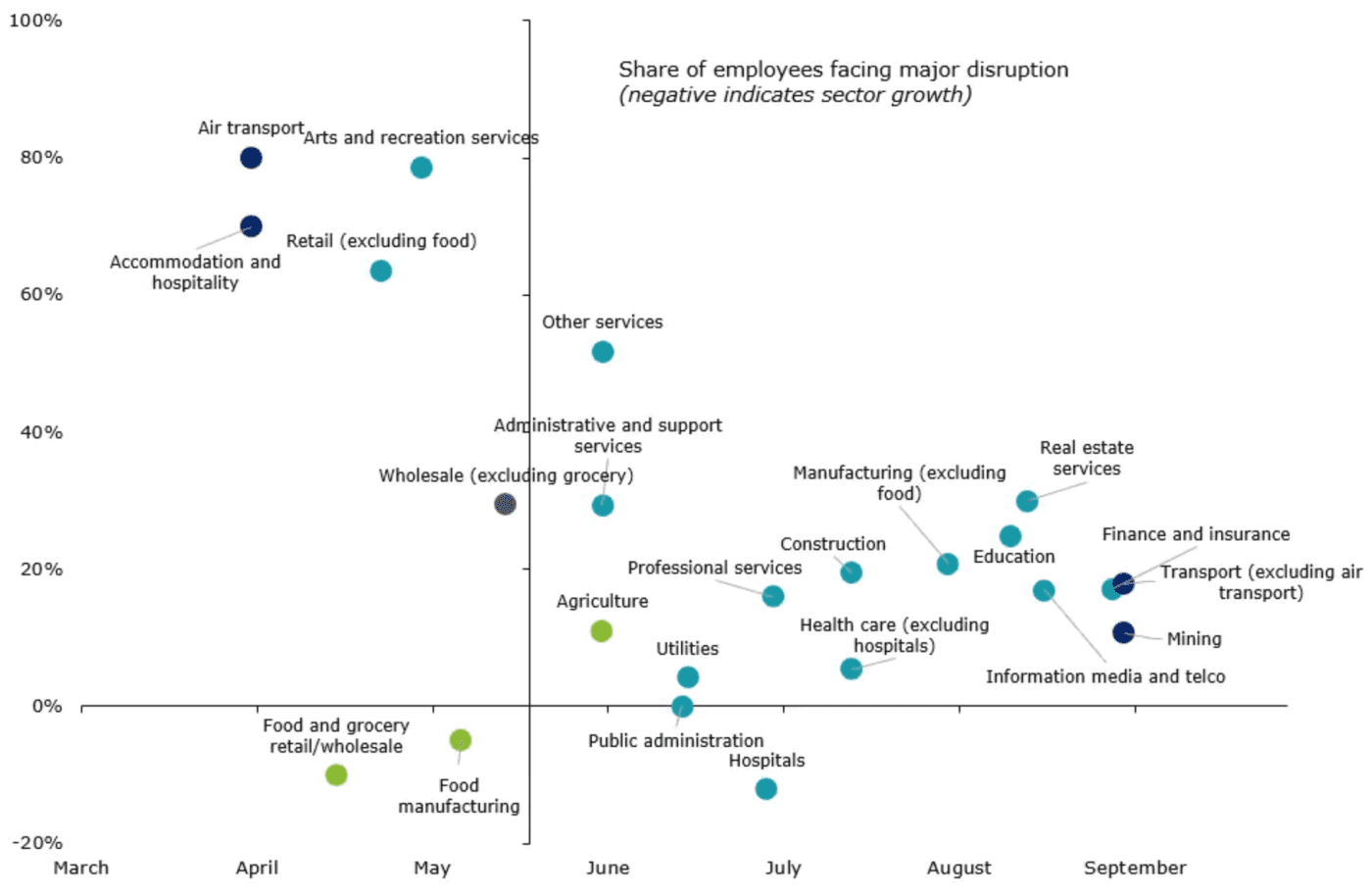

Covid-19 Australian industry stress map, charting jobs at risk (vertical axis), relative to period of expected peak impact. Source: Deloitte (3 April). Source: Deloitte. Click image to enlarge

AUSTRALIAN agribusiness has been a quiet achiever in a troubled economy during the COVID-19 crisis, analysis by financial consultancy Deloitte Access Economics shows.

