JUST over a decade ago ANZ’s market intelligence team produced a detailed report entitled Greener Pastures which forecast how the next 10 years was likely to pan out for Australian agriculture, and for investment in the sector.

Now that the period covered by the forecast has passed, how accurate did the outlook prove to be?

ANZ has released a new report called Greener Pastures 2 which objectively answers that question, highlighting where the original report was on the money, where forecasts were wider of the mark, and lessons learned from the process, along with a fresh forecast on what is likely to happen in the next 10 years.

ANZ has released a new report called Greener Pastures 2 which objectively answers that question, highlighting where the original report was on the money, where forecasts were wider of the mark, and lessons learned from the process, along with a fresh forecast on what is likely to happen in the next 10 years.

The full report is recommended reading, providing an in-depth overview of key factors that have contributed to the rise and rise of Australian agriculture over the past 10 years, and thoughtful analysis of the factors likely to influence the direction from here.

This article covers key points and insights from the report, but the full 56 page report can be downloaded and read here.

Ultimately the report tells the story of a decade that proved to be far more positive for Australian agriculture than many had predicted 10 years ago, a period of prosperity that has placed the sector in a substantially more globally competitive position, and well poised to capture opportunities to continue to prosper.

“For the most part, opposition to new investment 10 years ago has been replaced by enthusiasm,” the ANZ observes.

Behind the rise has been extended high prices for most agricultural commodities, combined with a string of good production seasons, and the benefits from constant improvements in structural efficiency, resilience, innovation and technology.

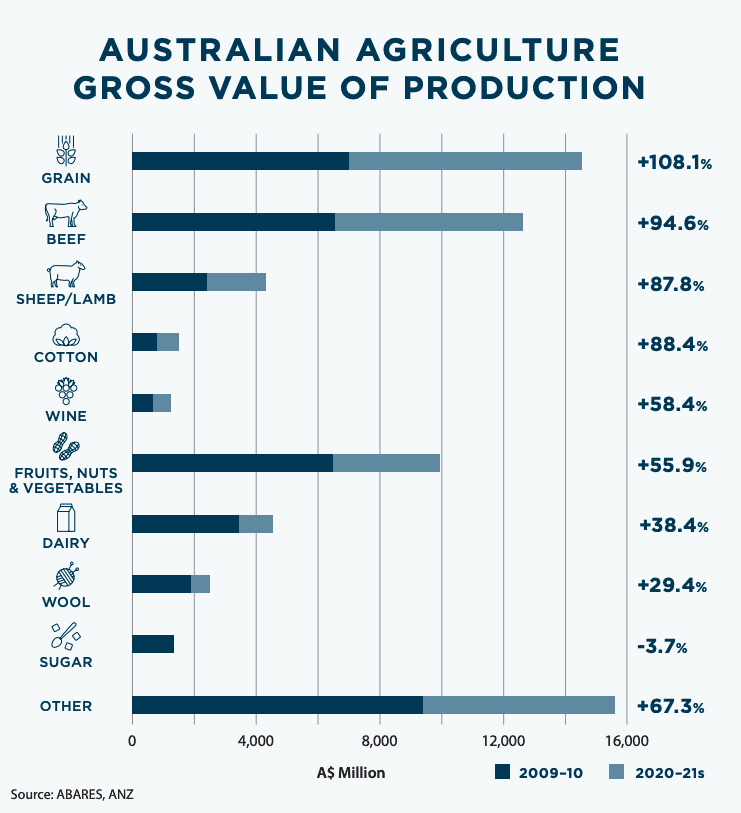

– Aus ag’s gross value of production grew faster than expected

Click on images to enlarge. Images source: ANZ

In 2010-11, Australian agriculture’s gross value of production was $49 billion.

GP1 forecast the sector to grow by a base rate of 2pc per year over 10 years to $58 billion by 2019/20.

The actual average growth rate achieved was 3.2pc, bringing GVP to $61 biliion in 2019/20.

