EVOLUTION is a fact of life and trade. What seems like a static situation never is. At times, such evolving situations become more apparent, as is happening now in the grains industry.

The impact of Black Sea wheat in world markets is a hot topic for the Australian grains export industry because of the impact it can have on Australian wheat prices.

The impact of Black Sea wheat in world markets is a hot topic for the Australian grains export industry because of the impact it can have on Australian wheat prices.

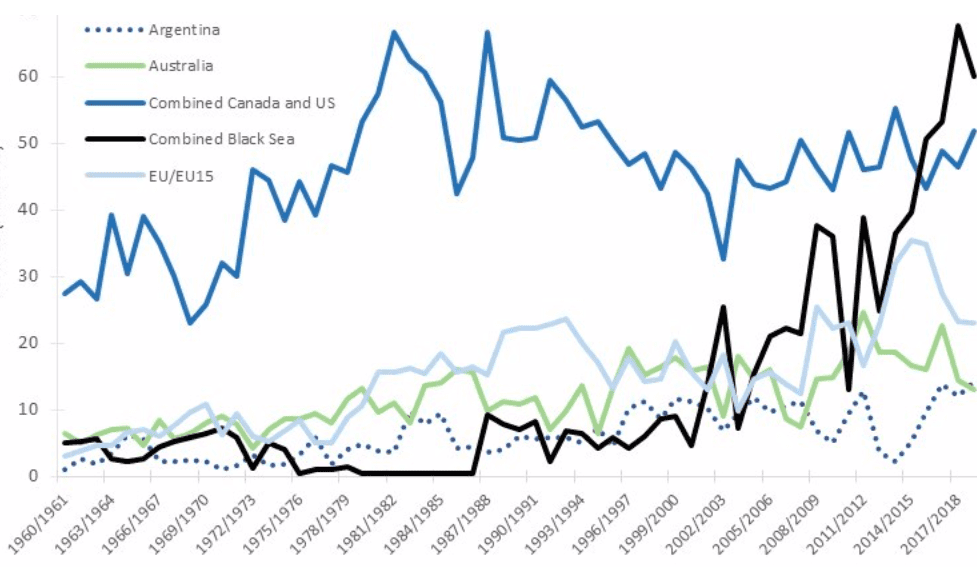

Formerly, international wheat market prices were dictated by the combined might of North American production from the United States and Canada. However, this dominance has recently shifted, with exports from Russia, Kazakhstan and the Ukraine (aggregated below as the ‘Black Sea’) exceeding those combined from the US and Canada.

The heyday for North American wheat exports was in the mid-1970s.

During this period the amount from the US and Canada made up around 70 per cent of the what the groups shown in Figure 1 exported.

In the last five years that level has dropped to 30pc.

In contrast, since the turn of the millennium, exports from the Black Sea have risen at a rate of around 2.8 million tonnes per year.

A consequence of this has been the increased market share of Black Sea wheat exports into regions like MENA (Middle East & North Africa), as well as further afield into South-East Asia, placing pressure on Australia’s market share.

Figure 1. Black Sea tide rising, wheat exports (million tonnes) top blue line combined Canada and US, black line combined Black Sea origins. Source USDA PSD

While these changes to global wheat trade have been evolving, the emergence of an alternative value proposition based on crops other than wheat has been occurring at home.

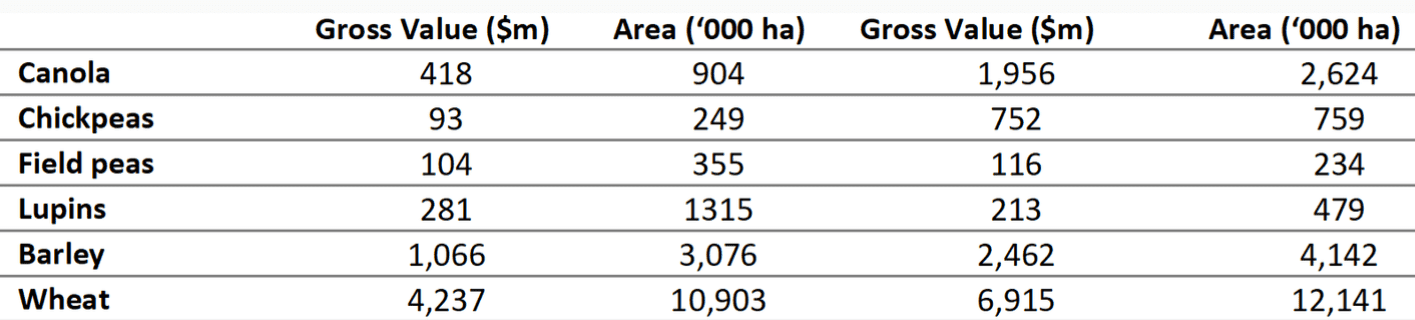

If we compare the makeup of the Australian broadacre crop from the late 1990s to more recently (Table 1), the standout increases have come from canola and chickpeas.

Barley has over doubled in value, but the wheat increase has been more modest while field peas and lupins have decreased in value and area (noting the gross value figures are not adjusted).