The firm has released a chart (above) to illustrate how the effects of the COVID-19 event and the timing of those effects have varied enormously from industry to industry in Australia.

The vertical axis charts jobs at risk, while the horizontal axis charts the period of expected ‘peak’ impact, according to Deloitte’s analysis.

Industries positioned in the top left quadrant were impacted “early and deeply” by the virus and the global response to it.

These included air transport, accommodation and recreation services, where swift curtailing of people movements dramatically reduced industry activity.

As economic risks have escalated, the impacts of COVID-19 have spread to most other industries, including much of the services sector, manufacturing, construction and mining. These impacts are expected to be realised relatively later, but still generate significant challenges, Deloitte notes.

A few industries are expected to fare better than the rest of the economy.

This includes those industries forming food supply chains – especially agriculture, food manufacturing and food retailing (highlighted in green) – which stand out as being sectors suffering the least.

Food manufacturing and food and grocery retail actually show a slight expansion.

Deloitte stressed this did not mean the consequences of the virus were minimal, rather that there have been some positives amongst the negatives for Australian agribusiness.

‘People still need to eat’

It notes that there is reason for continued optimism in the agribusiness sector because “people still need to eat”.

“Because food is an essential product demand remains high,” the report said.

“Unlike other sectors, agribusiness supply chains have not been heavily restricted by government regulation.

“Indeed, the Commonwealth Government has confirmed what we knew, all farming and forestry are essential services, as well as food, beverage and fibre production and saleyards and auction.”

Dollar depreciation boost

Optimism for the sector has also been buoyed by a stark depreciation of the exchange rate as a result of COVID-19.

Compared to the start of the year, the Australian dollar is around 10 cents lower than (down 11pc) the US dollar.

“This competitive boost for our exports is comparable to that during the global financial crisis, where a weaker Australian dollar (which fell from around US98c in mid-2008 to US72c a year later) largely shielded Agribusiness from reduced global demand.”

Agribusiness had also benefited from reduced competition for its scarce inputs. This includes oil where prices fell more than 50 percent between early February and mid-March, as demand from non-essential services disappeared (combined with a spike in production).

Favourable seasonal outlook adds to optimism

And while not an effect of COVID-19, the current favourable outlook for the growing season is likely to significantly contribute to the sector’s optimism, the report states.

“Even a return to average conditions could see a dramatic increase in agricultural production, with last year’s grain harvest around 33 per cent below the 10-year average.

“This growth in output should support farm profitability and provide enterprises with options that may otherwise have been unavailable as they look to navigate this period of considerable uncertainty.”

Catalyst for strong future supply chains

The report said COVID-19 has clearly exposed some of the supply chain weaknesses in a globalised world, which could lead to changes in Australian agribusiness supply chains in future.

Australian farmers may seek greater certainty of supply for inputs such as fertiliser, which this could provide a catalyst for the development of a competitive Australian fertiliser production sector.

The absence of cheap and readily available labour could also prompt an increased development of mechanisation, in industries such as horticulture.

The experience also provided the agribusiness supply chain with an opportunity to modernise and address some of its structural issues.

“This includes issues such as traceability and competitiveness in freight and logistics with this market disruption highlighting the need for greater transparency, resilience and flexibility.

“Modernising our supply chains would not only deliver significant productivity boost at home, but it would also provide greater competitiveness in export markets.”

Longer term, the structural impacts of COVID-19 on agribusiness will persist.

“A poorer Australia and a poorer world will see higher demand for staple foods, at the expense of the exotic. The resilience of food supply chains is being questioned, and the interdependence of our food production systems dramatically highlighted, potentially affecting preferences for locally sourced produce.

“The way that food moves from paddock to plate, and the way we think about it may never return to pre COVID-19 ways. While the balance remains to be seen, this is likely to include at least some good news for the Australian agribusiness sector.”

To read the full report, authored by Deloitte Access Economics’ Dr Daniel Terrill and Deloitte Access Economics manager Dr Stacey Paterson, click here to visit the Deloitte website

Grain Central: Get our free daily cropping news straight to your inbox – Click here

HAVE YOUR SAY