The access to, use of and reliability of water continues to be a strong driver for rural land sales, where higher-value crops or permanent plantings are replacing traditional land use, Herron Todd White says in its latest August property market report. There is still capital for such new developments, but finding the right combinations of land, water, region and supporting infrastructure is proving a challenge for this capital. With the latest North Queensland water allocations release completed recently, HTW’s Roger Hill provides an overview of this market….

Industry stakeholders have all voiced their welcoming of Queensland Minister Anthony Lynham’s recent announcement of the release of 92,500 megalitres of water in the Flinders and Gilbert River systems in North Queensland.

This round of allocations is proposed to be at a fixed price. That is good too, isn’t it? Well, perhaps.

What price per megalitre is going to hit the nail on the head for northern agricultural industry development this time? Has there been any mention of tradability? Or will these allocations be tied to the parcel?

What development covenants or policies are going to complement the price so that collectively, government and industry can look back in ten years’ time and say, “We did get it right that time”?

These are simplistic questions, but they need to be addressed by all stakeholders. Remember, this has to be a win-win for government, landholders, local towns and communities and investment partners (be they equity investors or debt raised through the banking sector).

Pricing

There are various methods to determine the price. These should all be considered independently in such an immature and developing market area.

There are both bottom-up and top-down methods to calculating the price for water. Independent advice should be sought to ensure that the water price modelling is appropriate.

There is some relevant market history in the local area. Careful consideration is required to contemplate the price discussion with the result:

- The first round of allocations for the Flinders and Gilbert River averaged $36 per megalitre. The result: industry was unhappy with the division of allocations. Government was unhappy that none of the allocations were utilised and local communities missed out on any economic benefit

- The second round of allocations saw government implement more structure to the distribution via reaches. To force industry to use the allocations, the minimum bid of $46 per megalitre model was introduced. The result: Limited successful tenders, lots of talk, no benefit to communities and no projects developed

- In 2016 there was an opportunity for graziers to purchase Great Artesian Basin Sustainability Initiative (GABSI) allocations which were to be attached to their bore supply. The price was fixed at $1,430 per megalitre. The result: Government said there was low demand due to only a small uptake. Industry buyers were scared off by the price. Industry commentary was that had the price been reasonable, then there would have definitely been more applications and acceptance of the offer documents.

These three examples demonstrate the importance of the price relationship to covenant, allocation and policy design. So, what broader market price parameters are relevant? A quick survey of the Herron Todd White independent rural valuers around Queensland yielded the following:

Southern Queensland

- Current trading price range for high security water is $3000 to $4000 per megalitre. High-priority (100pc reliability) water across the Border Rivers and Gwydir River systems in northern NSW where delivery infrastructure is in place and the water is used for irrigating intensive agricultural and orchard type crops.

- Majority of water trading in this area is medium priority or supplementary (water harvesting).

- Medium priority water has water delivery infrastructure in place (landowner owned). This includes pumps, supply channels and dams. Medium priority water is used for broad scale irrigation (eg cotton). This water is trading from $1,750 to $2,200 per megalitre and peaking around St George to $2,500 per megalitre.

- The lowest priority water is from water harvesting. In NSW this is called supplementary, in Queensland this is called unsupplemented water. These allocations use the same farmer owned delivery infrastructure as medium priority allocations.

- In Queensland, the unsupplemented water (Condamine and Balonne Rivers) allocations form the highest volume of market trades. These allocations trade for about $1300 to $1700 per megalitre in Qld and a slight discount in NSW.

Key points to consider here:

- Mature water trading market

- Established high gross margin industries

- Established knowledge capital on how to grow high gross margin crops

- Development finance and capital not required as the scheme is established

- Established financial relationships with experience with water and irrigation returns on investment risk parameters so that debt funding and equity instruments can be written

- Infrastructure is developed and is working – there is no development risk

- The free market scarcity (demand) has driven the water price to these ranges

- The towns and communities have developed a workforce, service centre and infrastructure to support the surrounding industries.

Central Queensland

Medium priority sales are ranging from $1700 to $1900 per megalitre; while high priority sales are few and far between and peaking at $2500 per megalitre.

The above points regarding industry maturity, high gross margin crops, developed infrastructure and communities are relevant again.

North and Far North Queensland

- Atherton Tablelands water is trading at an all-time high of up to $3000 per megalitre due to the scarcity of water. This scarcity arises not just due to the drought, but also due to the cropping area expansions being such that crop demand is much higher than the allocated water.

- Limited trades at all. There is no scarcity. This is an immature trading market. The irrigated production areas are the same size as they were when the allocations were detached from the land titles so there is no increase in demand above the allocations that farmers already have. Reported value apportionments in sale contracts of farm, water, plant, crop is reported to range from $50 to $70 and sometimes $90 per megalitre.

The previous points regarding industry maturity, high gross margin crops, developed infrastructure and communities are relevant again.

Further development considerations:

The initiative to develop a project must also provide adequate return to the investor, farmer or grazier developer and financier.

In time, the broader goal is for high gross margin crops, however the first incubator irrigation sector is the fodder crops for hay and silage. You might recall that in 2012/13, hay was in short supply and was being trucked from southern districts.

