AUSTRALIA’s second largest winter crop and promising rainfall outlook will help drive Australian farmgate production to $65 billion in 2020-21, according to ABARES’ December quarter 2020 Agriculture Commodities report released today.

The report points to continued recovery for the farming sector from drought—and resilience in the face of COVID-19.

“Overall, Australian agricultural production is bouncing back from the drought,” ABARES executive director Dr Steve Hatfield-Dodds said.

“Australian producers manage one of the most variable environments in the world so ebbs and flows in production are to be expected.

“We’re expecting a near all-time high winter crop, the best ever in New South Wales, and a more favourable outlook for summer cropping than we have seen in recent years.

“Livestock prices have also stayed high with herd and flock rebuilding, and continued international demand.”

Fall in exports

While agricultural production is forecast to rise by seven per cent to $65 billion, exports are expected to fall by 7pc from last year to $44.7 billion.

“Exports have continued to find markets during the pandemic but the residual effect of past dry seasons and trade uncertainties are pushing down export value,” Dr Hatfield-Dodds said.

“Recovery from drought is limiting production and exports of livestock products and fibres, with meat prices also falling as the African Swine Fever impact on China’s pork production begins to lessen.

“There are a number of risks present for the rest of 2021 that remain a watch point, including wine trade with China and labour shortages for the horticulture sector.”

World wheat prices to increase

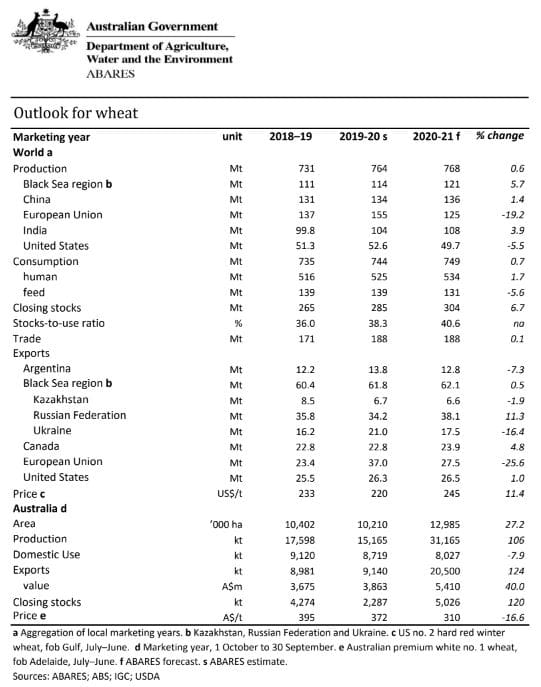

ABARES predicts the world wheat price will increase by 11pc in 2020–21, to an average of US$245 per tonne.

The higher prices reflect a fall in production in some major exporting countries in 2020–21, dryness during the 2021–22 winter crop planting window in the United States, the European Union and Russian Federation, and increased global import demand, particularly from China.

High global demand for staple wheat products is likely to be partially offset by a fall in demand for discretionary foods which have been affected by weaker global economic growth resulting from COVID-19 containment measures.

However, containment measures have not affected underlying demand for wheat.

World wheat production to reach new record

ABARES forecasts that world wheat production will increase slightly in 2019–20 to reach a record high of around 768 million tonnes (Mt) in 2020–21.

This is despite mixed seasonal conditions in major wheat-producing countries.

Increased production in Australia, Canada, China, India and the Russian Federation is forecast to offset lower production in Argentina, the European Union, the United States and Ukraine.

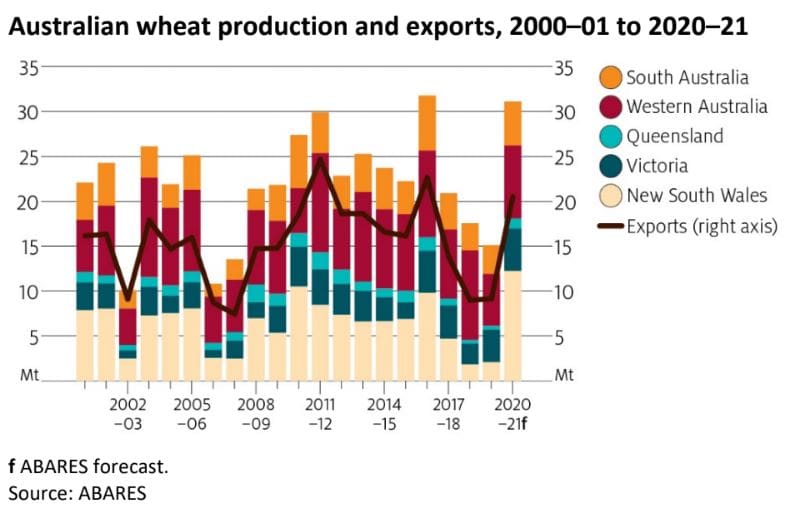

Australian wheat production is forecast to more than double in 2020– 21 to around 31Mt.

