Each year the Federal Government’s official commodity forecaster releases production and price forecasts for Australia’s key agricultural conferences.

Here’s a snapshot of what ABARES sees ahead for wheat, barley, sorghum, canola and cotton.

(If you’ve got a bit more time you can read the full comprehensive report on ABARES’s website here)

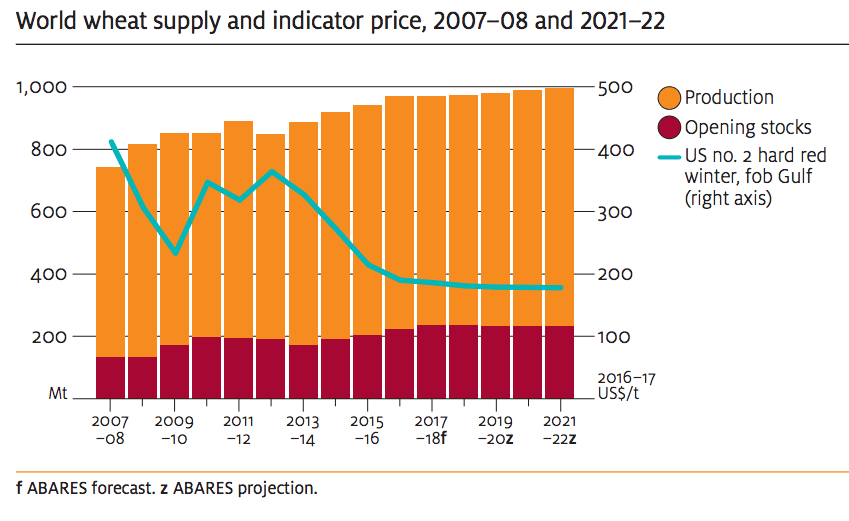

Wheat

- World wheat prices are projected to remain low in the short to medium term

- Abundant world supplies and competition from other feed grains on the global market keeping prices lower.

- World production of wheat is forecast to decline in 2017–18 but increase in the medium term as average yields return to historical trends.

- World wheat consumption is projected to grow from 735 million tonnes in 2016-17 to 762 million tonnes in 2021-22 – Driven largely by increases in Asia

- By 2021-22, China is projected to hold 45pc of world wheat stocks

- Australian wheat production to fall from 35 million tonnes in 2016-17 to 24 million tonnes in 2017-18

- In medium term, production expected to remain around 25 million tonnes in 2021-22

- Wheat export shipments in 2017-18 to fall by 8pc to 21 million tonnes (down from 23 million tonnes in 2016-17)

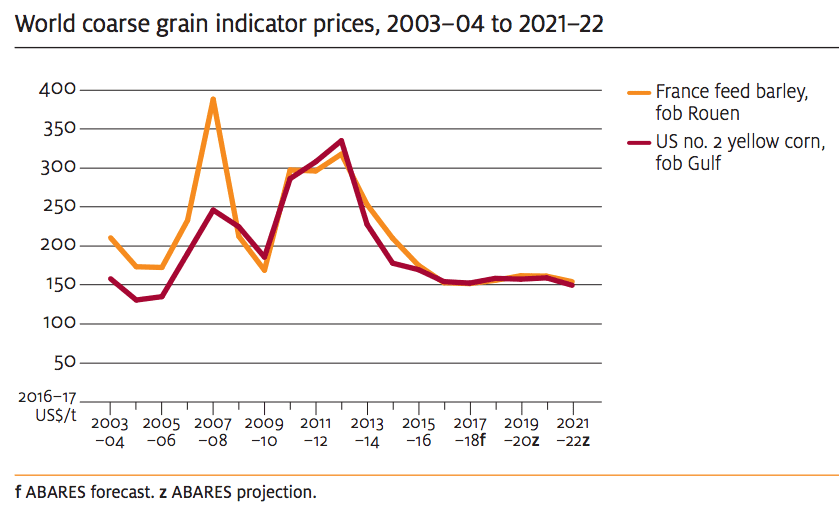

Coarse Grains

- World coarse grain indicator prices are forecast to remain historically low in 2017–18 and over the medium term, reflecting abundant world grain stocks.

- The 2017–18 world coarse grain indicator price (US no. 2 yellow corn, fob Gulf) is forecast to be US$157 a tonne, largely unchanged from the average price in 2016–17.

- The world indicator price for barley (France feed barley, fob Rouen) is forecast to average 1 per cent higher in 2017–18 at US$155 a tonne

- Consecutive years of increasing production have resulted in record world stock levels.

- Australian coarse grain production and exports are forecast to fall in 2017–18 but to increase over the medium term.