Hay farmers in north and north-west Queensland that year experienced peak demand and high gross margins. As soon as it rained late last year and when cattle numbers reduced, the contrary situation existed. There was limited demand and of course, no gross margins (possibly even a loss).

It is evident that the gross margin volatility is an economic issue – not all is smooth sailing and this is a risk that the industry has been worried about. Bearing in mind the three local market instances of pricing mentioned earlier and the broader established market information, the question arises as to what price can be afforded for the water given the value of the land underneath the farm site, the investment in earth works, water works and seed to create a crop.

Investment decisions require prudent consideration of a profit/value return for the effort and risk taken to develop a project. Why would an investor (in this case, a grazier/farmer, banker/investor) inject capital in such a project if there was no capital value return?

There is an opportunity cost and a rate of return required to make such a development decision to evolve the business model to incorporate the farming activity and potentially create employment within the wider community.

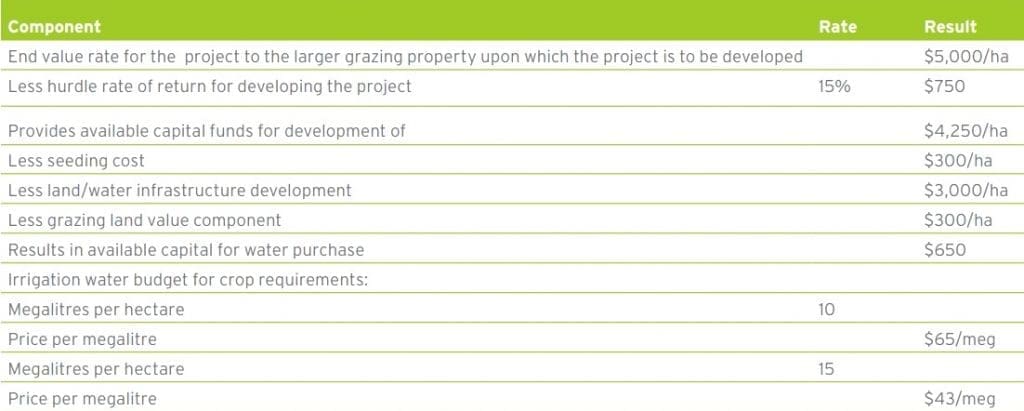

A recent exercise with one of HTW’s trading type grazing clients identified that for the highest and best use of the grazing land to be better and put to a farm project, the hurdle rate of return had to be greater than 15pc off tight Mitchell grass downs.

From an urban development perspective, 15pc is likened to a basic subdivision project, not the development of a farming block harvesting water from the Flinders River or Gilbert River. This hurdle rate of return has been used in the following straight line back of the envelope development model example.

You might choose to use a higher risk to represent that of the seasonality of water harvesting. There is sales evidence in the north and north-west Queensland rural property market where the added value of fodder crop farming areas range from:

- $2500 per hectare (this was a mortgagee sale of a western block that was not in production, the soil required re working; had an empty earth storage tank and is exposed to the seasonality of gulf river harvesting); to

- $8500 per hectare for an area under centre pivot on a larger cattle station (in use; established to Rhodes grass farm; pumping from a year-round reliable river source).

If one of these projects were to be developed on a downs grazing block then perhaps the added value rate might be $5000 per hectare once established in this example.

Further considerations:

- Planting cost – $300 per hectare

- Development cost – removing the Mitchell grass, laser levelling, constructing bays, and laying pipelines from the bore – roughly $3000 per hectare

- Grazing land sales suggests the underlying grazing land rate of $300 per hectare ($120 per acre).

The following model (demonstration purposes only – not a valuation, so use your own inputs especially if you are proposing higher gross margin crops) applies these variables to provide industry with a calculation model to determine how much capital is available for the acquisition of the water.

Click on image for a larger view

This model provides only one example of pricing methodology at a low risk, low return rate of 15pc. Pricing in a higher risk would lower the available capital to spend on the water.

The larger scale operators will employ the use of discounted cash flow analysis to give dynamics to the timing of each stage of the respective projected capital expenditure and the expected cash inflows.

The interesting point here is this basic, back of the envelope model provides a similar range to the previous pricing of the first and second rounds of allocation tenders. Perhaps the covenants and policy need to be collaborative to actually make good use of this opportunity.

Collectively, what do you think is relevant to ensuring a win-win so that in ten years’ time, industry and communities have grown positively? Should co-investment by government in infrastructure be explored perhaps? What about financial structure around the purchasing of the allocations?

Debt may not be available from existing channels to acquire the allocations and then to construct the farming project. Perhaps the financing of the allocations can be on a progressive payment basis.

You might be aware that this has happened before in the form of freeholding leases. Perhaps the ballot system, similar to that of the Brigalow Scheme would be worth re visiting. Through collaboration with the investors/financiers, the structure of the allocation payment scheme may help to finance the project development.

Is there any reason why access to development funding cannot be sourced or co-secured by government? It is noted that government sought to implement an initiative to force the use of allocations in the second round. Perhaps a requirement for the allocation funding agreement and structure would result in a time frame for development and use of the allocation.

As industry stakeholders have stated, this is a good opportunity, however a collaborative approach will be required to address stakeholders’ needs so that this announcement does in fact materialise into being a winner for North Queensland.

Source: HTW

HAVE YOUR SAY