AUSTRALIA is looking at a second consecutive near-record winter crop planting, as excellent prices and good seasonal conditions see planted hectares rise, according to Rabobank’s just-released 2021/22 Winter Crop Outlook.

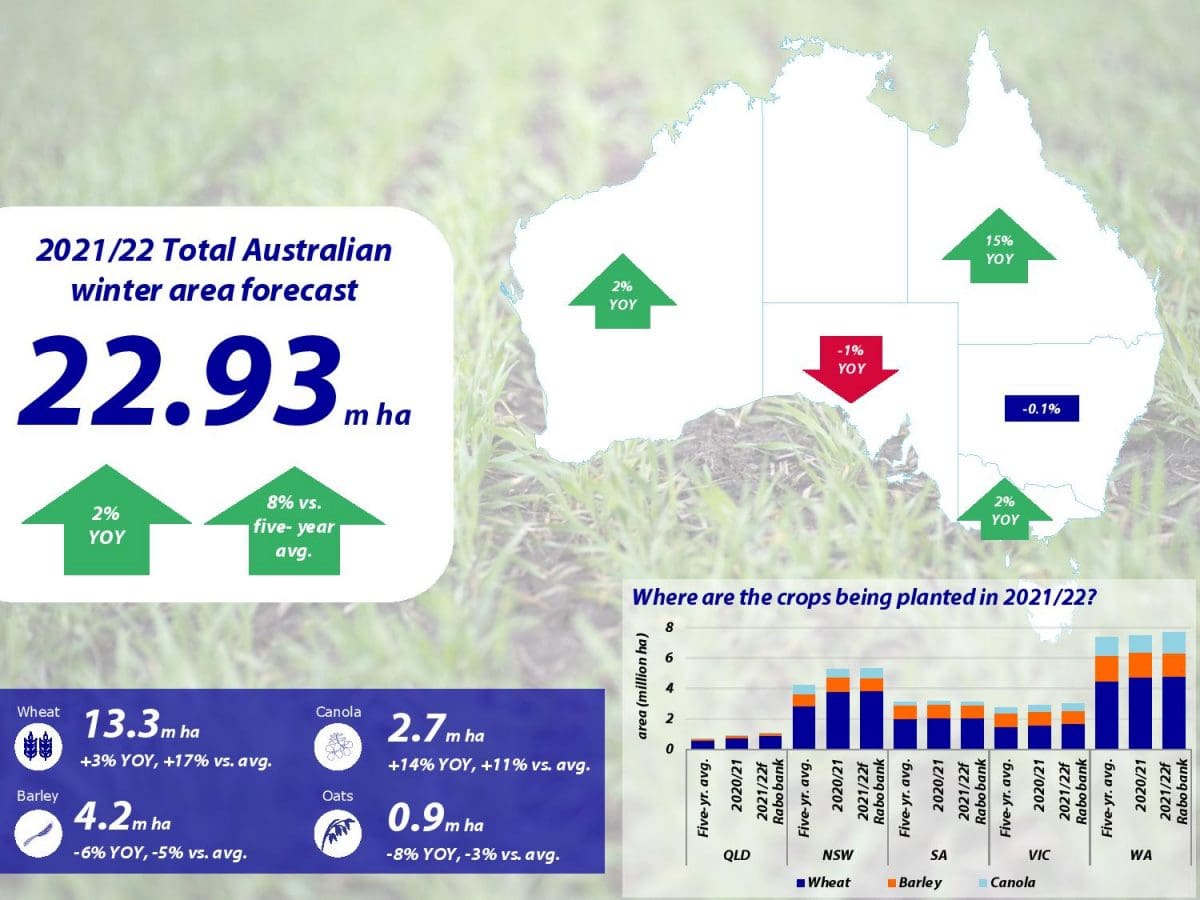

The bank says the national winter crop planting – currently underway across the country – is forecast at 22.93 million hectares (Mha).

This is up two per cent on last year – where planted area had soared on the back of a return to positive seasonal conditions around the country – and within 1pc of the nation’s record-high winter crop planting in 2016/17.

This acreage also represents an area 8pc above the five-year average.

The bank says this will see Australia on track to deliver an above-average winter grain crop for this season, with an estimated total wheat harvest of 28.9 million tonnes (Mt), barley 10Mt and canola 4.1Mt.

Positive outlook

Report co-author, Rabobank grains and oilseeds analyst Dennis Voznesenski said with substantial rainfall and good soil moisture profiles across many parts of the country coming into this year’s planting, Australia was overall set up for another very strong winter grain crop.

“And with the Bureau of Meteorology forecasting a 60 to 75 per cent chance of the east coast and South Australia exceeding median rainfall for the next three months, this should set crops up well and have a positive impact on yields in those regions,” he said.

Some states had, however, fared better than others with seasonal conditions coming into planting, the report noted.

“While most regions had excellent opening rainfall, particularly in Western Australian and northern New South Wales, not all have been so fortunate,” Mr Voznesenski said.

“In parts of South Australia and western Victoria, less favourable conditions have meant we will not be able to factor in a year-on-year increase in area planted in those regions, despite prices incentivising many other regions to expand total area.

“So, the forecast of further rainfall will be particularly welcome in South Australia and western Victoria, where the soil moisture profile was far less optimal than hoped for coming into planting.