Table 1. The changing profile of Australian winter grains from the late 1990s (left) to recently (right) showing the standout increases in value proposition coming canola and chickpeas. Barley has over doubled in value, but the wheat increase has been more modest while field peas and lupins have decreased in value and area. Source ABARES

Canola has become an increasingly important component of the Australian grain grower’s profitability equation—particularly in the winter rainfall environments from NSW across to Western Australia.

In addition to its relative monetary value, canola provides break crop rotational benefits, for growers with access to GM technology there is an additional tool for weed control at their disposal.

Furthermore, while prices will always fluctuate, canola has also provided relatively stable returns compared to other commodities, providing growers with a reliable source of much-needed cash flow.

That said, these positive aspects are somewhat dampened by higher input and management requirements, which means that most growers are reluctant to make canola their sole cash crop, despite such attractive economics compared to alternatives such as wheat and barley.

The expansion in area of canola production has coincided with greater healthy food awareness and Europe’s demand for biofuel.

Health trends will continue to support demand for healthy oil and other food products, but cheaper palm oil will continue to dominate unless more consumers proactively seek out sustainably-produced and healthy products, rather than the cheapest.

While support for sustainable biofuel production is currently strong in Europe, a change of attitude and support would significantly impact demand for Australian canola. The major canola exporters are Canada (60pc which is predominantly GM canola), Australia (20pc) and Ukraine (10pc).

A unique aspect of the canola supply chain—as opposed to cereals—is that in the process of extracting the oil, an equivalent amount of high-quality meal is produced.

This meal is readily consumed by the pork, poultry and dairy intensive animal feed sectors, particularly where canola production, crushing and intensive livestock industries are located in close geographical proximity.

The combined value of both the meal and oil, in particular where there is strong domestic demand, has contributed to relative consistent grower returns.

However, what constitutes a good quality oil profile does not mean the resultant meal is of the same good quality.

A common breeding challenge is the trade-off between traits with improvement in one area often being detrimental to another.

If demand for healthy oil options continues, then canola may need to move towards specialty products like Monola becoming the mainstream product.

In some instances, this may have undesirable consequences for the quality of canola meal.

To date, the Australian industry has been well supported by collaborative monitoring of varietal quality parameters, and this needs to continue.

Without ongoing support, quality profiles may shift unintentionally in the pursuit of one stream of canola processing over the other, consequently reducing the sum value of the oil and meal.

It may be risky to assume that European Union demand for canola will remain at current levels.

Since 2012/13 the five-year average of Australian exports to EU was 63pc.

EU demand is linked to its policies on clean fuels and renewables.

A competitive advantage Australia has over Canada has been Europe’s preference for non-GM canola, which is due to stringent labelling requirements for by-products containing GM material (e.g. meal in livestock feed rations and glycerol in cosmetics).

Consequently, the Australian industry has implemented rigorous handling management programs to support exports of non-GM canola to Europe, such as traceability certification and stringent testing to prevent the adventitious presence of GM material in shipments. This usually results in premium prices for non-GM canola over its GM counterpart.

Part of the certification process involves the calculation and subsequent declaration of greenhouse gas emissions along the entire value chain.

From 1 January 2018 those emission savings need to be at least 50pc (or 60pc for a new biofuel production facility), an increase from the existing default value of 35pc.

In preparation for that change, AOF, AEGIC and key researchers negotiated a new standard for Australian canola exports (see Blog 19 – How does low emission canola benefit Australian farmers?).

While this ensures the continuation of existing EU canola exports, it highlights the need for vigilance regarding the access requirements of our key export markets.

The impact of changing market rules is well understood by those involved in pulse exports to India. In the space of a year, the situation changed from positive to one of grave concern.

Pulse Australia media release, 26 October 2016

The pulse industry is now in a very positive position. Globally, demand is strong and growing. Locally, farmers are growing more pulses — area planted is up 35 per cent over the last decade. Even more importantly, value is growing because pulse prices are strong and thriving export container supply chains in Australia are adding value and creating regional jobs.

Pulse Australia media release, 28 December 2017

On Thursday 21 December, the Indian Government announced a 30pc tariff on imports of chickpeas and lentils, effective immediately. This will hit Australia’s two most important pulse crops hard, right in the middle of our harvest and when much of our export trade is getting under way for the year. This move follows hot on the heels of the 50pc tariff impost on field peas announced about a month ago.

These examples illustrate the importance of large export markets for canola and pulses to Australian farmers on one hand, however over-reliance on a few countries can have unexpected consequences.

Those trading pulses to India know that volatile markets can be rewarding and challenging at the same time.

The Australian grains industry, particularly for canola and chickpeas exports, needs to be strategic with its market options, lest being caught unprepared when large export markets change their policies or preferences. Proactive market diversification in terms of crops and products is more effective than reactive contingency and emergency responses.

Source: Colere Group, colere.com.au

Read the original AEGIC blog here

Report authors from the Colere Group,

- Managing director, Paul Meibusch

- Principal associate, Dr Jorge Mayer

- Senior associate, Dr Richard Williams

The Colere Group works with clients to bridge the gap from strategic food, fibre and biotech science to commercial results. Our strength is providing superior technical expertise in combination with commercial skills and business analysis through a strong group of non-exclusive associates and key collaborators. The Colere Group has been active in the intersection between grains R&D and commercial activities with roles in reviewing R&D programs, advising corporate growers and managing grains industry commercialisation.

HAVE YOUR SAY