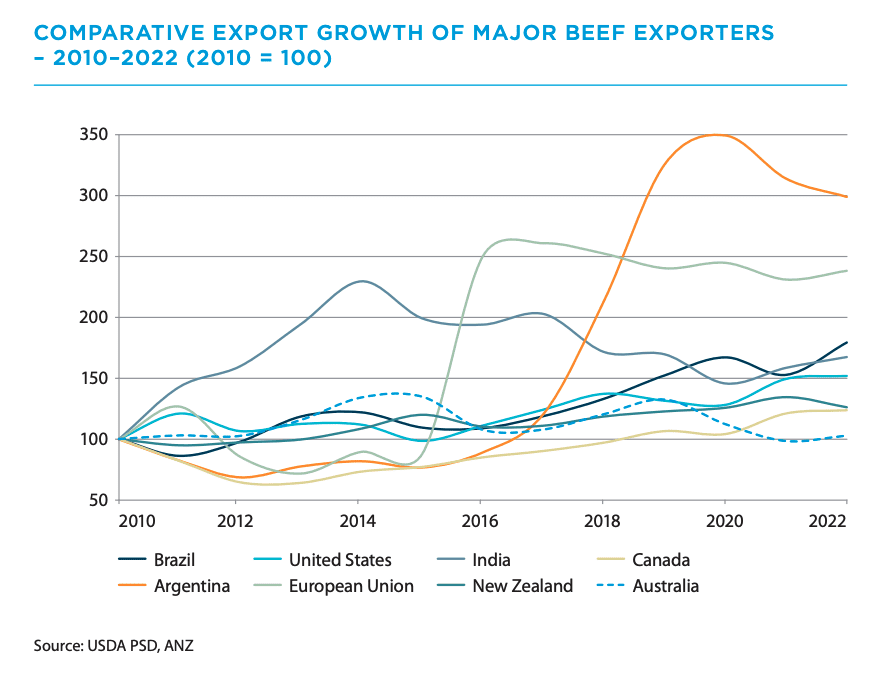

A clear trend across the last decade was the surge in demand for meat, as Australian agriculture’s GVP for meat overtook that of grain. Driven by rising exports and higher than forecast prices, beef production doubled in value to $14.6 billion in the 10 years to 2019/20.

– Aus ag exports surged beyond expectations

While forecasts at the time the GP1 report pointed to a looming surge in agricultural exports. this was supported by the continuing growth of the middle classes, particularly in Asia, as well as an accompanying change in diets towards increased consumption of meat and dairy, which helped to drive more investment in the sector.

The GP1 report forecast Australian ag exports to rise in a range between a base rate of $33 billion and high of $80 billion over the 10 years. The actual figure was an additional $111.5 billion.

This was principally driven by China’s rapid upsurge in importing Australian beef in the middle of the decade.

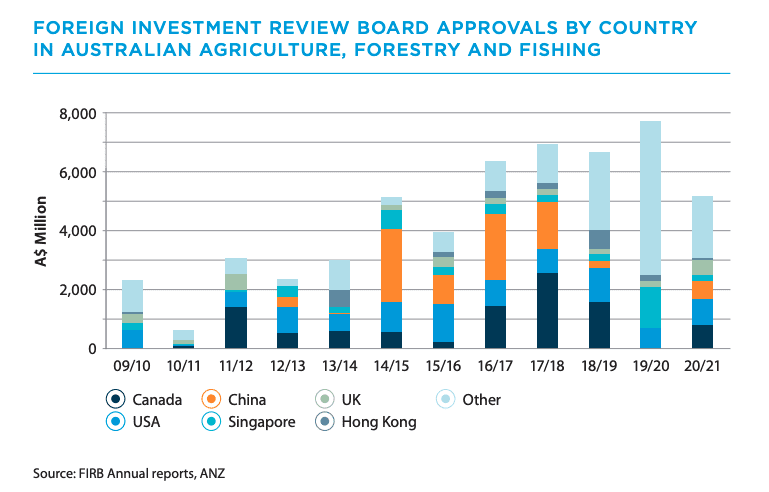

– Aus ag’s capital requirements eventuated

Australian agriculture has proven to be a compelling investment case for both existing participants and external investors, the report notes.

GP1 forecast in the decade of the 2010s that Australia would require $83 billion to continue to grow production, as well as $68 billion for farm turnover.

GP1 forecast in the decade of the 2010s that Australia would require $83 billion to continue to grow production, as well as $68 billion for farm turnover.

As it eventuated, Australian agriculture ultimately saw an investment of $212 billion in agricultural production over the decade, well above the original forecast.

This figure reflected the eventual major inflow of both domestic and global investment into the sector.

