Endeavour Wines has not renewed its tenure of Warakirri Diversified Agriculture Fund’s Chromy Estate in northern Tasmania, an indicator of issues tied to property under permanent plantings. Photo: Warakirri

IRRIGATED land under permanent plantings may be moving out of passive investor hands and into those of owner-operators in coming years, according to Roc Partners’ investor director agriculture and partner Frank Barillaro.

The insight came ahead of Mr Barillaro’s presentation on June 11 to the annual Global AgInvesting conference, its first to be held in the Southern Hemisphere.

Asia-Pacific region specialist private markets investment manager Roc Partners was the sponsor of Mr Barillaro’s presentation, entitled: The sale and leaseback market – has the bubble burst?

Roc Partners manages capital for some large Australian institutions, as well as family offices, foundations, endowments, and high net-worth investors across the world.

Image 1: Growth in land value is typically lower for permanent plantings, which require cyclical investment in trees or vines, than on annual crops. Source: Roc Partners

Pressure for permanent plantings

Figures contained in Mr Barillaro’s presentation indicated the sale-and-leaseback bubble has most definitely burst, at least when it comes to owners of land under permanent plantings.

“Grain and cotton are less sensitive; you can remove a crop year on year and a lot of the underlying value is in land price growth,” Mr Barillaro told Grain Central.

“In permanent crops, because you’re effectively buying depreciating assets, you’re relying on…operations to cover your rent and then make a profit.”

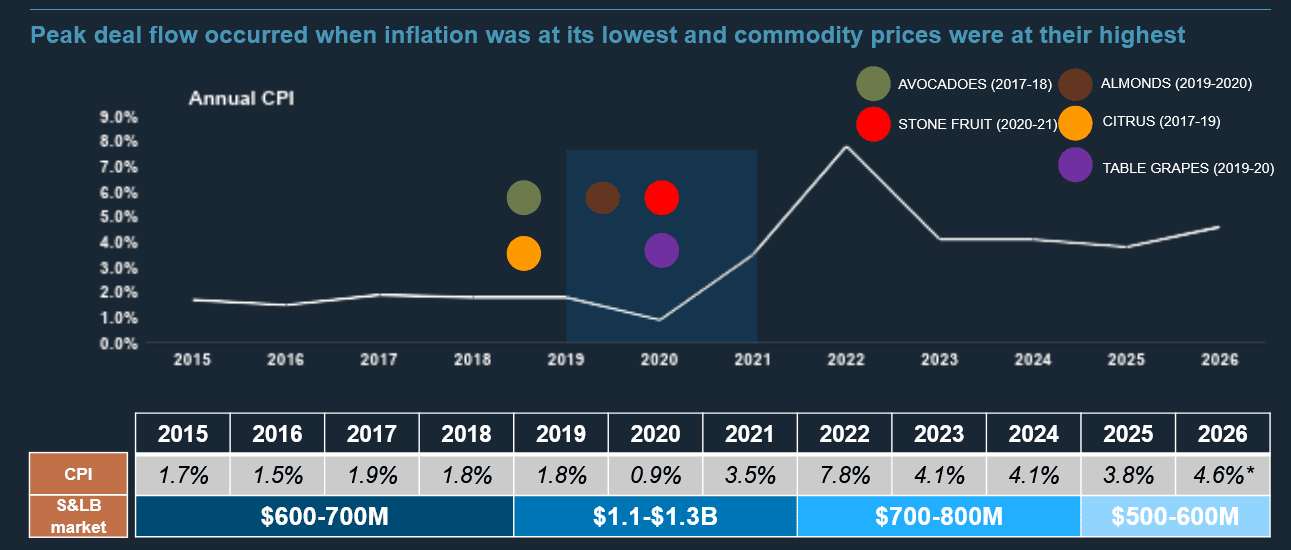

Image 2: Inflation as indicated by the Consumer Price Index, overlaid on Roc Partners’ estimate for total value of transactions in the class for grouped years between 2015 and 2026. Source: Roc Partners

Grapes and almonds were given as examples of permanent plantings not making lessees enough money to pay the rent and turn a profit.

“With lower commodity prices and higher costs such as water, the profit margins have been under pressure.”

Mr Barillaro said that has meant escalating rents are further pressuring lessees’ returns.

“When the lease comes up for renewal, there’s a question mark to say: Does the tenant go again?”

Mr Barillaro said a lot of sale-leaseback transactions were done when inflation was “really low”.

Asset types feeling the impact of inflation include almond farms in the Riverina, leases for which may have another 10 years to run.

Endeavour Wines’ announcement last month that it would not be renewing its lease of Oakridge in Victoria’s Yarra Valley and Warakirri’s Chromy Estate in northern Tasmania indicate country under grapes is also affected.

“Endeavour Wines recently announced they are not going to renew their vineyard leases.

“We think there’s going to be more and more of that.”

LVR hits 100pc

Loan-to-value ratio, or LVR, represents the amount borrowed to buy the asset as a percentage of the value of the asset.

Mr Barillaro said sale-and-leaseback has shifted in the past 10 years from being a tool to release capital as a portion of the value.

Roc Partners’ Frank Barillaro.

“Somewhere between 2015 and 2020, this market kind of exploded, and it became a 100pc financing tool.”

