CBH Group’s Brookton site set a new daily receival record of 15,469t in the 2025-26 harvest. Photo: CBH Group

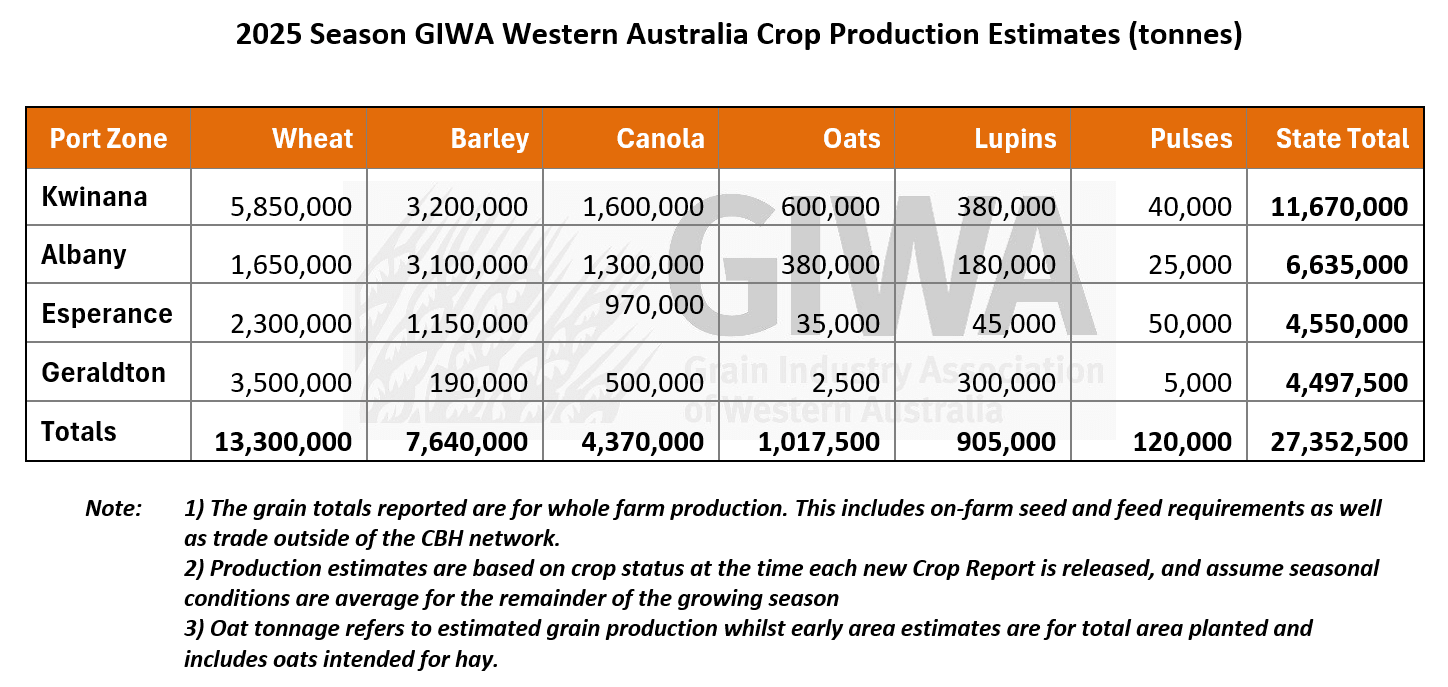

THE GRAIN Industry Association of Western Australia has called the record 2025-26 harvest at 27.35 million tonnes (Mt), a lift on its previous forecast of 26.55Mt released in December.

In its crop report released today, GIWA report author Michael Lamond has detailed WA’s fourth record crop in five years, saying production was fueled by exceptionally good yields in three of the five port zones and good yields across the other two.

“Adequate rainfall in July and August in most areas followed by mild temperatures during grain-fill allowed crops to push water use efficiency to very high levels,” Mr Lamond said in the report.

“An increase in total crop area of 6.8 percent from the previous record production in 2022 helped, considering most of this increase in areas was in the higher rainfall regions.”

GIWA figures show wheat and canola areas were down 3.3pc and 7.3pc respectively from 2022 area, while barley was up 26.4pc, lupins was up 17.4pc, and oats for grain and hay was up a startling 65.1pc.

The report said wheat crops in the central regions of the state suffered from a later start and less spring rain than further north and south.

“[This] resulted in yields being below previous record years and grain quality was erratic, with both high screenings and low protein resulting in downgraded quality segregations.