“Despite concerns at the start of the 2010s that attracting investment to Australian agriculture may be challenging, clearly this shows that the momentum of global food demand over the decade, combined with the positive attributes of Australian agriculture, meant that it was ultimately quite achievable.”

A key trend over the last decade has been the evolution of the capacity of Australian farmers to reinvest in their own sector, in contrast to expectations at the start of the decade that family farmers would inevitably decline in the wider production landscape, with the space likely to be filled by the growth in corporate farming operations.

But many family farms emerged stronger than ever and now find themselves in a robust position both financially and agronomically, developing more innovative and efficiency multi-generational farming operations and enabling them to make long term strategic decisions with far more complexity than 10 years ago.

– Efficiency gains helped to mitigate labour concerns

It was estimated at the start of the decade that Australia faced a shortage of 100,000 workers, and constraints on worker availability would prevent agriculture from keeping pace with the sector’s expected strong growth.

However, developments over the past decade had somewhat mitigated this concern. The consolidation of farms, growth in corporate farming structures, and the growth in efficiency measurements has seen an ongoing reduction in the labour requirements of the major agricultural sectors. ANZ modelling has shown that for both the broadacre and dairy sectors, total labour time for each sector overall has fallen over the past 30 years. This is largely due to rapid advances in agricultural technology.

– Deregulation and restructuring gave rise to innovation

The post-regulation of major Australian agricultural commodity sectors (cropping, wool, dairy, eggs) has continued to drive the push for greater efficiency.

The post-regulation of major Australian agricultural commodity sectors (cropping, wool, dairy, eggs) has continued to drive the push for greater efficiency.

The ANZ notes that while global discussion around whether some of Australia’s major competitors should look to reduce agricultural subsidies, the political situation remains that for domestic political reasons in many countries, little is likely to change. “This is a reality with which Australian agriculture must come to terms”.

It adds that the freedom to choose marketing outlets for their commodities as well as pursue individual trade relationships has enabled modern producers to explore innovative developments tailored to their buyers’ needs.

– Greater control of production costs boosted Australia’s international competitiveness

The first report in 2010 showed that as costs rose across supply chains, Australian agriculture lost international competitiveness. At the time, the average production cost of Australian beef and wheat was already double that of export competitor Argentina.

By 2020 however, Australia’s cost of production for most major agricultural products sat comfortably among the best in the developed world. While a factor in the previous decade had often been labour costs, the growth in technology for many agricultural production and processing areas had reduced this as a variable today. For beef cattle, Australia’s cost structures by 2020 were similar to those of North and South America. However, Australia remains a relatively high-cost producer of wheat.

Looking ahead to 2030

While qualifying that the potential outlook is “highly variable” and subject to impacts by unexpected global factors, ANZ suggests Australian agricultural exports are set to rise at a base rate of 3pc per annum to gain an extra $82 billion over the next decade.

A “high-side” scenario would see export growth rates of 5pc per year to an overall $153 billion rise. This would require commodity prices to maintain high levels, which, with tightening global food supplies, the ANZ report notes, seems a reasonable assumption.

It would also require Australia to maintain its share of big export markets while also growing its share of other markets. This would rely on Australia’s ability to continuing innovating in commodities to suit market demands, such as producing animal proteins with lower carbon footprints.

It would also require Australia to maintain its share of big export markets while also growing its share of other markets. This would rely on Australia’s ability to continuing innovating in commodities to suit market demands, such as producing animal proteins with lower carbon footprints.

ANZ forecasts structural change ahead in Australian farm ownership, as the outlook as shifted substantially from where it may have been 5 to 10 years ago, and farms now more attractive to family members (and their partners) coming back from capital cities.

An increasing number of variables will impact investment flows into agriculture over the next decade, ANZ suggests, including global agricultural trade, ongoing consolidation of Australian farms, the increasing impact of agtech implementation, sustainability regulations and climate.

Its base case forecast is that over the current decade (2021-2030) Australia will require a further $122 billion in investment to grow agricultural productivity, as well as an additional $118 billion to fund the turnover of farms.

“Given the strong investment growth over the previous decade, this would seem an achievable goal,” the report states. “The challenge will increase if Australia looks to accelerate its rate of productivity.”

Aus ag’s $100b by 2030 target may be a stretch

The report also highlights how challenging it may be for Australian agriculture to attain its stated goal of achieving Gross Value of Production of $100 billion by 2030.