“For Western Australia, conditions have been very favourable for the opening to the planting season due to the rainfall associated with Cyclone Seroja. So, while WA is only forecast to receive average to below-average rainfall in the next three months, the impact should be softened by the favourable soil moisture at planting.”

For specific commodities, the bank is forecasting a 3pc increase in wheat planting this year (to 13.3Mha), while area planted to canola is expected to climb by 14pc (to 2.7Mha).

Barley planting is down an estimated 6pc (to 4.2Mha), with oats declining eight per cent (to 0.9Mha).

“With canola prices near record highs, and China’s tariff on Australian barley top of mind, farmers have heeded the call and switched in favour of canola,” Mr Voznesenski said.

“Come harvest time, however, it may mean that there will be increased harvest pressure on local canola prices.”

With tight global markets and the world looking for Australian grain, the report says, the nation will likely be in a position to respond, with above-average export availability expected in 2021/22.

Elevated global prices

Report co-author, Rabobank senior grains and oilseeds analyst Cheryl Kalisch Gordon said at this stage, the bank was “pencilling in an export program of almost 20Mt of wheat, 5.5Mt of barley and 3.1Mt of canola”.

Global prices for most grains and oilseeds are expected to remain elevated over the next 12 months, the bank says, on the back of strong demand and poor seasonal conditions in many other of the world’s grain-growing regions.

Domestically, Dr Kalisch Gordon said, Australian wheat track prices were expected to remain near to A$300 per tonne for the coming 12 months, with marginal strengthening in the first quarter of 2022. Australian feed barley track prices were forecast to trade at around A$250/t over the same period, with some softening in quarter three 2021, and canola prices to remain elevated.

“Strength in the Australian dollar, which we forecast to continue to trade in the high US70 cents range, together with strong local supply, will keep local prices at more modest levels than global price levels would otherwise support,” she said.

State by state

Western Australia, Victoria and Queensland are all forecast to see year-on-year increases in area planted to winter crop, with Queensland up as much as 15pc (to 1.3Mha). WA plantings are estimated to be up 2pc to 8.49Mha and Victoria also up 2pc to 3.5Mha.

For New South Wales, the report says, the state is expected to plant another massive 6Mha of crops this year (just 0.1pc below last year), with most regions planting a similar area to 2020.

“There may though be a slight decrease in winter-cropped area in major summer cropping regions, as farmers hold some paddocks to prepare them for summer planting,” Mr Voznesenski said.

He said the east-coast mouse plague continued to be a serious concern, with lost grain and hay reserves, downgraded quality of stock and increased costs to manage mice populations challenging grain farmers.

“The issue is particularly bad in, though not restricted to, central and western NSW,” Mr Voznesenski said.

“With winter here, we can expect colder temperatures to slow mouse populations. However, crop replanting and a re-emergence of populations in spring remain real risks in the outlook.”

For South Australia, total winter crop plantings are estimated down 1.3pc on last year to 3.6Mha.

A different year

While 2021/22 was shaping up as a second consecutive very good cropping season for Australia, there were marked differences to last year, Rabobank’s report notes. And these will have price implications.

Mr Voznesenski said in addition to the shift in planted area from barley and oats to canola, a noticeable move was also being seen from non-GM (genetically-modified) to GM canola, particularly in Western Australia.

“With the premium for non-GM over GM canola declining considerably, we have seen a greater uptake in GM canola this year, with the biggest rise in WA,” he said.

“With non-GM canola supplies tight around the world, this should support a rising premium for non-GM.”

Similarly, Mr Voznesenski said, growers were also noted to be switching from malt barley to feed barley.

“With less malt barley being planted and world malt demand recovering, we see the premium for malt barley over feed barley increasing this season from its lows,” he said.

Another factor of note, Mr Voznesenski said, was that approximately 25 per cent of last year’s east coast grain harvest remained on farm in storage and this would weigh on prices.

“Until the stored grain is sold down, local prices will continue to be restrained from fully following overseas markets higher,” he said.

Price outlook

For wheat, Rabobank sees CBOT (Chicago Board of Trade) wheat trading near to US650 cents a bushel out to quarter one 2022 then gaining marginally in quarter two – supported by a number of factors, including low global corn stocks.

A stronger Australian dollar and good local supply is however expected to temper local wheat prices this season.

A tight global corn market will also feed into support for barley in the coming year, Dr Kalish Gordon said.

“For Australian barley, pricing will continue to be reliant on the ongoing patronage of Saudi Arabia and Thailand,” she said.

“With good volumes of new Australian crop expected in quarter four this year and no expectation of resumption of the barley export program to China in 2021 or 2022, local prices will be kept in check.”

Global canola stocks are on track to end the 2021/22 year at a five-year low, and the bank expects Australian canola prices to remain elevated.

However, expanded planting will support higher production in 2021/22 and see local prices lag behind global, Dr Kalisch Gordon said.

Potential upside is seen for pulse prices in the year ahead, with scope for lentil and chickpea prices to lift on potential relaxation of some market access restrictions by the Indian government. However, periods of uptick rather than a sustained lifting in the price outlook are expected.

Source: Rabobank

Most encouraging to see the lift and the prospect of a second very good to excellent year emerging.