AUSTRALIA’s 2017 wheat crop is forecast to be 24 million tonnes, down from a record 35Mt in 2016, due to depressed cereal prices and an autumn which is forecast to be drier and warmer than average, according to the latest USDA Grain and Feed Annual report.

The USDA predicts Australia will produce 24 million tonnes of wheat in 2017.

The report predicts Australian winter crop production will decline significantly in 2017/18 due to less favourable seasonal conditions and in response to low world prices.

Barley production is also forecast to drop significantly to 8.5Mt in 2017/18 from 13.4Mt in 2016/17.

Australia’s 2017/18 wheat exports are estimated to be 18Mt, down more than 20 per cent on the previous year’s volume, because of lower production, continued strength in the Australian dollar, and “possible continued shipping delays”.

While forecast production figures in the report released on 18 April were roughly in line with Australian industry expectations, USDA’s downward revision of current-crop wheat volumes was not.

Logistics questioned

The report states Australia’s exports of wheat have been affected by a range of transport and logistical problems, and exports for 2016/17 have been revised down.

Australian trade sources report that export performance has been anything but poor.

On the contrary, Market Check head of marketing and advisory Richard Perkins said logistics had been negatively affected but Australia had exported an all-time record as at the end of March 2017.

USDA also revised down 2016/17 wheat shipment estimates because of “port and logistical problems”, which it said could continue for the rest of the year.

Storage and handling operator Viterra, a division of Glencore Agriculture, said its rail and road network had been working very efficiently in out-turning grain from upcountry sites to port and had been meeting all of its export requirements.

“Viterra has shipped more than 4Mt of bulk grain from its six ports already this season,” Viterra general manager logistics and commercial relations Jonathan Wilson said.

“From December 2016 to March 2017 3.2Mt of grain was shipped – the largest four months in a row on record.”

In terms of storage, the USDA report estimates Australia’s total on-farm and warehousing capacity may exceed 15Mt.

It said new port facilities built over the past five years had added 4Mt to capacity.

Industry sources report increased capacity, provided by new terminals at Bunbury in Western Australia and Port Kembla in NSW, had more than compensated for losses of throughput such as a shortage of containers, and temporary suspension of wheat deliveries to GrainCorp’s Port of Geelong facility in January and February.

Wheat outlook

Based on current seasonal outlooks, the 2017/18 yield is forecast at 1.9t/ha from 12.8m ha, and cereal area is forecast to drop in favour of alternative crops like canola which have a stronger price outlook.

USDA forecasts Australia’s 2017-18 total domestic wheat consumption at 7.96Mt in 2017/18, down from a revised estimate of 8.96Mt for 2016/17. This decline represents an expected return to normal consumption of feed wheat after a record harvest.

The consumption figure for 2016/17 has been revised upwards because of the plentiful supply of feed wheat, which is likely to boost demand.

Even with relatively low domestic prices, sales to pig, chicken and dairy industries could be expected to increase, especially as international prices remain very low, while port congestion and costs have increased.

Exports in 2016/17 will be 23Mt in the marketing year from October 2016 and 22Mt respectively for the trade year from July 2016.

These revisions are below the official estimates due to ongoing port and logistical problems, which have continually hampered wheat exports and could continue for the rest of the year.

Wheat stocks will increase in 2016/17 to 8.8Mt because of shipping delays and the record size of the crop; this is up 1Mt from the previous estimate of 7.8Mt, with lower grades still expected to form the bulk of the volume.

In 2016/17, average wheat yields increased from a five-year average below 2t/ha to 2.7t/ha due to exceptional in-crop rain.

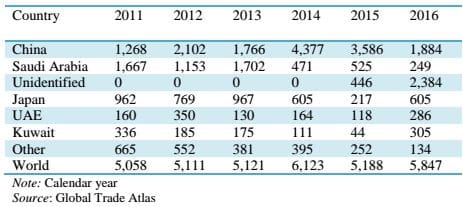

Table 1: Australian exports of wheat, 2011-2016 (‘000 Mt)

Barley outlook

Barley exports are expected to increase slightly for 2016/17 due to increasing monthly shipments. Stocks of barley are expected to increase in 2016/17, in line with the official estimate.

Port and logistical delays have affected shipments of winter crops from Australia, but this problem may be less important for barley exports as monthly shipments have continued to expand.

Australian barley exports at 5.5Mt in 2017/18, down from 8.5Mt in the current year due to record production and high grain quality.

This forecast is slightly above the official estimate because of a recent upsurge in barley exports from Australia.

The report said demand for malting barley was expected to be stronger over the year, with lower supplies from some other countries.

Feed barley prices were estimated to have fallen US$30/t year-over-year because of oversupply in Australia and in the world market.

USDA estimates Australia’s 2017/18 barley crop to yield 2.4t/ha over 3.5m ha, compared with 3.3t/ha over 4m ha in 2016/17.

Table 2: Australian exports of barley, 2011-2016 (‘000 Mt)

Sorghum

USDA forecasts Australia’s sorghum production to fall to 800,00t from 300,000ha in response to an expected switch to alternative crops such as cotton and pulses with stronger price outlooks.

Flagging demand from China and other export markets, as well as domestic consumers, has fuelled the foreseen softening of values.

HAVE YOUR SAY