The ANZ’s “base case” forecast sees Australian agriculture’s GVP climbing from $61 billion to $83 billion in 2030, based on a forecast annual increase of 3 percent.

To reach the $100b by 2030 goal, annual production value growth would have to increase at just over 5pc this decade.

That would require an additional $284 billion in investment for growth, and $133 billion for farm turnover – an increase of 73pc on the base case requirements, and almost double the level of investment that Australia saw in the 2010s.

Future of farm ownership

The ANZ’s modelling also looks at the future of farm ownership.

It presents that of current rural enterprises, 40 percent are likely to still be held by the same ownership in 2030, and another 15pc will be in the same family, but will have been passed onto the next generation.

30pc will have been purchased by either a neighbour, or a local farmer or farming family, with 15pc purchased and operated by outside investors or farm management companies.

The stronger family farm segment also provides a new investment pathway into agriculture for outside investors, the report notes. While still being considered an emerging option, it offers investors who may have the scale to purchase a major agricultural asset and run a skilled management team an option of partnering with an innovative family operation to jointly build the business.

Changing nature of agricultural investors

A major change between the 2010s and 2020s documented in the report is the structure of large investments in Australian agriculture. Over the past 10 years offshore funds including pension funds, endowment funds and family offices have gradually become the dominant vehicle for the purchase and management of major agricultural assets.

The ANZ predicts this trend to continue, with the emergence of even larger domestic funds from industry consolidation with greater strength to invest in larger agricultural production assets, along with high net worth Australians, as the scale of wealth at the high end of the spectrum continues to grow dramatically.

Five paths to enhancing agricultural growth

The report concludes by proposing five major, and interlinked ways stakeholders across the Australian agricultural landscape can work together – by understanding the impact of capital flows, green technology, sustainability practices, enhanced trade flows, and greater industry cohesion.

– Improve the process of capital flows into agriculture

As more Australian super funds grow in scale far larger than their current size, they will have the ability to not only pursue investments in agriculture more aggressively, but also to acquire far larger assets. It is important for the industry to best position itself to take advantage of a likely pending growth in domestic appetite.

Farmers will also need to be “investment ready”, which will require education on the metrics usually required by investors, as well as any new sustainability characteristics an operation should adopt to become an attractive investment proposition.

– Embrace agricultural technology

In the coming decade, likely increases in regulatory requirements around sustainability will create further impetus for widespread uptake of agtech. A greater compulsion to show a range of sustainability metrics – such as reducing water usage or carbon capture – will push many agricultural producers to utilise relevant agtech mechanisms to boost their ability to achieve and record future sustainability metrics.

– Utilise sustainability for economic advancement

It is increasingly likely that major international investors, both Australian and global, as well as Australian agriculture’s global customer base, will require far more extensive sustainability and carbon metrics.

A question which will increasingly arise will be around what is more valuable to a farmer – the carbon credit cashflow (from trading credits from carbon captured on farm for financial return to an entity which may emit carbon emissions), or the license to operate (keeping credits generated by their own operations to offset their own individual emissions profile).

A further question will be whether the industry will be able to reach a position of being a net positive carbon sink, which would allow it both to sell credits, while remaining carbon neutral.

– Improve the trade landscape

Australia needs to concentrate on several main area to solidify its global export strength, including streamlining trade flows, enhancing trading relationships, seeking new markets. and develop and refine niche product offerings.

– Advocacy and industry cohesion

Like all major industries in Australia, the agriculture sector looks to its peak bodies for a range of advocacy functions.

The role of peak agricultural bodies will continue to be encapsulating and promoting issues which are important for the broader agricultural sector, including the enhancement of regional telecommunications or promoting upskilling on agricultural sustainability programs. They should play a lead role in promoting positive messages by the industry out to the wider community. Most importantly, they need to play a strong and expert role in all aspects of policy and regulatory development, in any way which may impact agriculture.

As the farmer base continues to decline, and sustainability initiatives will come to the fore, Australian peak bodies will need to explore the option of including more commercial partners while at the same time, not compromising the interests of primary producers. Consolidation among groups will be unavoidable and never easy in an industry of very big personalities.

To download the full ANZ Greener Pastures 2 report click here

HAVE YOUR SAY