“Grain quality for wheat was also erratic in the southern regions, with low falling numbers, sprouting, and low protein also resulting in downgrading.”

The report said wheat crops across the state did not perform as well as barley for a range of reasons.

“Barley had a dream run for disease in 2025 and avoided most of the frost that shaved off over a million tonnes of wheat in the central regions of the state.

“Wheat also suffered more from grain quality issues where rainfall was light going into spring.

“The mild spring extended the grain-fill period, and where moisture reserves were low going into spring, wheat crops failed to fill the many available grain-fill sites fully.”

Conversely, this slow maturity period pushed grain yields for wheat to heights never seen before in areas that had adequate subsoil moisture.

Where top growth was excessive, and driven by the warm wet early stages of spring, the extended mild finish resulted in wheat crops “slowly transpiring themselves to death”.

This resulted in significant yield loss from grain weight, and then downgrading for quality.

“Barley grain yields and quality in most regions were good although many growers opted for voluntary downgrades to feed due to the low malt-barley premiums and simpler logistics for delivery.

“Barley profitability exceeded wheat in many areas and on the back of this, an expansion in barley area is likely for the 2026 growing season.”

Canola shines again

Canola was again the most profitable crop for most areas in 2025, thanks to the combination of above-average grain yields, and buoyant prices.

The price premium for non-GM over GM at harvest and going into the 2026 season will see the slight substitution out of the GM to non-GM that occurred in 2025 continuing in the southern regions in 2026.

Fueling this trend are the yields for newer imidazolinone and triazine-tolerant varieties getting closer to those from Roundup Ready lines.

“The area sown to canola will go up this year if there is an early break to the season, particularly now that the recent rains from ex-cyclone Mitchell have delivered some subsoil moisture across significant areas of the grainbelt.”

Growth for lupins, oats

The lupin area in the state increased by 11.2pc from 2024 to 2025 pushing production over 900,000t for the first time in more than 15 years.

“Variable grain yields and the cap on price in Western Australia continue to hamper the crop and a reduction in area substituted to canola is likely for the 2026 season.

Mr Lamond said oats has continued its push to becoming a substantial crop for WA growers, with oats harvested for grain consistently sitting around 60pc of the planted area over the past four years, and the remainder going to hay.

“Both oat grain and oat hay reached production levels around 1Mt in 2025, and whilst prices have come off from highs at the start of the 2025 growing season, they haven’t crashed as in the past.

“This maturing of the crop with diverse and growing markets coupled with growers having greater confidence in being able to reliably hit higher yields under a range of seasonal conditions will probably see the boom-and-bust cycles of the past, fade.

“However, saying this, early indications are that the crop area will contract in 2026 due to some questions around the sustained year-on-year growth putting a block on prices.”

Pulse crops went well in most areas in 2025, although prices remain a major stumbling block for further substantial expansion.

“There are a raft of hurdles for all the pulse crops to overcome before there is likely to be any significant jump in areas in the future.

“The most promising is lentils based on 2025 yields across the state, whilst the areas planted to faba beans, field peas and chickpeas are all likely to stay stagnant in 2026.”

Crops costly to grow

Mr Lamond said many growers in the better areas had good operating margins thanks to relatively high yields, even though grain prices were down from previous years.

Across the state, the total value of production was greater than the previous record year in 2022.

This was skewed to the perimeters of the grainbelt, with the central regions where crops were lower yielding recording significantly lower operating margins than 2022.

“With these lower grain prices last harvest, small changes in farm gate return due to factors such as quality downgrading pushed the breakeven yields required to be profitable to historically high levels.

“Projected budgets for 2026 are tight for many, even though some of the main operating costs such as fertilizer and crop protection products have not spiked in price.

“Self-inflicted business costs such as machinery and land purchases are having a greater impact on budgets than some of the major variable costs.

In the past, tight budgets have resulted in growers pulling back and becoming more risk averse.

“This time round, there is a quiet confidence among growers that they can now hit these higher yield levels required to maintain profit under a range of seasonal conditions based on recent history.

“In saying this, most growers are expecting that the good times can’t last and will be preserving capital rather than aiming to maximise profit.

If the break of season is late in 2026, this could mean more fallow in lower-rainfall regions, and not committing to advance idea about canola area in low to medium-rainfall regions.

“On the production front, overall sentiment is positive going into the 2026 growing season, but growers remain concerned about external factors affecting global trade, to which Western Australia is heavily exposed.”

Source: GIWA

Further detail on crop conditions in individual WA port zones can be found as part of the full report on the GIWA website.

HAVE YOUR SAY