Ideal seasonal conditions in New South Wales, Victoria and South Australia are forecast to result in above average yields, particularly in NSW.

This is forecast to be partially offset by less favourable seasonal conditions in Queensland and Western Australia, where limited spring rainfall has reduced yield potential.

World coarse grain prices remain resilient

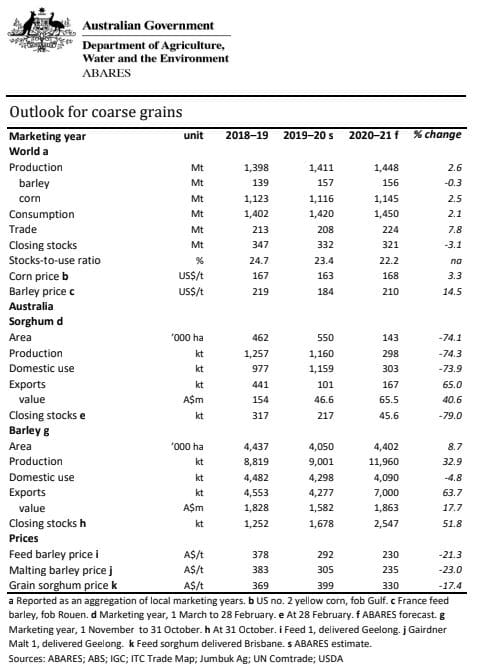

ABARES says the world indicator price for corn (maize) is likely to increase by 3pc year-on-year to US$168/t in 2020–21.

World production of corn is expected to reach a record high in 2020–21, however world demand, particularly from China, is expected to outpace production despite the COVID-19 pandemic.

The world indicator price for barley is also expected to increase by 15pc to US$210/t. World barley prices are being supported by increasing demand from China, dry conditions in the Black Sea region and reduced barley plantings in the United States.

Demand for barley internationally is also being supported by prohibitive tariffs on Australian exports of barley to China, necessitating a reorganisation of supply chains in China away from Australian production to alternative sources.

World coarse grain production to increase

ABARES predicts world production of coarse grains will increase by 3pc to 1.4 billion tonnes in 2020–21 underpinned by rising corn production.

Dry seasonal conditions in the Black Sea region and Europe have led to lower production with Black Sea corn production falling 15pc to 43Mt and EU corn production falling 4pc to 64Mt in 2020–21.

However, the decline is expected to be offset by rising production in North America, China and South Africa.

Barley production is expected to remain stable year-on-year at 156Mt. Production in Australia and the Russian Federation is expected to increase as a result of favourable seasonal conditions and increased plantings.

However, these increases are expected to be offset by falling production in Ukraine and Argentina following dry seasonal conditions and reduced plantings.

Increasing world oilseed prices

Oilseed demand and prices bounced back after a sharp decline at the start of the COVID-19 pandemic and have maintained upward momentum since April.

Recovering global demand is outstripping supply despite higher production and high carry-over stocks. This is expected to support prices for the remainder of 2020–21.

The world soybean indicator price is expected to increase by 26pc to US$438/t in 2020–21.

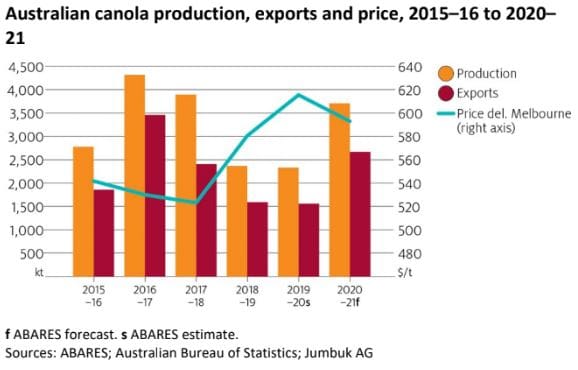

The Australian canola price is expected to return to export parity following consecutive years of drought- affected production, falling by 4pc to AU$593/t in 2020–21.

Slight rise in cotton prices

ABARES expects the world cotton price to average US73 cents per pound in 2020–21, 12pc below the five-year average in real terms.

Cotton prices are forecast to be 2pc higher than in 2019–20 due to lower world production and improved mill demand.

High stock levels resulting from interruptions to cotton mill operations will continue to maintain a low-price environment, with intense competition between exporters on the world market.

World cotton production is forecast to fall by 6pc in 2020–21 to 24.7Mt, largely due to area reductions in the United States, Pakistan, China and Brazil as farmers respond to low prices.

Consumption is forecast to increase by 9.5pc in 2020–21 to 24.3Mt, but remain below production and still 2Mt below 2018–19 levels.

Source: ABARES

The December quarter 2020 Agriculture Commodities report is available here

Grain Central: Get our free cropping news straight to your inbox – Click here

HAVE YOUR SAY