- Australian barley production in 2017-18 to fall 37pc to around 8.5 million tonnes, reflecting return to average yields

- Area planted to grain sorghum in Australia to increase from 441,000 hectares un 2016-17 to 631,000ha in 2017-18, boosted by Qld ethanol mandate introduced in Jan 2017

- World demand for coarse grains for livestock feed in developing countries expected to be main source of growth in next five years

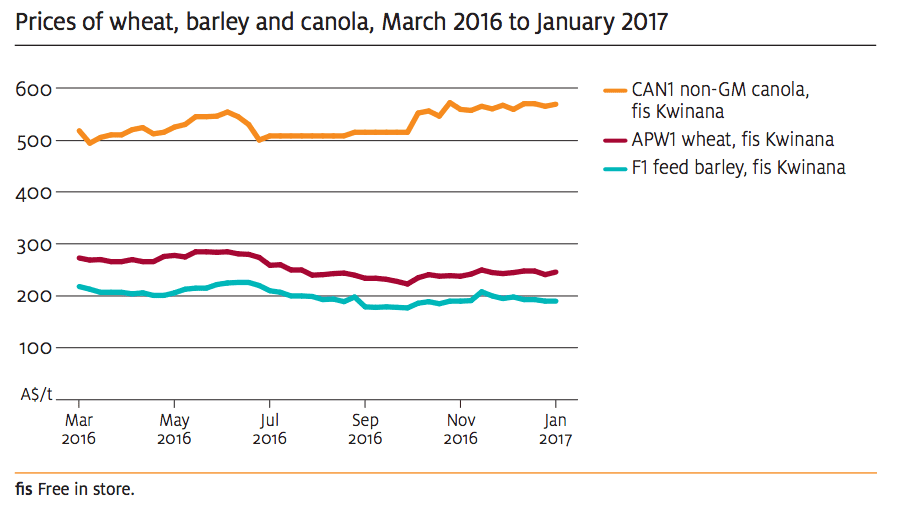

Oilseeds

In contrast with wheat and barley, Australian canola prices have risen compared with March 2016

- World oilseed indicator price is forecast to average lower in 2017–18, reflecting abundant stocks at the beginning of the year and another year of good harvests in major exporting countries.

- Prices to 2021–22 are projected to fall because of a continuation of strong yield gains and area expansion in South America.

- Australian canola plantings are forecast to rise in 2017–18, reflecting better returns to producers compared with other cropping alternatives.

- In contrast with wheat and barley, Australian canola prices have risen compared with March 2016

- Area planted will hinge on timing of rainfall in Autumn

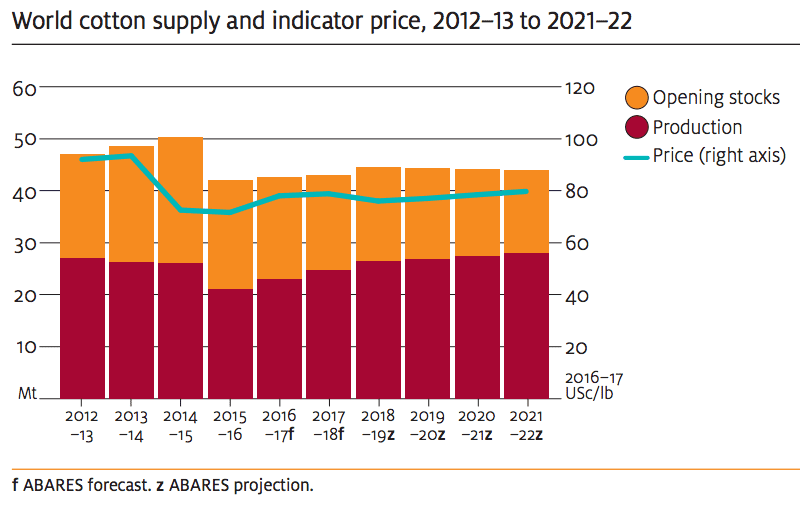

Cotton

- World cotton prices are forecast to increase over the short term as a result of world cotton consumption exceeding production.

- In 2021–22 world cotton prices are projected to average around US80 cents a pound (in 2016–17 dollars), reflecting continued growth in world consumption driven by strong demand from non-OECD apparel-producing countries.

- Returns to Australian cotton growers are projected to rise to average $592 a bale (in 2016–17 dollars) in 2021–22, reflecting higher world prices

- Cotton exports from Australia are projected to increase to around 1 million tonnes in 2021–22 from a forecast 774,000 tonnes in 2016–17.

Source: ABARES. To read full report click here

HAVE YOUR SAY