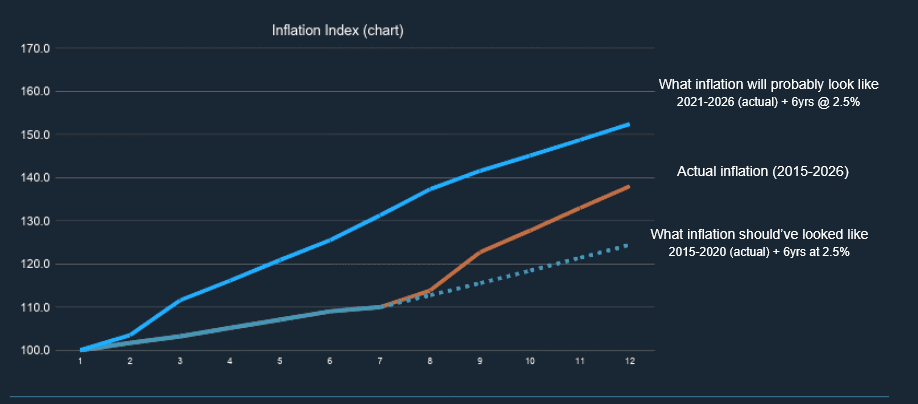

“This has seen a number of very expensive leases entered into 5-7 years ago that have experienced massive annual rental escalators due to inflation.”

“Valuations have outpaced operating profit; either land prices have to come down, or the operating profits have to go up.”

If the current lessee cannot afford to pay the rent required without eating into its profit, chances are there will be others in the same boat.

“Our thesis is there’ll be a lot of those properties coming to market.”

“We think the most likely form is that it ends up going back to an owner that owns and operates, instead of a land-and-tenant structure.

“What has happened over the last 10 years is that landlords are willing to pay the full amount of [the farm’s] value.”

“This has essentially created a 100pc LVR financing vehicle…because most, if not all, leases increase each year with CPI, [so] the cost of rent goes higher and higher.

“In most cases, rent has gone up more than the operating profits.

“This has created a scenario where a number of these leases are no longer economic and the farmer is unlikely to renew the lease.”

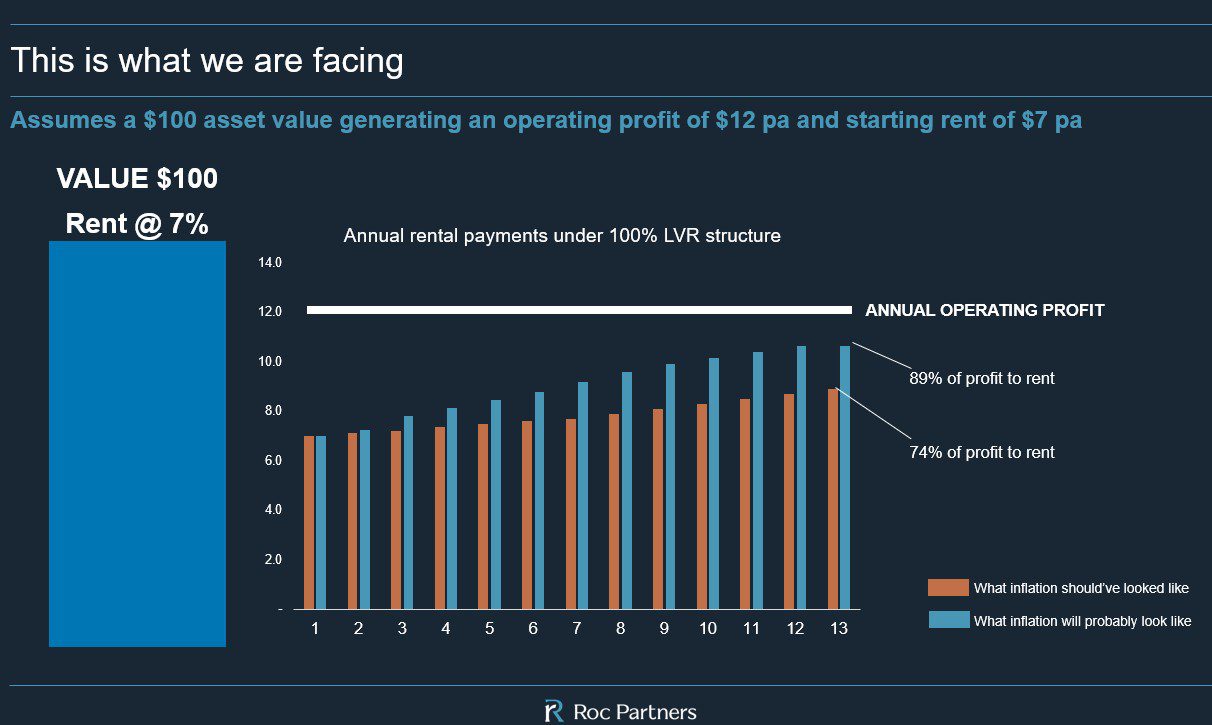

Image 3: Source: Roc Partners

As an example, think of a farmer who owns a citrus farm valued at $1,000,000 as a standalone asset, and needs finance to operate it.

A bank would normally lend the farmer 40-50pc of its value, and the farmer would use this facility to run the farm, make a living, and pay interest to the bank on the borrowings.

Under a sale-and-leaseback model of 15 or so years ago, an investor would typically advance the farmer $600,000 in exchange for a rental income, and the opportunity to sell the asset and achieve capital growth at the end of the lease period.

The sale-and-leaseback model has typically given the farmer access to a greater amount of capital than is available through retaining title and borrowing from a bank.

Image 3: Roc Partners

Sale-and-leaseback typically runs over a lease of 10-20 years, and does not require the tenant farmer to spend $300,000-$400,000 at its expiry to replace the trees.

The sweetener for the investor, or landlord, has been the ability to achieve capital growth at the end of the lease period.

“By the end of the 20 years, the trees have depreciated to a zero value, but the land and infrastructure hold their value.”

Grain Central: Get our free news straight to your inbox – Click here

HAVE YOUR SAY