas, the top HRW wheat-production state. The northeast portion of the state is rated abnormally dry or moderate drought. But three-quarters of the state, including the major wheat-growing areas, are enduring extreme or exceptional drought conditions, predominantly the latter.

Last week, the USDA rated topsoil moisture levels across Kansas as 43pc very short, 26pc short, 29pc adequate and just 2pc in surplus. Subsoil moisture reserves were rated 47pc very short, 34pc short, 18pc adequate and only 1pc in surplus. The state’s declining winter wheat crop ratings reflected the poor soil-moisture status, with 2pc of the crop deemed excellent, 17pc good, 32pc fair, 26pc poor and 23pc very poor compared to 2pc excellent, 20pc good, 36pc fair, 24pc poor and 18pc very poor five weeks earlier.

The acute drought areas also spread south into Oklahoma, where most agricultural land area is experiencing extreme or severe drought. Nonetheless, winter wheat ratings have improved slightly since late November, with 38pc of the crop in the good to excellent categories last week against 31pc, and 24pc in the poor to very poor categories last week compared to 27pc. Eastern Texas is currently in good shape, but the western half, including the panhandle, is suffering moderate to severe drought, with isolated areas of extreme drought.

Nebraska to the north is entirely drought declared, much of it in the severe and extreme stages. The local USDA office pegged winter wheat conditions at 18pc good to excellent and 36pc poor to very poor, compared to 20pc and 39pc on November 27. The wheat growing areas of South Dakota and Montana are generally in much better shape moisture wise, but the crop is still suffering. In South Dakota, only 16pc of the crop is rated good (zero excellent), a significant decline from 27pc in late November. Montana’s winter wheat crop was rated 44pc good to excellent on November 27, but that had halved to 22pc last week.

Snow missing in south

Snow cover is essential for protection of the US winter crop over the cold and windy winter months, acting as a warming blanket and insulating the hibernating plant. The current cover is moderate to heavy in much of the northwest and northern US. However, almost all winter wheat areas of the Southern Plains and the southern Midwest have little to no protection, with strong winds sweeping away what settled during the minor flurries of recent weeks. Winterkill becomes a distinct possibility if the plant remains exposed to the harsh winter element.

Meanwhile, on January 12, the USDA will release its first estimate of the area planted to winter wheat for the 2023/24 season. The upward area trend over the past three years is expected to continue with the pre-report forecasts of a total winter wheat area of between 13.8 and 14.6Mha, both higher than the final 2022/23 planted area of 33.3Mha. Early trade forecasts suggest that the HRW wheat area will be up around 7pc year-on-year, and the Soft Red Winter wheat area will likely come in around 11pc higher.

Shrug from US markets

Such a poor US wheat production outlook would typically give the “bulls” something to celebrate, but the futures market reaction has been relatively ho-hum, with the March Chicago contract losing more than 6pc of its value in 2023. Improved global weather patterns and big crops in Russia and Australia appear to be allaying international supply concerns.

Most meteorologists are now forecasting a breakdown of the La Niña phenomenon that has dominated global weather for the past three years. Expectations are for neutral conditions or even a weak El Niño, which would boost crop production prospects around the globe, most immediately row crops in Argentina and winter crops in Northern Hemisphere producers such as Europe and the US.

We all know that last season’s wheat crop in Russia was huge, indeed a record, and according to local analysts, north of 100Mt. And it seems an Australian wheat crop as high as 42Mt may finally be gaining recognition in global markets with plenty of chatter in wires and on social media over the past week. Export capacity becomes the limiting factor in both jurisdictions, but it does add supply certainty out the curve with higher carry-outs.

But solid export margins do encourage investment in logistics and elevation capacity. Considering Australia exported 28Mt in the 12 months to October 31, despite some extremely testing logistic challenges, it is within the realms of possibility that exports could challenge 30Mt in the corresponding period in 2022-23.

HAVE YOUR SAY